Your credit score affects almost every major life moment. Want to rent that dream apartment? Your credit gets checked. Planning to buy a car? Lenders look at your credit. Even some employers check credit reports during hiring.

Table of Contents

Why Your Credit Score Deserves Some Love

The Real Cost Of A Low Credit Score

5 Ways To Romance Your Credit Score This February

Why Building Credit Is Better With A Partner (Like Arro)

Your Credit Glow-Up Timeline: What To Expect

Breaking Up With Bad Credit Habits

Real Talk: Credit Myths That Need To Go

Start Your Credit Love Story Today

FAQ

If your credit score could speak, it might be feeling a little neglected right now. This Valentine's Day, it's time to change that relationship. Improving your credit isn't just about numbers - it's about opening doors to better opportunities, lower interest rates, and financial freedom.

The good news? You don't need perfect credit to start seeing real benefits. Even small improvements make a meaningful difference. And unlike some Valentine's Day relationships, this one gets better the more time you invest in it.

Key Takeaways

Payment history is the biggest factor in your credit score - consistent on-time payments are your most powerful tool.

Many users see credit improvements within 30-60 days of building a positive payment history.

The right tools make the difference - AI coaching and a pathway to a real credit card help you stay motivated and build credit effectively.

The Real Cost Of A Low Credit Score

A low credit score isn't just frustrating - it's expensive.

Higher interest rates mean you pay thousands more over time. A person with excellent credit might get a 5% car loan rate, while someone below 600 could face 15% or higher.

Rental applications get tougher. Many landlords require higher security deposits or reject applications when they see poor credit.

Credit card options become limited. Instead of rewards cards, you might only qualify for secured cards with high fees and low limits.

Here's the encouraging part: roughly 68 million Americans have credit scores below 601. You're not alone. And your current score doesn't define your financial future - you have the power to change it.

