Arro Team

Table Of Contents

The Rewards Trap: Why Cash Back Can Backfire

The Mindset Shift: Cash Back Is A Bonus, Not A Goal

Smart Cash Back vs. The Overspending Trap

The 4-Step Framework For Cash Back Responsible Use

Let’s Talk Numbers: When 1% Actually Adds Up

How The Arro App Keeps You Honest

FAQ

Let’s be real for a second: cash back rewards sound amazing until you realize you spent $200 you didn’t plan on just to “earn” $2. That’s not a reward. That’s an expensive hobby.

And it happens more than you’d think. With most credit cards, cash back is designed to get you to spend more. The more you use the card, the more rewards you earn. Over time, that can quietly push you to spend more than you planned.

This guide is about keeping that line crystal clear. We’re talking about cash back responsible use, how to actually benefit from everyday spending without letting them trick you into spending more than you should.

No lectures, no complicated math. Just real talk about making rewards work for you instead of the other way around.

Key Takeaways

Cash back rewards only work in your favor when you use them on purchases you’d make anyway, like gas and groceries.

Spending more to “earn” more is the most common cash back trap, and it costs you way more than you earn.

The smartest approach: budget first, swipe second. Your spending plan comes before your rewards strategy.

Arro’s 1% cash back on gas & groceries is designed for everyday essentials - the stuff you’re buying regardless.

Checking your spending daily in the Arro app (2 minutes) is the simplest way to make sure rewards don’t lead to overspending.

The Rewards Trap: Why Cash Back Can Backfire

Here’s something nobody puts in the rewards marketing: cash back programs are designed to get you to spend more. That’s not a conspiracy, it’s literally the business model. The more you swipe, the more the card issuer earns in transaction fees. Your cash back is their cost of doing business.

And for many people, it works exactly as intended. You see “earn cash back!” and your brain translates that to “I should buy more things.” Suddenly, you’re filling up premium gas because it’s “earning you more rewards” (spoiler: the extra $8 per tank gets you some points back).

This is the overspending trap, and it’s sneaky because it feels like you’re being financially smart. You’re not being reckless, you’re “maximizing rewards.” But the math doesn’t lie. Every dollar you spend beyond what you planned is a dollar lost, minus one penny earned. That’s a terrible return.

The good news? Once you see the trap for what it is, it’s pretty easy to avoid.

The Mindset Shift: Cash Back Is A Bonus, Not A Goal

This is the single most important reframe for responsible cash back use: rewards are a bonus on spending you’d make anyway. They’re not the reason you spend.

Think about it like this. You need gas to get to work. You need groceries to eat. Those purchases are happening whether or not you earn cash back. The 1% back from your Arro Card is just a nice little thank-you on top of the spending you already planned.

The moment you start planning purchases around earning rewards? That’s when it flips. That’s when the reward stops being a bonus and starts being an excuse to spend more.

So before you swipe, ask yourself one question: “Would I buy this even if there were zero rewards attached?” If yes, great, enjoy your cash back. If the honest answer is no, put the card away. That’s not a reward. That’s a loss you haven’t calculated yet.

