Ian Quetglas

Table Of Content

Be The CEO Of Your Finances

Set Your Short-Term And Long-Term Goals

Consider Multiple Budget Scenarios

Create A Realistic Budget That Reflects Your Current Situation And Future Goals

Go Out And Live Your Financially Planned Life

Build Your Budget And Your Credit With Arro

FAQs

Forget previous financial strategies that haven't worked. You have the opportunity to finish this holiday season with a sound budget and start 2026 with a fresh perspective on managing your finances. Recent data show that average annual expenditures for all consumer units were $78,535, underscoring the importance of budgeting.

Don't be intimidated by a budget. All the information you need is in your head, bank account, or credit card statements. Budgeting is not complicated. It's all about understanding the money coming in and out of your accounts and planning to meet your goals.

In this article, we'll walk through five practical steps that can help you create a realistic budget, set achievable goals, and discover tips for saving money that fit your life.

Key Takeaways

Assess your finances like a CEO, understand your income, expenses, assets, and debts before creating any plan.

Set both short-term (1-year) and long-term goals with clear metrics to track your progress.

Plan for multiple scenarios, best case, worst case, and most probable, to prepare for uncertainty.

Build a realistic budget that reflects your current situation while supporting your future goals.

Take action immediately. A good plan executed today beats a perfect plan that never happens.

Be The CEO Of Your Finances

Before taking any action, you must assess your situation. It helps me think about my financial situation the way I would look at a business. That helps me ask tough questions and separate emotions from the exercise. One of the main reasons people don't create a budget is that they fear what they might see under the hood. However, to properly create a path forward, it will be important to ask the tough questions and face reality with a solid plan. Let's rip that band-aid!

Ask yourself some questions to get you going:

Have I made any spending mistakes during the holidays?

How did my financial situation look for the whole year?

Was I able to cover all my expenses without needing debt?

These questions help you summarize what's most important, how much you spent during the past year, and how you can improve next year with effective tips for saving money.

You will need a summary of your financial activity for the year. You can find this information on your bank or credit card statements, or you may know it by memory. This will help you understand where you stand and develop an effective plan to get where you want to be.

Like a business, list your income, expenses, and things you own and owe. What you own might be more than what you think, so include anything you can sell! Think about your car, clothes, jewelry, savings, etc.

Once you have a clear picture of your financial situation this year, you can identify potential issues and where you will need to make adjustments. These tips for saving money start with honest self-assessment and a clear view of your financial reality.

Set Your Short-Term And Long-Term Goals

Once you have a good idea of where you stand, you need to consider where you want to be. You should divide your goals into short-term and long-term. Your short-term goals should be achievable within 1 year and position you to successfully achieve your long-term goals, which should be your aspirations. Additionally, short-term goals should focus on addressing obstacles that could prevent you from achieving your long-term goals, such as debt repayment or improving your credit score.

After assessing your situation, you will have enough ammunition to develop impactful goals. For example, this can be a short list of goals of someone looking to save more to buy a house in the future:

Build an emergency fund covering three months of expenses

Pay down high-interest debt to improve credit utilization

Save for a down payment by setting aside a specific amount monthly

Understanding your goals as the starting point will give you a purpose and measurable metrics to evaluate your progress throughout the year.

To help plan for 2026, we'll focus on short-term goals and how your financial planning guide can help you achieve them. These tips on saving money work best when tied to specific, measurable objectives that keep you motivated throughout the year.

Consider Multiple Budget Scenarios

It's okay to be pessimistic for a second! Think about the best-case, worst-case, and most probable scenarios as you try to understand how everything will play out in the future. This will help you understand how much room you have to deviate from the plan and how quickly you can get back on track. During this activity, consider how the economy is doing and how it might look next year.

