Table of Contents

What Makes Credit Builder Brands Different

5 Essential Features To Evaluate

Understanding AI Credit Support

Pricing Reality Check

Bureau Reporting Truth

Red Flags To Avoid

Top Brands Compared

Making Your Decision

FAQ

When you're working to improve a low credit score, choosing between credit builder brands feels overwhelming.

Some promise AI-powered support, others tout three-bureau reporting, and many claim they'll boost your score faster than competitors. Which features actually matter?

This guide helps you evaluate credit builder brands based on what genuinely impacts credit-building success. Whether you're comparing established services or researching newer options like Ava credit builder, understanding these criteria ensures you invest wisely.

Key Takeaways

AI coaching (essentially AI credit repair free guidance) delivers more value than tradeline-only services

Two-bureau reporting covers most lenders - three bureaus are less critical than AI coaching and education

Pathways to real credit cards matter more than tradeline amounts

Transparent $10-15/month pricing indicates customer-first brands

Quality education creates lasting knowledge for maintaining good credit

What Makes Credit Builder Brands Different

Understanding the fundamental differences between credit builder brands helps you avoid paying for features you don't need while ensuring you get the support that actually matters.

The Three Types

Tradeline-Only: Report payments to bureaus. No coaching, no education. Mechanical credit building only.

Comprehensive Platforms: Modern best credit builder apps combine reporting with AI coaching, education, and card access. Arro bundles all these at $12/month.

Repair + Building Hybrids: Premium services ($35-40/month) remove errors through disputes while building history.

Why It Matters

Rebuilding from low credit requires solving two problems: a lack of payment history AND fixing habits that caused credit challenges. Tradeline-only services solve one. Comprehensive platforms solve both - helping you understand why you're building credit and how to maintain it.