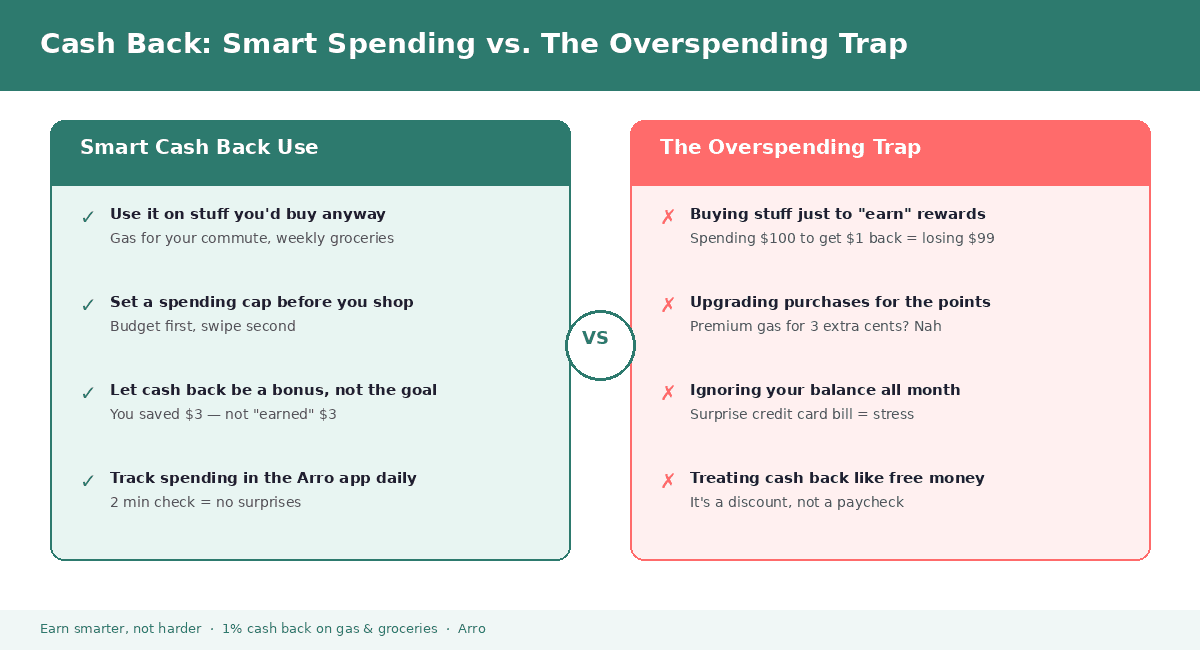

Smart Cash Back vs. The Overspending Trap

Let’s make this concrete. Here’s what cash back responsible use looks like in real life versus what the overspending trap looks like - because the difference is way more subtle than most people think.

Smart: Using Your Arro Card At The Gas Station You Already Go To

You drive to work. You need gas. You’d fill up regardless. Swiping your Arro Card earns you 1% cash back on purchases already in your budget. That’s the whole point. No extra spending, free reward.

Trap: Driving To A Farther Gas Station Because It’s “More Expensive = More Rewards.”

Nobody actually thinks this consciously, but the logic creeps in. Spending more on gas doesn’t earn you more in any meaningful way. An extra $10 at the pump gets you… 10 cents. And you burned extra gas on the drive there.

Smart: Weekly Grocery Run With A List And A Budget

You know what you need, you go get it, you swipe your Arro Card. The 1% back on that $75 grocery run is $0.75 you didn’t have before. Multiply that over a year, and it adds up, without changing your spending at all.

Trap: Throwing Extra Stuff In The Cart Because “I’m Getting Cash Back Anyway”

That $20 impulse snack haul earns you 20 cents back. You’re still out $19.80 on stuff you didn’t plan to buy. The reward didn’t cover it - not even close.

Also Read:

Credit Builder Programs Compared: Arro vs Kikoff vs Dovly vs TomoCredit (2026 Guide)

How the Increase in Fed Interest Rates Affects Your Credit Card

The 4-Step Framework For Cash Back Responsible Use

If you want a simple system that keeps rewards in their lane, here it is. Four steps, no overthinking required.

Step | Title | Description | Key Focus |

1 | Budget First | Set your monthly gas & grocery budget BEFORE you swipe. | Proactive Planning |

2 | Swipe Smart | Use your Arro Card only on planned purchases. | Intentional Spending |

3 | Check Daily | Open the Arro app. 2 minutes. Stay on track. | Consistency |

4 | Stack Wins | Cash back + low utilization + on-time payments = credit building habits. | Long-term Growth |

Step one: budget first. Before the month starts, know how much you plan to spend on gas and groceries. This is your spending cap; rewards don’t change it.

Step two: swipe smart. Use your Arro Card for those planned gas and grocery purchases. That’s where you earn 1% cash back, and that’s where you stop. No “might as well” purchases.

Step three: check daily. Open the Arro app for 2 minutes and review what you spent yesterday. This tiny habit is the difference between staying on track and realizing two weeks later that you’ve blown your budget. Arro Insights makes this stupid easy - it’s all right there.

Step four: stack your wins. Cash back is just one piece. When you combine responsible spending with low utilization and on-time payments (AutoPay handles that), you’re not just earning rewards, you’re building credit history. That’s where the real value is.

