Table Of Content

Why Arro Stands Out

Quick Decision Guide

Comparison Table

Kikoff Overview

Dovly Overview

Arro Overview

Final Verdict

FAQ

This guide provides an honest, side-by-side comparison of features, pricing, and what makes each service unique, so you can decide which option aligns with your credit-building goals.

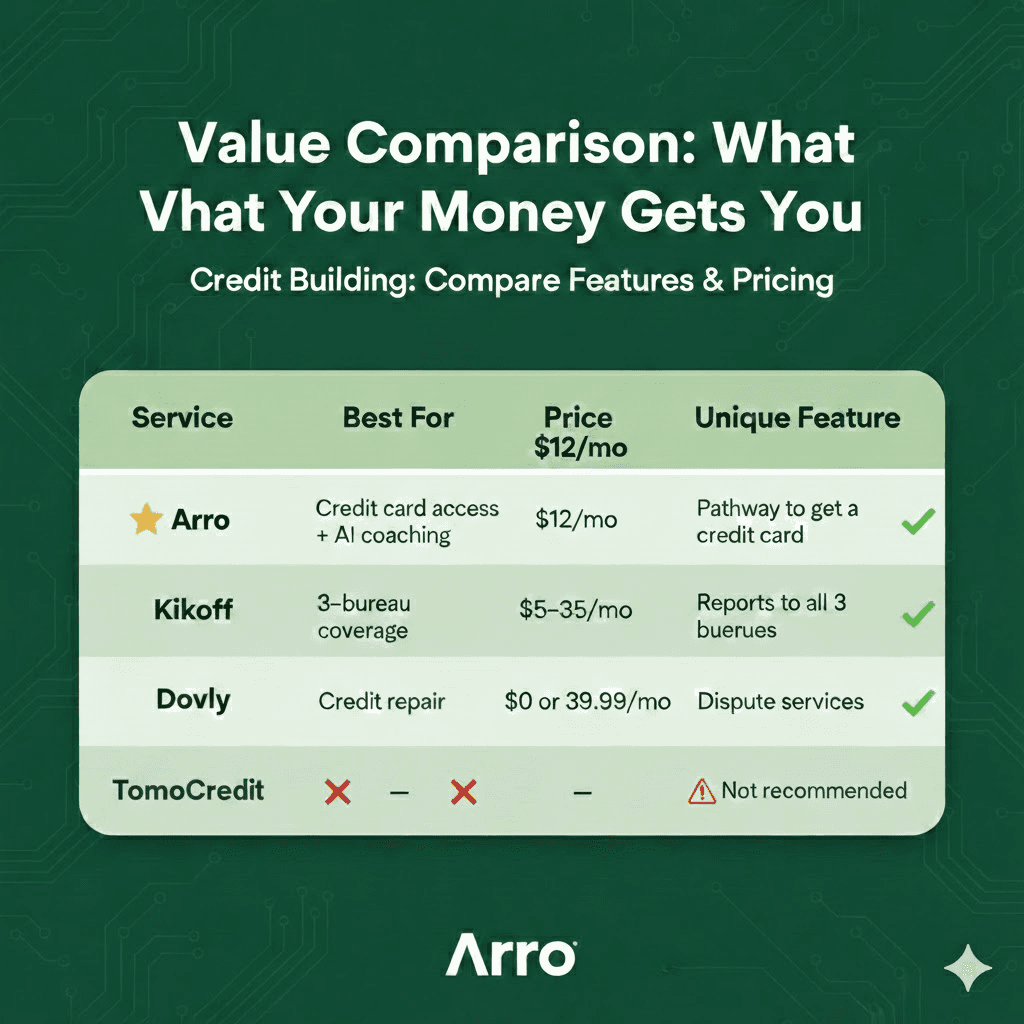

Arro ($12/mo) stands out as the only credit builder offering a pathway to an actual revolving credit card, a meaningful edge over tradeline-only competitors.

Kikoff ($5/mo) offers the lowest price and 3-bureau reporting, but lacks coaching, card access, and has documented cancellation issues.

Dovly ($39.99/mo) is best suited for credit repair via automated disputes, not straightforward credit building.

TomoCredit has significant red flags, legal issues, an F BBB rating, and persistent complaints, making it a risky choice.