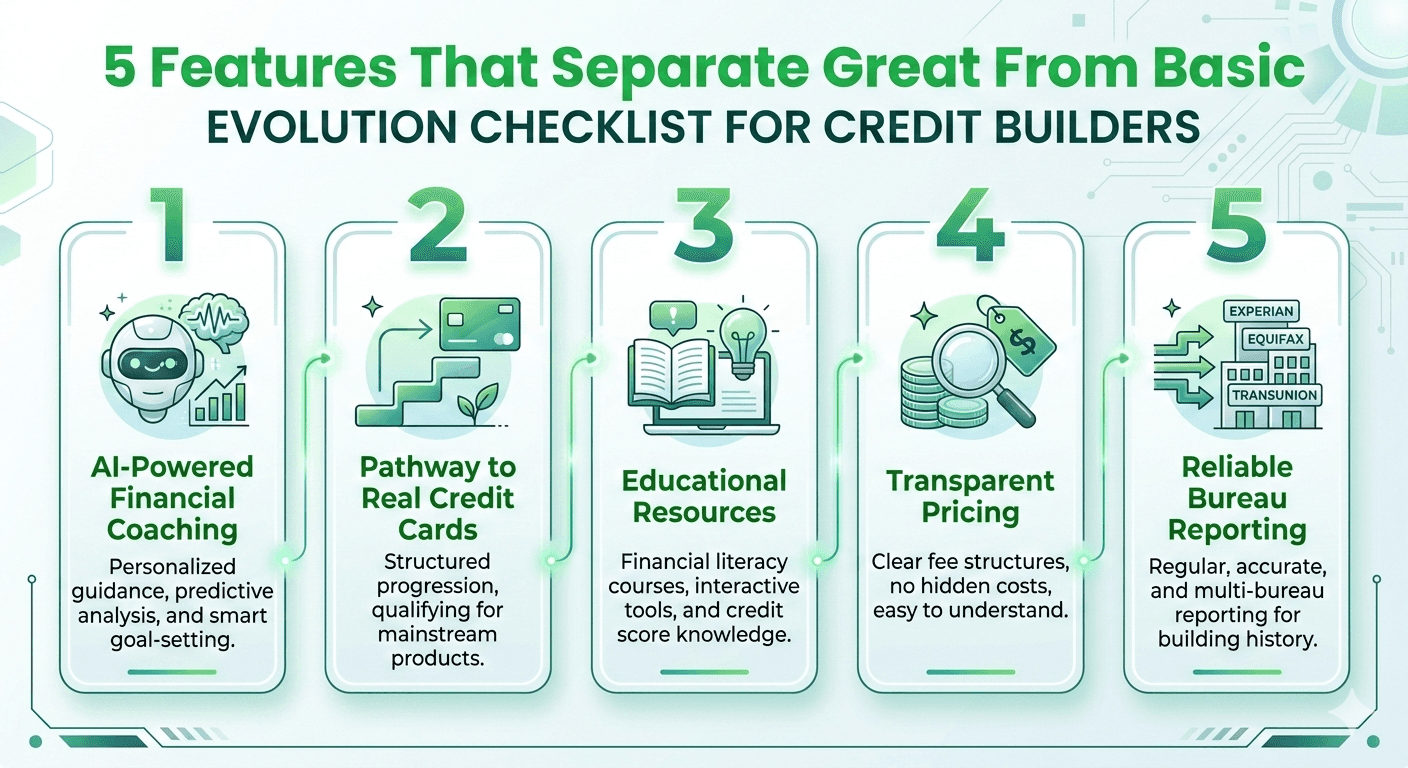

5 Essential Features To Evaluate

These five features separate comprehensive credit-building solutions from basic tradeline services that leave you without guidance or long-term support.

1. AI-Powered Financial Coaching

What it is: 24/7 chatbot guidance answering credit questions and providing personalized recommendations.

Why it matters: Instant access to guidance prevents mistakes. When you're deciding "Should I pay in full or carry a balance?" at 11PM, AI coaching gives accurate answers immediately.

Look for: Services including AI as part of subscription (essentially AI credit repair free features) deliver more value than those charging extra.

Example: Arro includes Artie (AI money coach) in $12/month - no extra fees for 24/7 guidance.

Also read:

Best Credit Builder Apps: What Actually Matters

AI Credit Repair: How Automated Tools Actually Work in 2026

Kikoff Alternative: Key Features to Compare

Cred.ai Alternatives: What to Consider When Switching

Does Brigit Report to Credit Bureaus? How Reporting Actually Works

Credit Builder Programs Compared: Arro vs Kikoff vs Dovly vs TomoCredit (2026 Guide)

Ava Credit Builder: Overview and Alternatives

2. Pathway to Real Credit Cards

What it is: Integrated credit card access, not separate products requiring new applications.

Why it matters: Revolving credit impacts your profile more than tradelines. Services offering unsecured card pathways help you transition to practical purchasing power.

Look for: Integrated access, unsecured options, rewards, and clear qualification criteria.

Example: Arro Credit Builder provides a pathway to the Arro Card (unsecured, 1% cashback) while competitors require separate secured card applications with deposits.

3. Educational Resources

What it is: In-app lessons teaching financial literacy alongside credit building.

Why it matters: Understanding why credit works helps you maintain good credit independently.

Look for: Bite-sized lessons, interactive elements, practical guidance covering credit basics and broader financial topics.

4. Transparent Pricing

What it is: Clear monthly costs with straightforward cancellation.

Red flags: Prices varying between marketing and checkout, automatic upgrades, and difficult cancellation.

Fair pricing:

Budget tradeline: $5-10/month

Comprehensive with AI: $10-15/month

Premium repair: $35-40/month

5. Reliable Bureau Reporting

What it is: Consistent monthly reporting to Experian, Equifax, and/or TransUnion.

Why consistency matters: Missed reports waste months of progress.

Two vs three bureaus: Most lenders pull from Experian and Equifax. Two-bureau reporting plus superior features often beats three-bureau reporting alone.

Verify: Check recent reviews for reporting consistency patterns.

