Table Of Contents

Does Brigit Report To Credit Bureaus? The Short Answer

How Credit Bureau Reporting Actually Works

What Brigit Reports (And What It Doesn’t)

How Other Credit Builder Brands Compare

Why Arro Credit Builder Is A Strong Alternative

What To Look For In Credit Building Apps

FAQ

If you’re looking into credit-building apps, one of the first questions you probably have is: Does Brigit report to credit bureaus? It’s a fair question, and honestly, the answer matters more than most people realize.

Because here’s the thing: a credit builder only helps your score if it actually reports your payment activity to the bureaus.

And not all services report to the same ones. Some report to one bureau, some report to two, and a few report to all three. Where your data shows up determines which lenders can see your progress, and that directly affects what you qualify for.

This guide explains how Brigit’s credit reporting works, how it compares to other credit builder brands such as the Arro Credit Builder, Kikoff, Cred.ai, and Ava, and what to look for when choosing the right service for your goals.

Key Takeaways

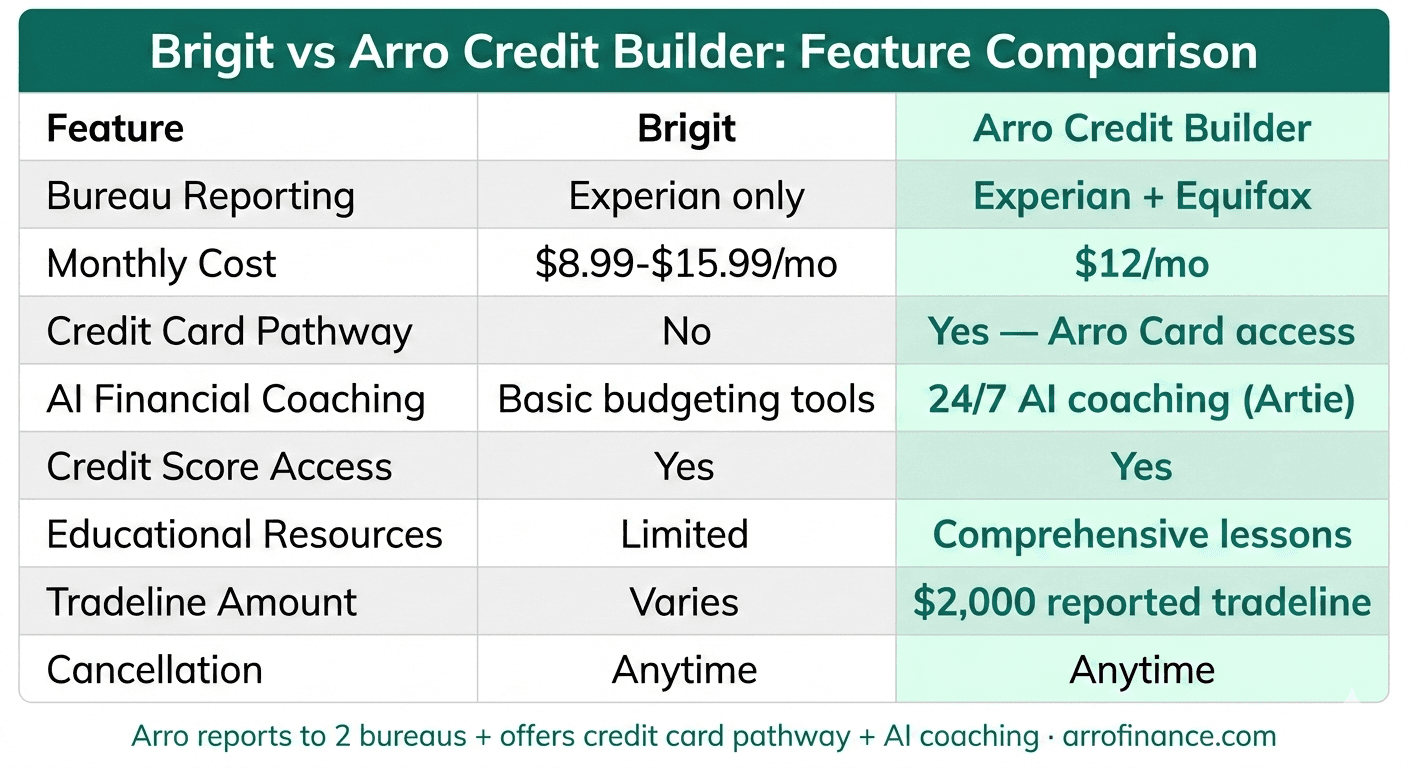

Does Brigit report to credit bureaus? Yes - Brigit reports to Experian only, not to Equifax or TransUnion.