All credit builders require consistent on-time payments over 6–12 months; none are quick fixes.

Arro's included AI coach (Artie) and built-in financial education add long-term value beyond just reporting a tradeline.

What Is A Credit Builder Program?

A credit builder program helps you establish or improve your credit by reporting your payment activity to credit bureaus. Unlike traditional credit cards that require existing credit, these programs focus on building payment history from scratch.

Credit builder subscriptions work by providing a tradeline that appears on your credit report. When you make monthly payments, the service reports this activity to one or more major credit bureaus: Experian, Equifax, and TransUnion. Over time, this consistent payment history can positively impact your credit score.

These programs aren't quick fixes. Credit building takes months of consistent, on-time payments to show meaningful results. Most users see initial changes within 30-60 days, with more substantial progress appearing over 6-12 months.

At a Glance

Why Arro Credit Builder Stands Out

After comparing the top credit builders available in 2026, Arro Credit Builder emerges as the most comprehensive solution for one critical reason: it's the only service that provides a pathway to actual revolving credit through the Arro Card. Here's why that matters:

Access to the Arro Card – The Clear Differentiator

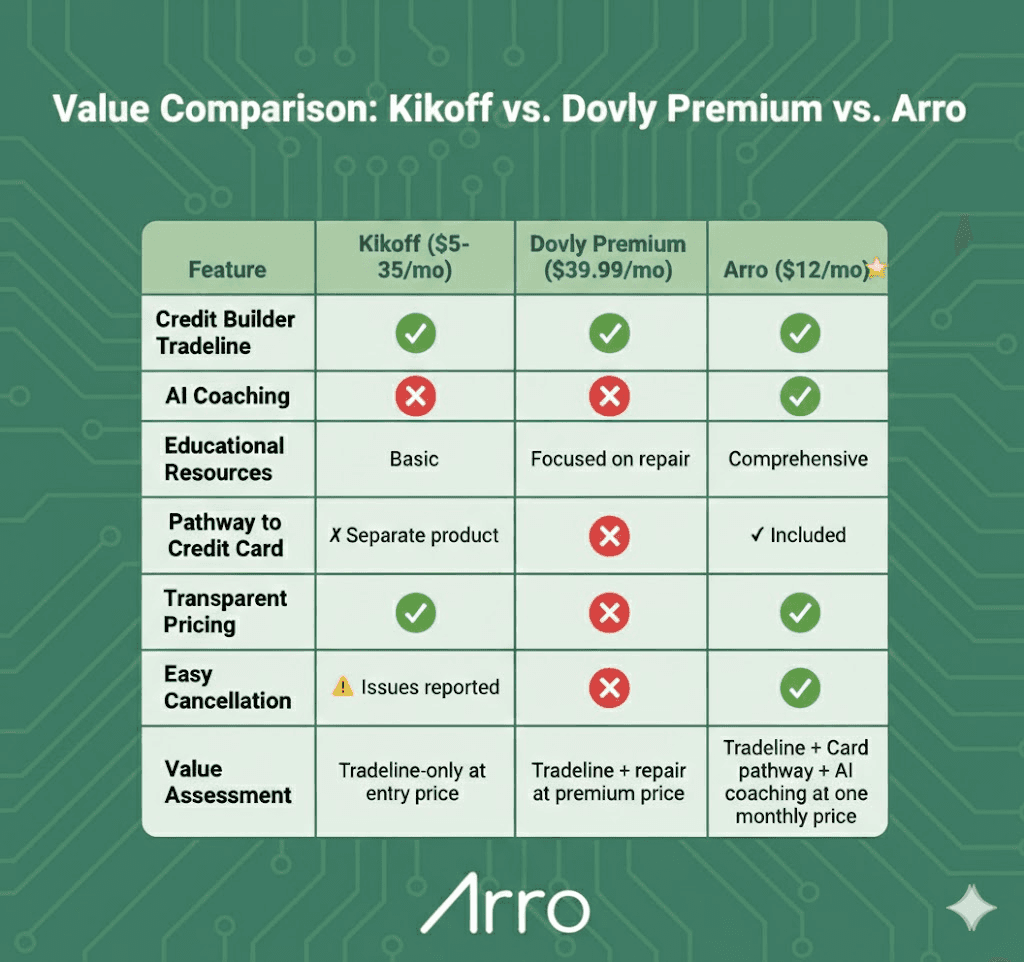

Unlike other credit builders that only report a tradeline, Arro Credit Builder creates a pathway to the Arro Card, an actual revolving credit card. This is a fundamental difference that may help build your credit more effectively than tradeline-only products. While competitors help you build payment history, Arro positions you for access to real revolving credit, which may have a more substantial impact on your credit profile.