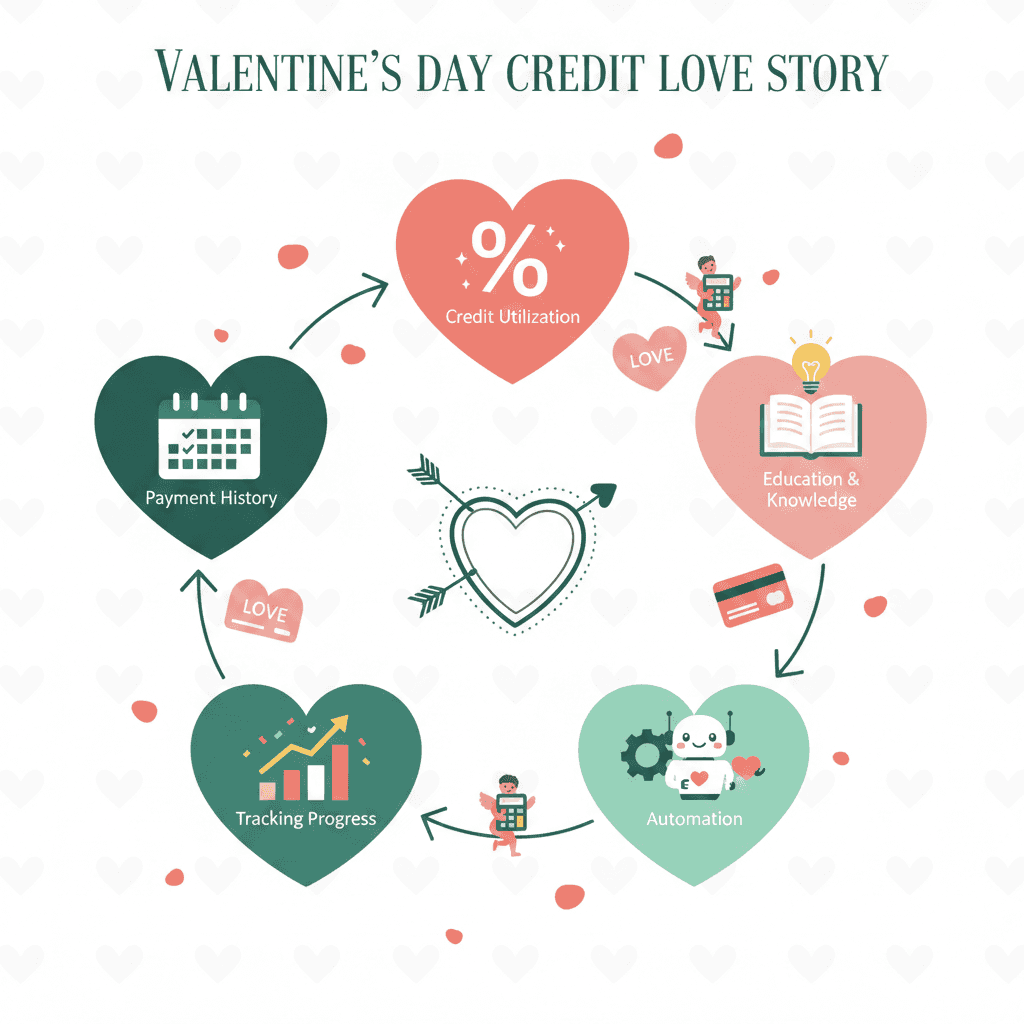

5 Ways To Romance Your Credit Score This February

Ready to start your credit improvement journey? Here are five practical ways to show your credit score some love this month.

1. Start Building Payment History (Even If You Have No Credit)

Your payment history accounts for about 35% of your credit score - it's the most important factor. But here's the catch-22: you need credit to build credit history, right?

Not anymore. Credit builder programs help you establish a payment history even if you have no existing credit. You make affordable monthly payments that get reported to major credit bureaus (Experian and Equifax). Over time, this consistent payment history builds your credit profile.

The best part? No hard credit check required, so applying won't hurt your score. Unlike traditional credit cards that may be denied, credit builders are designed for people in your exact situation.

2. Get Smart About Your Credit Utilization

Credit utilization is simple: it's how much of your available credit you're using. If you have a $300 credit limit and you've charged $100, you're using 33%.

Lenders like to see you using less than 30% of your available credit. Ideally, keeping it under 10% is even better.

Here's the strategy: use your card for small, regular purchases (like gas or groceries), then pay it off in full each month. This shows responsible credit use without racking up debt or interest charges.

3. Learn the Credit Game (Knowledge Is Power)

Understanding how credit works is just as important as mechanically building it. When you know why certain actions help or hurt your score, you make better decisions naturally.

Arro includes bite-sized lessons about credit basics, personalized insights, and 24/7 AI coaching with Artie, who answers your questions anytime. Got a random credit question at 11 PM? Artie's got you.

Topics worth exploring: how credit scores are calculated, what factors matter most, and realistic timelines for improvement. When you understand this, credit stops feeling mysterious and starts feeling manageable.

4. Set Up Your Credit Building on Autopilot

Consistency is everything when building credit. The problem? Life gets busy, and you forget payments.

The solution is automation. Arro Credit Builder works on autopay - your monthly subscription payment gets reported to credit bureaus automatically. You set it up once and let it run in the background.

This removes the friction that often derails credit building. Make sure your payment method has sufficient funds to avoid payment failures.

5. Track Your Progress and Celebrate Small Wins

Building credit can feel slow when you're just hoping numbers change. Tracking your progress and celebrating improvements keeps you motivated.

Arro gives you ongoing access to your credit score and factors in the app. Celebrate the small wins: three months of on-time payments, a 10-point score increase, completing credit lessons. These all count.

Credit building isn't about perfection - it's about progress. Every positive action moves you forward, even if the big number doesn't jump overnight. Those small, consistent improvements compound into meaningful change over time.

Why Building Credit Is Better With A Partner (Like Arro)

More Than Just a Tradeline

Arro provides payment history reporting plus a pathway to the Arro Card, an actual revolving credit card - something no competitor offers. Revolving credit can impact your profile differently than installment tradelines alone.

24/7 AI Coaching

Artie, your AI money coach, answers credit questions in plain language and provides personalized budgeting advice anytime you need it. No judgment, no jargon.

Transparent Pricing

$12/month gets you: $2,000 tradeline, pathway to Arro Card, 24/7 AI coaching, ongoing credit score access, and educational resources. Cancel anytime.

Ready to start? Get Arro Credit Builder for $12/month. No hidden fees. Cancel anytime.