Single-bureau reporting means lenders who pull from Equifax or TransUnion won’t see your Brigit payment history.

The Arro Credit Builder reports to both Experian and Equifax, offers a $2,000 tradeline, 24/7 AI coaching, and a pathway to the Arro Card - features that most credit builder brands don’t match.

When comparing credit-building apps, look at which bureaus they report to, whether they offer real credit card access, and what educational support is included.

No credit builder is a quick fix. Meaningful results come from consistent on-time payments over 3 to 12 months, regardless of which service you use.

Does Brigit Report To Credit Bureaus? The Short Answer

Yes, Brigit does report to credit bureaus - but only to one. Brigit’s Credit Builder feature reports your monthly payment activity to Experian. It does not report to Equifax or TransUnion.

This matters because different lenders pull your credit from different bureaus. If a lender checks your Equifax report and your Brigit payments only show on Experian, they won’t see that history. Your effort is real, but it’s only visible to some lenders.

So does Brigit report to credit bureaus in a way that fully covers you? Partially. You’re building payment history, which is good. But single-bureau reporting leaves gaps that could affect your approval odds depending on which bureau a lender checks.

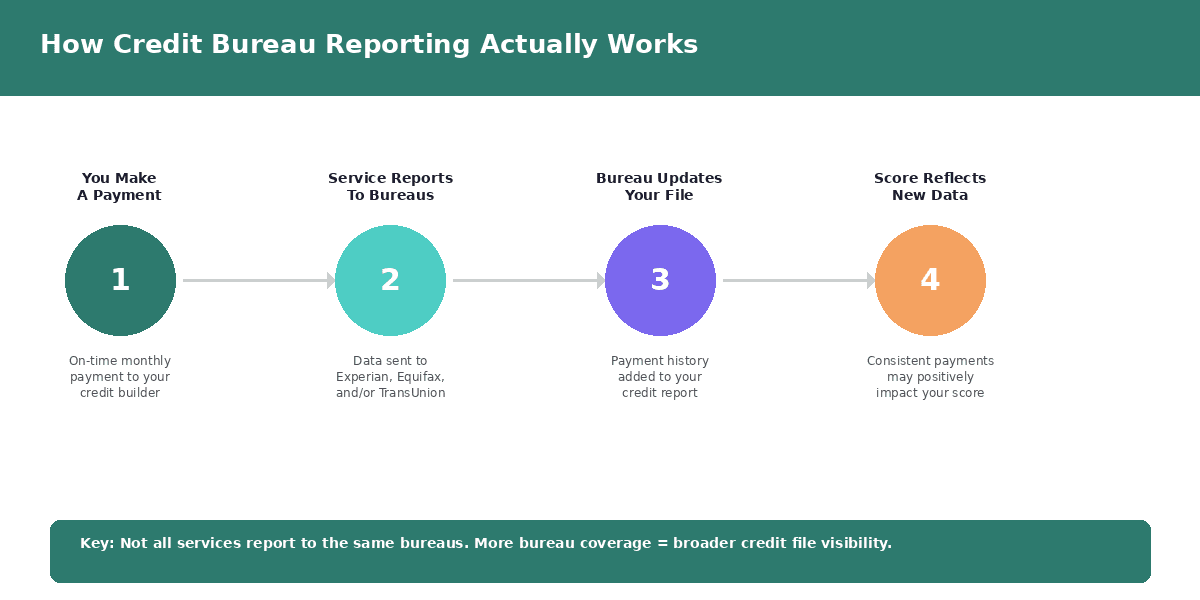

How Credit Bureau Reporting Actually Works

Before comparing specific services, it helps to understand how credit bureau reporting works in general. This is the foundation that determines whether all credit builder brands are useful or limited.