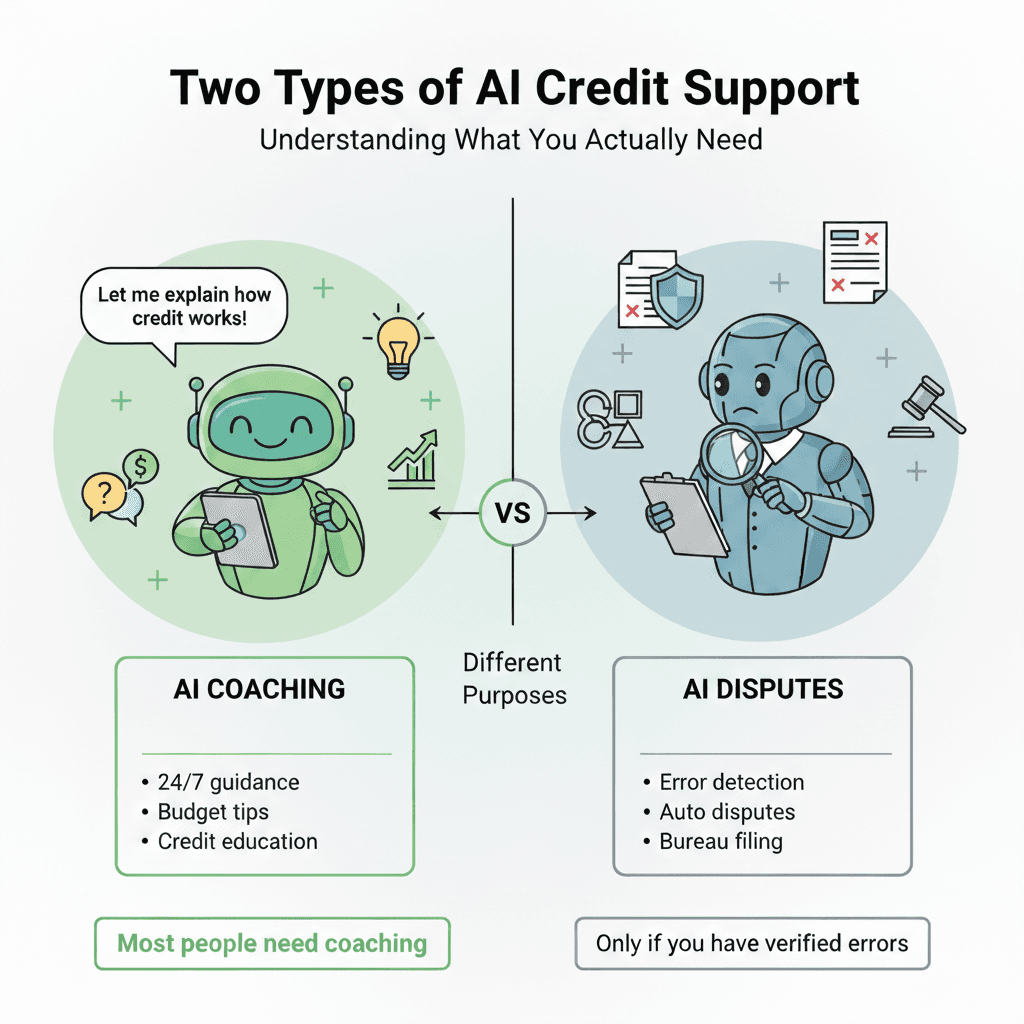

Understanding AI Credit Support

Credit builder brands mention "AI" in two different ways:

AI Credit Coaching

Answers credit/budgeting questions 24/7

Provides personalized recommendations

Explains concepts in plain language

Typically $10-15/month included in subscription

Choose if: Building from scratch, need financial guidance, limited budget.

AI Credit Repair

Scans reports for errors automatically

Files disputes with bureaus

Automates manual dispute process

Typically $35-40/month premium pricing

Choose if: Have verified errors, need AI credit repair automation.

Most people rebuilding credit need AI coaching, not premium disputes (unless verified errors exist).

Pricing Reality Check

Understanding what you should pay for credit-building helps prevent overspending on basic features marketed as premium services. Here's how to identify fair pricing versus inflated costs across different feature sets.

Strong value:

$12/month: Tradeline + AI coaching + education + credit card pathway

$5/month: Basic 3-bureau reporting

$40/month: Comprehensive repair + building + protection

Poor value:

$20/month: Tradeline only

$35/month: Features comparable to $12 competitors

Any price: Services with operational issues

Hidden costs to watch:

Deposits for secured cards

Processing fees

Upgrade fees

Early termination penalties

Bureau Reporting Truth

The "more bureaus is always better" myth leads many people to overpay for three-bureau reporting when two bureaus would serve them just as well.

Most credit card companies and auto lenders pull from Experian and Equifax - the two bureaus that comprehensive credit builder brands like Arro report to.

What matters more than bureau quantity is reporting consistency: a service that reports to two bureaus reliably every month delivers better results than one that reports to three bureaus inconsistently or misses reports entirely.

Three-bureau (Experian, Equifax, TransUnion):

Comprehensive coverage

Best for mortgages

Example: Kikoff

Two-bureau (Experian + Equifax):

Covers most lenders

Focus on AI coaching and education instead

Example: Arro, Dovly

Reality: Most credit card issuers and auto lenders pull from Experian and Equifax. Consistency matters more than quantity - three inconsistent bureaus deliver worse results than two reliable ones.