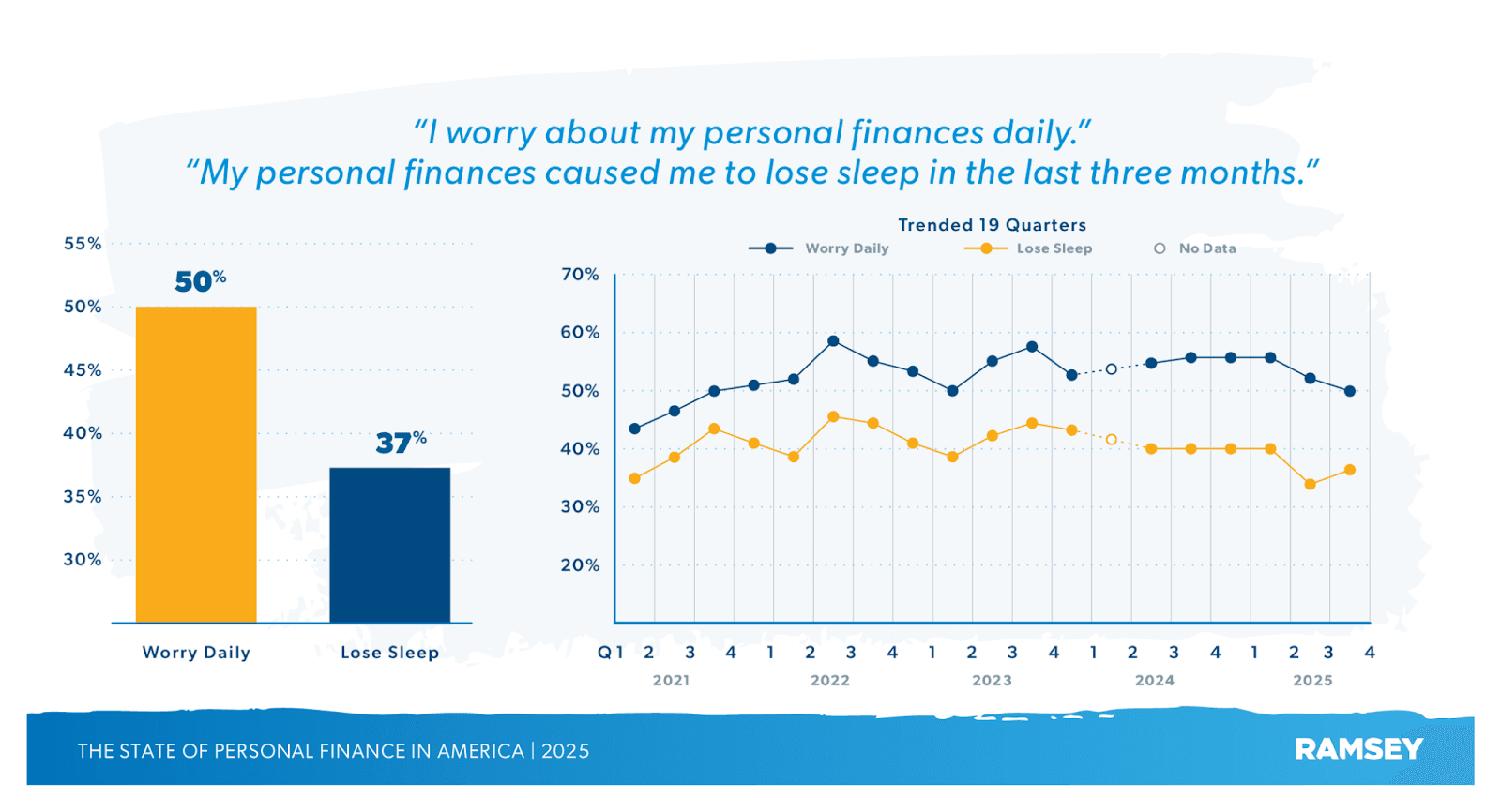

According to recent research, 50% of U.S. adults worry daily about their personal finances, showing that financial uncertainty is widespread.

Source: Ramsey Solutions

Having all the answers is impossible, but scenario planning can help you prepare for any situation. For example, it might be important to have extra savings just in case you can no longer rely upon your income from other activities if the economic downturn makes it harder for that second job to provide you with that opportunity.

Think about what line items in your personal assessment can change and by how much:

Best case: Income increases, all expenses stay stable or decrease

Most probable: Income stays steady, some expenses increase moderately

Worst case: Income decreases, or job loss occurs, and expenses rise significantly

By doing this, you will identify which actions move you toward your goals and discover practical tips for saving money along the way.

Assessing how the key drivers of your budget may change will help you create the most realistic budget. These are the metrics you can track as you implement your budget. It would be ideal if you had a case where everything that could go wrong did, and you had a safety plan to address it.

Create A Realistic Budget That Reflects Your Current Situation And Future Goals

Congratulations! You can now create a realistic budget by considering your current financial situation, understanding where you want to be, and accounting for multiple scenarios. Now it's time to create your 2026 budget!

Fifty-one percent of adults reported spending less than their income in the past month, which means having a margin in your budget is achievable.

Source: Federal Reserve System

Laying out and visualizing your budget in whatever format works for you will be the most time-consuming part of creating your plan, but having completed the previous work makes it much easier.