Kikoff offers a secured card, but it's a separate product with additional barriers. Dovly and most other credit builders don't offer card access at all.

24/7 AI Financial Coaching – Included at No Extra Cost

Meet Artie, your AI money coach. Get instant answers to credit questions, personalized budgeting advice, and recommendations tailored to your financial situation, available anytime you need guidance. No other credit builder in this comparison offers intelligent, always-available coaching without additional fees.

Ongoing Access to Your Credit Score

Arro provides ongoing access to your credit score and score factors directly in the app. While credit scores typically update monthly when bureaus receive new data (regardless of which service you use), you always have transparent access to understand where you stand and what's affecting your credit.

Transparent, Mid-Tier Pricing

At $12/month, Arro sits between budget options like Kikoff ($5/mo) and premium-priced services like Dovly ($39.99/mo). You get AI coaching, educational resources, and Arro Card pathway access, features that competitors either don't offer or charge significantly more for.

Educational Focus

Arro doesn't just help you build credit mechanically, it helps you understand why credit works the way it does through built-in resources, real-time insights, and AI coaching. This knowledge serves you for life, not just during your subscription.

Easy Management and Cancellation

Month-to-month flexibility means you can cancel anytime without jumping through hoops. No long-term contracts, no cancellation nightmares, unlike some competitors with documented cancellation difficulties.

Built on Trust & Transparency

✓ No credit check required to sign up

✓ No hidden fees or surprise charges

✓ Cancel anytime, no hassle

✓ Reports to Experian and Equifax monthly

✓ FDIC-insured through Cross River Bank partnership

Value Comparison: What Your Money Gets You

Bottom Line: Arro delivers comprehensive features at a fair price point, with unique capabilities no competitor offers at any price.

Kikoff Credit Builder Review: 3-Bureau Coverage At $5/Month

Kikoff offers credit accounts starting at $5/month with tradelines of $750 or $2,500. The service reports to all three major credit bureaus (Experian, Equifax, TransUnion), which provides comprehensive credit coverage.

Reported Results:

Average reported credit improvement of 58 points for users who make on-time payments*

Average reported credit improvement of 86 points for users starting under 600 within one year with on-time payments*

Average first-month reported impact of +25 points for users starting below 600*

*Source: Kikoff claims. Individual results may vary.

Pricing:

Basic Plan: $5/month

Premium Plan: $20/month

Ultimate Plan: $35/month

What's Included:

$750 or $2,500 tradeline (depending on plan)

Reports to all three credit bureaus

Monthly credit reports and score updates

Credit can only be used in Kikoff's store for e-books and courses

Premium/Ultimate plans include rent reporting, dispute tools, and identity theft protection

Considerations:

The credit line can only be used in Kikoff's proprietary store, limiting practical utility. Multiple user reviews report difficulties with cancellation and customer service response times. Some users have experienced unexpected membership fees.

What Kikoff Doesn't Offer

While Kikoff provides comprehensive bureau reporting, it lacks several features that credit builders may benefit from:

There's no AI coaching to help you understand credit decisions, no pathway to a real credit card included in the credit builder subscription (their secured card is a separate product with additional requirements), and multiple users report difficulties canceling their subscriptions.

If you need basic credit building with 3-bureau coverage and are comfortable with these limitations, Kikoff may work for your needs, but you'll miss out on the educational guidance and integrated card access that can support your credit journey.

Dovly AI Review: Credit Repair + Building At $39.99/Month

Dovly offers free and premium plans focused on credit building and repair. The service provides AI-powered credit dispute and report submissions.

Reported Results:

Average reported improvement of 82-93 points for Premium members enrolled 6+ months (as of December 2025)*

Many users report beginning to build a credit within the first 30 days

*Source: Dovly claims. Individual results may vary.