Let’s Talk Numbers: When 1% Actually Adds Up

One percent doesn’t sound like much. And honestly? On any single purchase, it isn’t. But here’s where it gets interesting.

Spending Scenario | Monthly Calculation | Cash Back (1%) | Outcome |

Normal Gas Spending ($50/week) | $50 x4 weeks = $200$ | $2.00 back | Success: You needed gas anyway. Free $2. |

Normal Grocery Spending ($75/week) | $75 x4 weeks = | $3.00 back | Success: Groceries you'd buy regardless. |

Extra Spending ("For the points") | $40 extra per | $0.40 back | Loss: You lost $39.60 chasing rewards. |

Say you spend about $200 a month on gas and $300 on groceries. That’s $500 in essentials, money that’s leaving your account no matter what. With 1% cash back, that’s $5 a month. Over a year, that’s $60 back in your pocket for purchases you were making anyway. Not life-changing, but not nothing either.

Now compare that to someone who spends an extra $50 a month chasing rewards, buying premium products, adding impulse items, and filling up more often than needed. Their extra $50 earns them $0.50 in cash back. Over the past year, they’ve spent an extra $600 to earn $6. That’s a net loss of $594.

The math is clear: responsible cash back use means keeping your spending flat and letting rewards be a passive perk. The second you increase spending to increase rewards, you lose.

➡️ Want cash back that works with your budget, not against it? The Arro Card gives you 1% cash back on gas & groceries with no annual fee. Download the Arro app to get started.

How The Arro App Keeps You Honest

Knowing the right approach is one thing. Actually sticking to it? That’s where most people struggle. And that’s exactly why having the right tools matters.

The Arro app isn’t just for checking your balance. It’s where you see your spending patterns, track how close you are to your utilization limit, and get real-time insights that keep you from drifting into overspending territory. Think of it as a reality check that takes two minutes a day.

Then there’s Artie, your AI Money Coach. Wondering if that Costco run will push you over budget? Ask Artie. Curious whether paying your statement early helps your credit? Artie’s got you. Available 24/7, no judgment, answers that actually make sense for your situation.

And here’s something that ties it all together: with Arro, your cash back isn’t just about rewards. It’s part of a bigger picture. Every responsible swipe contributes to your payment history, which is reported to credit bureaus. Every month of low utilization strengthens your credit profile. The cash back is a nice perk, but the real reward? That’s the credit history you’re building.

No hard credit check required to apply. No deposit. No hidden fees. Just a card designed to reward the spending you’re already doing while helping you build toward something bigger.

➡️ Ready to earn cash back the smart way? Download the Arro app for free. Your spending insights, AI coaching, and credit-building tools - all in one place.

FAQ

What does cash back responsible use actually mean?

Cash back responsible use means earning rewards only on purchases you’d make, regardless - like gas and groceries - without increasing your spending to chase more rewards. It’s about letting Arro points be a passive bonus, not a reason to buy more.

How can I avoid overspending with a cash back card?

Set a monthly budget for your cash back categories before you start spending. Use the Arro app to check your spending daily - just 2 minutes keeps you aware. And always ask: “Would I buy this without the reward?” If not, skip it.

Is 1% cash back even worth it?

On its own, 1% is modest. But on spending you’re doing anyway - like $500/month on gas and groceries - it adds up to about $60 a year with zero extra effort. Combined with building credit history through the Arro Card, the total value is way bigger than the cash back alone.

Does the Arro Card have an annual fee?

The Arro Card has a low annual fee, no deposit required, and no hard credit check to apply. You earn 1% cash back on gas & groceries with no hidden costs.

Can cash back actually hurt my credit?

Cash back itself doesn’t hurt your credit. But overspending to earn more rewards can increase your utilization, which may negatively affect your score. Keeping your balance low relative to your credit limit is key; the Arro app helps you track it in real time.

How does the Arro app help me use cash back responsibly?

The Arro app gives you daily spending insights, utilization tracking, and access to Artie - your AI Money Coach - who provides personalized tips. It’s designed to help you stay within budget while earning rewards on purchases you’d already make.

Resources

National Library of Medicine. Spendception: The Psychological Impact of Digital Payments on Consumer Purchase Behavior and Impulse Buying