Add all the expenses from 2025 that you expect you'll still have, and think about what can change in the future based on your situation and your goals:

Fixed expenses: Rent or mortgage, insurance, loan payments

Variable expenses: Groceries, utilities, gas

Discretionary spending: Entertainment, dining out, subscriptions

Savings goals: Emergency fund, retirement, specific purchases

This is where practical money-saving tips become essential in your planning guide, helping you identify areas to cut back.

This might take a little bit of time, but you're almost there! Remember, these money-saving tips should fit your lifestyle while still challenging you to improve your financial habits.

Go Out And Live Your Financially Planned Life

The great thing about having your budget is that you'll start seeing how all your finances evolve and where you need to focus your attention. But for now, you've done the hard work, so it’s time to execute on your plan! George Patton, a great general, once said he would always choose a good plan perfectly executed today rather than a perfect plan executed next week.

Most people stay in the planning stage and never fully execute their plans, but the only way to meet their financial goals is to take action.

Here are final tips for saving money as you implement your budget:

Track your spending weekly to stay accountable

Review and adjust your budget monthly based on actual expenses

Celebrate small wins to maintain motivation throughout the year

Stay tuned for more insights on the best ways to track and monitor your budget. Remember, the journey to financial wellness starts with a solid plan, and these money-saving tips will help you lay the foundation for a stronger financial future.

These actionable tips for saving money will help you stay on track and make continuous progress toward your financial goals.

Also read:

Pass The Deposit: How Credit Impacts Security Deposits, Utility Bill Deposits, And Phone Plans

Streaming, Subscriptions, And Small Bills: Which Ones Can (And Can’t) Help Your Credit?

Balance Transfer Or Personal Loan: What Is The Right Fit For You?

Build Your Budget And Your Credit With Arro

Creating a realistic budget is the foundation of financial wellness; it helps you understand where your money goes, set achievable goals, and make smarter decisions throughout the year. By honestly assessing your finances, planning for multiple scenarios, and taking action on your plan, you're setting yourself up for long-term success.

At Arro, we believe building credit shouldn't be confusing, expensive, or out of reach. That's why we've created a credit card that supports you in learning, earning, and building credit, all seamlessly integrated within a single app. With no hard credit checks, no deposit, and 1% cash back on gas and groceries, Arro makes it simple to start improving your credit while rewarding your everyday spending.

You'll also get access to Artie, your personal AI Money Coach, who's there 24/7 to answer questions, celebrate wins, and help you make smart financial moves. Every on-time payment, every lesson, every small step forward helps you unlock higher credit limits and better credit health. Thousands of Arro members are already building stronger credit and having fun doing it.

Ready to start your own journey? See how easy it can be to build credit with confidence while mastering your budget.

FAQs

How do I handle irregular income while maintaining a budget?

Calculate your average monthly income from the past 6-12 months as your baseline. Build a larger emergency fund (6 months instead of 3) to cover lean months. Use percentage-based allocation rather than fixed amounts; this gives flexibility while maintaining structure. During high-earning months, set extra funds aside in a buffer account.

What's the difference between budgeting and financial planning?

Budgeting is tactical, month-to-month management of income and expenses, your daily money roadmap. Financial planning is a broader long-term strategy including retirement, investments, insurance, and estate planning. Think of budgeting as the foundation supporting your larger financial planning structure; you can't build wealth without mastering where money goes monthly.

Should I adjust my budget categories based on seasonal changes?

Your budget should reflect actual spending patterns. Utility costs spike in summer or winter, holiday spending increases in November and December, and back-to-school expenses hit late summer. Review past year's spending to identify seasonal trends, then build them into monthly projections. Some create "sinking funds”, setting aside money monthly for predictable annual expenses.

How can I stay motivated to stick to my budget when I feel restricted?

Reframe budgeting from restriction to empowerment; you're choosing how to use money for goals that matter. Build in a "fun money" category for guilt-free spending. Visualize progress with charts showing debt decreasing or savings growing. Find an accountability partner or join a budgeting community. Most importantly, tie every category back to personal values.

What percentage of my income should go toward different budget categories?

While the 50/30/20 rule (50% needs, 30% wants, 20% savings) is popular, your breakdown depends on location, income level, and life stage. High cost-of-living areas might need 60% for needs. If aggressively paying debt, flip to 50/20/30. Ensure essential expenses don't exceed 50-60% of take-home pay, and you're saving at least 15-20%.