Pricing:

Free Plan: $0

Premium Plan: $39.99/month or $99.99/year

What's Included:

Free Plan:

Monthly TransUnion credit score and report

Manual dispute selection with TransUnion only

Basic credit monitoring

Premium Plan:

$2,000 tradeline reported to Experian and Equifax (Note: The tradeline is only available with the Premium plan, not the free version)

Rent, telecom, and utility bill reporting (up to 24 months of on-time payments)

AI-powered automated disputes with all three bureaus

Real-time credit monitoring

$1 million identity theft insurance

Weekly TransUnion report and score

Considerations:

Like Arro, Dovly reports the tradeline to two major credit bureaus (Experian and Equifax) rather than all three.

The free plan does not include the $2,000 tradeline or multi-bureau reporting, those features require the Premium subscription. The Premium plan focuses heavily on credit repair through automated disputes alongside credit building.

What Dovly Doesn't Offer:

Dovly excels at credit repair through disputes, but its credit builder component is secondary to its repair focus.

At $39.99/month, it's more than 3x the cost of Arro, and it doesn't provide any pathway to a real credit card, meaning you're building credit but not positioning yourself for the revolving credit that lenders often value.

If you have errors to dispute and can afford the premium, Dovly's dispute services may be valuable. However, if you're primarily focused on building credit (not repairing it), you may be paying for features beyond your needs.

TomoCredit Overview

TomoCredit was designed for those without a traditional credit, offering no-credit-check approval. However, the service has faced significant operational challenges.

Documented Issues:

In 2023, TomoCredit was sued by Silicon Valley Bank after defaulting on its debt facility, according to court filings uncovered by Fintech Business Weekly

Better Business Bureau F rating with hundreds of complaints

BBB alert issued in 2020 for customer service difficulties, with issues persisting through 2026

Industry analysis suggests certain credit builder tradelines may not provide the signals some lenders look for

Common User Complaints:

Inability to cancel subscriptions despite repeated requests

Continued charges after requesting cancellation

No phone support (email only) with inconsistent response rates

Inconsistent reporting to credit bureaus

Unauthorized withdrawals from bank accounts

Customer service conversations being deleted when refund requests are made

Pricing (if operational):

Monthly card fee: $2.99/month

TomoBoost credit builder product: $15-$170/month range

Recommendation:

Given documented legal challenges, persistent customer service issues, and operational disruptions dating back to 2023, we recommend exploring alternative credit builders with more reliable track records. While TomoCredit appears to still be operating as of January 2026, the volume and consistency of user complaints raise concerns about service reliability.

Arro Credit Builder Review: Card Access + AI Coaching AI $12/Month

Arro Credit Builder is a $12/month subscription that automatically reports your payment history to Experian and Equifax. The service emphasizes transparency, education, and a unique pathway to actual revolving credit through the Arro Card.

What's Included:

$2,000 reported tradeline

Ongoing access to your credit score and score factors in the app

AI coaching with Artie available 24/7 for credit questions

Budgeting insights to understand spending patterns

Real-time credit insights

Financial education resources

Flexible month-to-month plans (annual option available)

Pricing:

$12/month with transparent, straightforward pricing. No hidden fees.

Considerations:

Like Dovly, Arro reports to two major credit bureaus (Experian and Equifax) rather than all three. Results vary by individual and depend on the overall credit profile. Building credit takes consistent time regardless of service.