When you make a payment to a credit builder service, that service sends data to one or more of the three major credit bureaus: Experian, Equifax, and TransUnion. The bureau then adds that payment record to your credit file.

Over time, consistent on-time payments build a positive payment history, which is the single biggest factor in your credit score.

The key detail: each bureau maintains a separate file on you. A payment reported to Experian doesn’t automatically appear on your Equifax or TransUnion reports. That’s why the number of bureaus a service reports to matters. More coverage means more lenders can see your progress.

Most people researching AI credit repair or credit-boosting apps assume that all services report to all three bureaus. They don’t. And that assumption can cost you if you’re applying for a loan or card that pulls from a bureau your service doesn’t report to.

What Brigit Reports (And What It Doesn’t)

Now that we’ve covered the basics, let’s get specific about Brigit. Here’s what Brigit's credit bureau reports actually look like in practice.

Brigit’s Credit Builder creates an installment-style tradeline and reports your monthly payments to Experian. This shows up on your Experian credit report as a consistent payment history. Making on-time payments can positively influence your Experian-based credit score over time.

What Brigit doesn’t do: it doesn’t report to Equifax or TransUnion. It doesn’t offer a pathway to a real credit card. And its educational tools, while present, are more basic budgeting features than comprehensive credit education.

Brigit’s pricing ranges from $5.99 to $9.99 per month, depending on the plan. For single-bureau reporting and basic budgeting tools, that’s competitive on price, but it means you’re building visibility on only one of three bureaus.

How Other Credit Builder Brands Compare

Brigit isn’t the only option. If you’re comparing the best credit builder apps, here’s how other services stack up - especially on the reporting question that matters most.

Kikoff

Kikoff reports to all three bureaus, which is its strongest selling point. Plans range from $5 to $35 per month. If you’re looking for a Kikoff alternative with real credit card access, Kikoff doesn’t offer that within its credit builder subscription. Multiple users have also reported difficulty canceling.

Cred.ai

The Cred.ai credit card is a debit card replacement that reports to all three bureaus. It’s free to use, which makes it attractive. However, it functions more as a debit-like card with credit reporting than a traditional credit builder - you can only spend what you have. If you’re researching cred.ai alternatives because the product doesn’t fully meet your needs, services like Arro Credit Builder offer a more comprehensive approach with AI coaching, education, and a pathway to a real credit card.

Ava Credit Builder

The Ava credit builder is a newer entry in the space, typically priced $10 per month. Bureau reporting varies by plan, and the service focuses primarily on the tradeline itself without extensive educational features or credit card pathways. If you’re comparing Ava credit builder to other options, the main consideration is whether you need additional tools like AI coaching and card access alongside your tradeline.

Why Arro Credit Builder Is A Strong Alternative

If you’re asking, does Brigit report to credit bureaus and feeling like single-bureau coverage isn’t enough, Arro Credit Builder addresses that gap - and goes further.

Arro Credit Builder is a $12/month subscription that reports your payment history to both Experian and Equifax. That’s double the bureau coverage of Brigit. You receive a $2,000 reported tradeline, one of the highest in the credit builder space.

But here’s where Arro really separates from other credit builder brands: it’s the only service in this comparison that provides a pathway to an actual revolving credit card - the Arro Card. While other services stop at the tradeline, Arro positions you for real credit card access, which may have a more meaningful impact on your credit profile over time.

Arro also includes Artie, a 24/7 AI Money Coach that provides personalized answers to credit questions, budgeting advice, and financial guidance. If you’ve been searching for ai credit repair tools with real coaching built in, Artie delivers that without any additional cost. No other credit builder in this comparison includes anything comparable.

Additional features: ongoing access to credit scores in the app, comprehensive financial education resources, and transparent month-to-month pricing with easy cancellation. No hidden fees, no long-term contracts.

For anyone comparing the best credit builder apps, looking for a Kikoff alternative or cred.ai alternatives, or simply seeking a more complete option than Brigit, Arro offers the strongest combination of bureau coverage, credit card access, and AI-powered support.