Red Flags To Avoid

Certain warning signs indicate credit builder brands that could waste months of your progress or trap you in difficult-to-cancel subscriptions.

Recognizing these red flags early saves you from services with operational problems, poor customer support, or misleading marketing. Watch for these issues before committing your money and time.

Operational issues:

Pending lawsuits or BBB alerts

Declining service quality in recent reviews

Inconsistent reporting patterns

Customer service problems:

Can't reach support

Cancellation nightmares

Scripted, unhelpful responses

Marketing red flags:

Guaranteeing score increases

"Instant" credit-building claims

Hidden fees in fine print

Vague bureau reporting information

Example: Does Brigit report to credit bureaus consistently? Services with operational challenges show reporting gaps. For dedicated credit building, use services designed explicitly for that purpose (Arro, Kikoff, Dovly).

Top Brands Compared

After understanding what to look for, here's how the leading credit builder brands actually stack up on the features that matter most. This comparison focuses on AI coaching, credit card access, education, pricing transparency, and bureau reporting consistency.

Arro - $12/month

AI coaching (Artie) included

Education resources

Pathway to Arro Card (unsecured)

Reports to Experian & Equifax

Best for: AI guidance + education + card access

Kikoff - $5-35/month

Reports to all 3 bureaus

Lowest entry price

No AI coaching

Best for: Budget users prioritizing 3-bureau coverage

Dovly - $0 or $39.99/month

Free plan available (no tradeline)

Premium includes AI credit repair disputes

$2K tradeline with Premium

Best for: Verified credit report errors

Cred alternatives: Users searching for Cred.AI credit card or Cred.AI alternatives should prioritize operational stability. Consider Arro for similar features with better reliability.

Ava credit builder: Apply extra scrutiny to newer services - verify operational track record and recent reviews.

Making Your Decision

Use this five-step framework to match your specific credit situation with the right service. Most people rebuilding credit benefit most from comprehensive platforms like Arro, but your budget and specific needs may point to different options.

Step 1: Identify Your Need

Build from scratch → Arro (comprehensive)

Tight budget → Kikoff (basic)

Report errors → Dovly (repair)

Step 2: Check Budget

$5-10: Budget options

$10-15: Comprehensive with AI

$35-40: Premium repair

Step 3: Verify Reliability

BBB rating

Recent reviews (3-6 months)

Consistent reporting confirmation

For most people: Arro at $12/month balances comprehensive features, AI coaching, education, and card pathway - delivering more value than basic services while costing less than premium.

Ready to build credit with AI guidance?

No credit check. Cancel anytime. Build credit history starting today.

FAQ

What should I look for in credit builder brands?

Prioritize AI coaching, credit card pathways, education, transparent pricing, and reliable bureau reporting. Services with AI coaching deliver more value than tradeline-only products.

Is AI credit repair worth it?

AI coaching ($10-15/month) helps most people rebuild credit. Premium AI credit repair disputes ($35-40/month) only if you have verified errors on your report.

How do I verify bureau reporting?

Check the website for explicit bureau disclosure, read recent reviews for consistency confirmation, and verify reports appear on your credit report 60-90 days after starting.

Are credit boosting apps better than secured cards?

Credit boosting apps with AI coaching and education often deliver better value - no deposit required, ongoing guidance, and pathways to unsecured credit versus secured card deposits.

Which brands offer AI coaching?

Arro includes AI coach Artie in a $12/month subscription. Most competitors don't offer AI coaching (Kikoff) or focus on disputes rather than education (Dovly).

What's a good Kikoff alternative?

Arro offers AI coaching, an integrated Arro Card pathway, and comprehensive education that Kikoff lacks. Trade-off: Kikoff reports to three bureaus, Arro reports to two (covering most lenders).

Does pricing guarantee faster results?

No. Credit building takes 6-12 months regardless of price. Higher costs add features (disputes, monitoring), not speed. Best credit builder apps maintain behaviors through education, not premium pricing.

How long should I use a credit builder?

6-12 months minimum. Continue until you qualify for prime cards, understand credit independently, have 12+ months of payment history, and achieve your target score.

Important Information

On-time payment history may have a positive impact on your credit score. Late payment may negatively impact your credit score. We report payment history to Experian and Equifax. Credit impact may vary based on a number of factors, including your activity with other financial services organizations.

Upward is a financial technology company, not an FDIC-insured bank. Credit builder lines of credit provided by Cross River Bank, Member FDIC. Line of credit is not a deposit product.