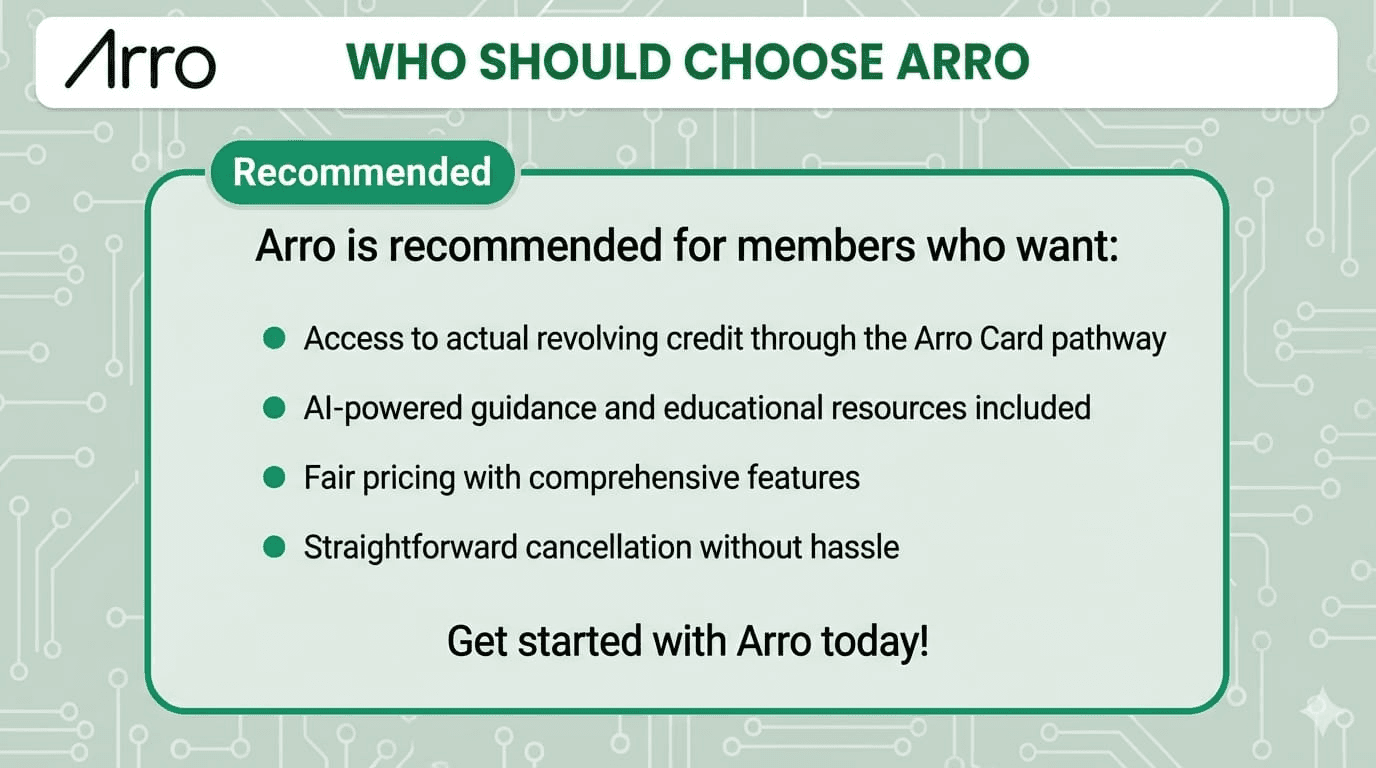

Best For:

Users who want a pathway to actual revolving credit (not just a tradeline), value AI-powered financial guidance, and prefer transparent educational resources during their credit-building journey.

For a detailed comparison of Arro's advantages, see the "Why Arro Credit Builder Stands Out" section above.

Arro Credit Builder Overview

Arro Credit Builder is a $12/month subscription that automatically reports your payment history to Experian and Equifax. The service emphasizes transparency, education, and a unique pathway to actual revolving credit through the Arro Card.

What's Included:

$2,000 reported tradeline

Ongoing access to your credit score and score factors in the app

AI coaching with Artie available 24/7 for credit questions

Budgeting insights to understand spending patterns

Real-time credit insights

Financial education resources

Flexible month-to-month plans (annual option available)

Pricing: $12/month with transparent, straightforward pricing. No hidden fees.

Key Differentiators:

Pathway to the Arro Card: While Arro Credit Builder isn't required to apply for the Arro Card, it can help develop the payment history that supports future approval. This is the only credit builder in this comparison that provides access to an actual revolving credit card, which may help build your credit more effectively than tradeline-only products.

AI financial coaching: Get personalized guidance from Artie on credit questions, budgeting, and financial decisions, 24/7 availability with no additional cost.

Educational focus: Built-in resources help you understand the "why" behind credit, not just the mechanics of building it.

Transparent pricing: Flat $12/month with no variable pricing or upsells.

Easy cancellation: Month-to-month flexibility with straightforward cancellation process.

Considerations: Like Dovly, Arro reports to two major credit bureaus (Experian and Equifax) rather than all three. Results vary by individual and depend on overall credit profile. Building credit takes consistent time regardless of service.