➡️ Ready to build credit with 2-bureau reporting + AI coaching + credit card access? The Arro Credit Builder is $12/month with no hidden fees. Start building today.

What To Look For In Credit Building Apps

With so many credit-building apps on the market, it’s easy to get overwhelmed. Here’s what actually matters when choosing a service - whether you’re comparing Brigit, Arro, or any other credit builder brands.

Bureau coverage comes first. How many bureaus does the service report to? Single-bureau reporting (such as Brigit’s Experian-only model) builds a history on a single file. Two-bureau or three-bureau reporting provides broader visibility across more lenders.

Credit card pathways matter more than most people realize. A tradeline is helpful, but revolving credit (such as a credit card) can have a greater impact on your credit profile. If a service offers a pathway to real card access - like The Arro Credit Builder does with the Arro Card - that’s a meaningful advantage.

Educational support separates good services from great ones. Credit building isn’t just mechanical - understanding why your score moves helps you make better decisions long-term. Look for services that include lessons, coaching, or, at a minimum, clear guidance on what affects your score. AI credit repair tools are appealing, but make sure "free" doesn’t mean "bare-bones."

Transparent pricing and easy cancellation are non-negotiable. If a service makes it hard to cancel or buries fees in the fine print, that’s a red flag. The best credit-building apps are upfront about their costs and allow you to leave without hassle.

And finally: set realistic expectations. No credit builder delivers overnight results. Meaningful progress comes from consistent, on-time payments over months. The service you choose should make that consistency easy - not complicated.

➡️ Build credit the comprehensive way. Arro Credit Builder: $12/month, 2-bureau reporting, AI coaching, and the only pathway to the Arro Card. No hidden fees. Cancel anytime.

Also Read:

Credit Builder Programs Compared: Arro vs Kikoff vs Dovly vs TomoCredit (2026 Guide)

The 30-Day Credit Streak: 10-Minute Daily Actions That Compound

Rewards That Don’t Backfire: Using 1% Cash Back Without Overspending

FAQ

Does Brigit report to credit bureaus?

Yes, however Brigit reports to Experian only. It does not report payment activity to Equifax or TransUnion. This means your Brigit payment history is only visible to lenders who pull your Experian report.

Does Brigit report to all three credit bureaus?

No, Brigit reports exclusively to Experian. If you need broader bureau coverage, services like Kikoff (all three) or Arro Credit Builder (Experian and Equifax) report to more bureaus.

What is the best Kikoff alternative with credit card access?

Arro Credit Builder is a strong Kikoff alternative because it combines credit building with a pathway to the Arro Card - an actual revolving credit card. Kikoff’s credit line is limited to its own store, while Arro positions you for real credit card access.

How does Arro Credit Builder compare to Cred.ai?

The Cred.ai credit card is a free spending card that reports to three bureaus. The Arro Credit Builder costs $12/month but includes a $2,000 tradeline, AI coaching with Artie, educational resources, and a pathway to the Arro Card. If you want comprehensive credit-building beyond basic reporting, Arro offers additional features.

Are there AI credit repair tools that are actually free?

Some services offer free tiers with limited features, but comprehensive AI credit repair tools typically come with a subscription. The Arro Credit Builder includes AI coaching for $12/month with no additional costs, making it one of the most accessible options for AI-powered credit guidance.

How long does it take for credit builder reporting to affect my score?

Most people see initial changes within 30 to 60 days as the first payments are reported. More meaningful progress typically appears over 6 to 12 months of consistent on-time payments. Results vary based on your overall credit profile and activity with other accounts.

Is the Arro Credit Builder better than the Ava Credit Builder?

The Arro Credit Builder offers several features the Ava Credit Builder doesn’t: a pathway to the Arro Card, 24/7 AI coaching with Artie, comprehensive educational resources, and a $2,000 tradeline reported to two bureaus. At $12/month, Arro provides more comprehensive credit-building support.

What should I look for when comparing credit builder brands?

Focus on bureau coverage (how many bureaus the service reports to), whether there’s a pathway to real credit card access, what educational tools are included, pricing transparency, and ease of cancellation. The best credit builder apps combine multiple features rather than offering a tradeline alone.