Best For: Users who want a pathway to actual revolving credit (not just a tradeline), value AI-powered financial guidance, and prefer transparent educational resources during their credit-building journey.

Bottom Line: Arro delivers comprehensive features at a fair price point, with unique capabilities no competitor offers at any price.

Final Verdict: Which Credit Builder Should You Choose?

After a comprehensive comparison of features, pricing, and real-world considerations, Arro Credit Builder stands out as the most comprehensive choice for building credit in 2026.

Why Arro is the recommended choice:

Unique Card pathway - The only credit builder that positions you for actual revolving credit through the Arro Card

Best value proposition - Fair pricing ($12/mo) with premium features (AI coaching, educational resources, credit card access)

Comprehensive approach - Not just mechanical credit building, but financial education and guidance

Transparent and reliable - No hidden fees, straightforward cancellation, consistent service

For most people building credit, Arro offers the most balanced combination of features, value, and long-term credit-building support.

Ready To Build Credit The Right Way?

Arro Credit Builder offers what no other service can: a pathway to the Arro Card, AI-powered guidance, and transparent pricing, all for $12/month.

Don't settle for tradeline-only products. Start building credit that opens doors.

No hidden fees. Cancel anytime. Build credit history starting today.

FAQ

Is Arro really the best credit builder?

We think so (obviously, we built it!), but "best" depends on what you need. Arro gives you the most complete package: AI coaching, budgeting insights, educational resources, and the only pathway to a real credit card, all for $12/month.

If you need three-bureau reporting and the absolute lowest price, Kikoff might work better at $5/month. If you have errors to dispute, Dovly's $39.99/month Premium plan focuses on repair.

But for comprehensive credit building with guidance and card access? Arro's your best bet.

Why does Arro cost more than Kikoff but less than Dovly?

Kikoff costs less ($5/mo) because it's tradeline-only—no coaching, no card pathway, no advanced education. Dovly costs more ($39.99/mo) because they focus on credit repair with dispute services.

Arro sits at $12/month because we're giving you more than just a tradeline (AI coaching, card pathway, budgeting insights, education) without charging premium-repair prices.

Do I really need AI coaching, or is that just a gimmick?

Artie gives you instant answers to questions like "Why did my score drop?" or "Should I pay off my balance?" without waiting for customer service or Googling.

Could you build credit without it? Sure. But it's easier when you've got help that doesn't judge and doesn't sleep.

Will this hurt my credit?

Nope! There's no hard credit check to sign up, so joining Arro won't ding your score.

As long as you make your payments on time, you're building credit, not hurting it. The only way it would hurt is if you missed payments or didn't pay your subscription—but that's true of any credit product.

What happens if I miss a payment?

Missing a payment could get reported to the credit bureaus and might negatively impact your score. That's why it's important to only sign up if you can comfortably afford the $12/month.

If you're ever in a tight spot, reach out to us before missing a payment. We're humans on the other end, and we'd rather help you figure it out than see you hurt your credit.

What's this "pathway to the Arro Card" thing? Do I have to get the card?

Nope, you don't have to get the Arro Card. The "pathway" just means we're building your payment history in a way that supports future card approval if you want it.

Most credit builders give you a tradeline, and that's it. Arro positions you for actual revolving credit, which is what lenders really care about. When you're ready to apply for the Arro Card, you've already built the foundation with us.

Can I really cancel anytime, or is that one of those "technically true but actually hard" things?

No tricks here. You can cancel anytime, genuinely. No phone calls required, no "are you SURE?" emails, no 30-day wait periods.

We're month-to-month. When you're done, you're done.

Is my money safe with Arro?

Yes. Credit builder lines of credit are provided by Cross River Bank, which is FDIC-insured. We're a financial technology company partnering with a real, regulated bank to make sure everything's safe and above board.

Important Information

On-time payment history may have a positive impact on your credit score. Late payment may negatively impact your credit score. We report payment history to Experian and Equifax. Credit impact may vary based on a number of factors including your activity with other financial services organizations.

Upward is a financial technology company, not an FDIC-insured bank. Credit builder lines of credit provided by Cross River Bank, Member FDIC. Line of credit is not a deposit product.