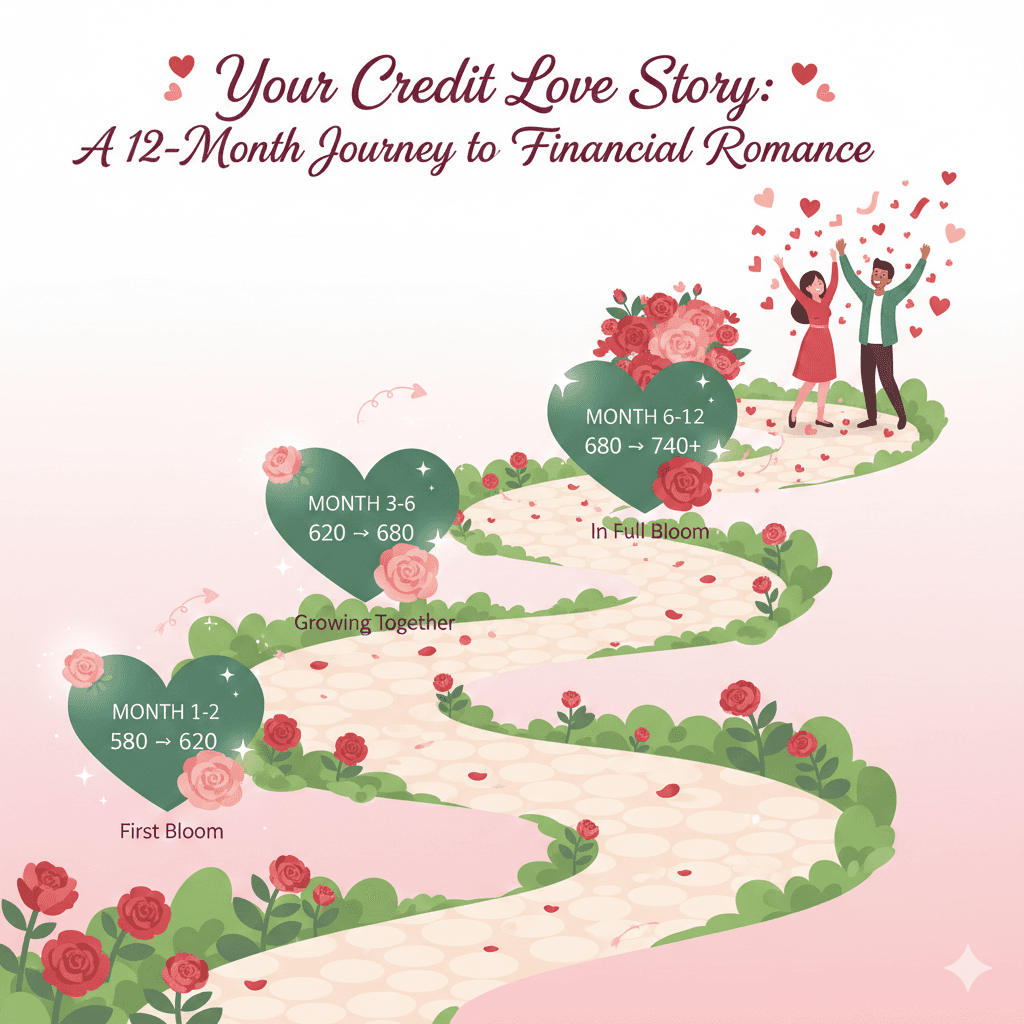

Your Credit Glow-Up Timeline

Month 1-2: Initial payments get reported within 30-60 days. Those with thin credit files may see an initial bump.

Months 3-6: Multiple on-time payments carry more weight. Many people see consistent improvements as credit reports show several months of positive history.

Months 6-12: Consistent payment history brings the most substantial improvements. Older negative marks have less impact. People often qualify for better financial products.

Everyone's journey is different. The key is consistency - keep making on-time payments and trust the process.

Breaking Up With Bad Credit Habits

Building better credit means changing habits that hold you back.

Late Payments

A single 30+ day late payment can drop your score by 50-100 points. Set up autopay and calendar reminders to avoid missing payments.

Ignoring Your Credit Report

Check your credit regularly to catch errors and track progress. Arro gives you ongoing access to your score and factors.

High Credit Utilization

Using most of your available credit signals trouble. Only charge what you can pay off in full each month.

Too Many Credit Applications

Multiple hard inquiries hurt your score. With Arro, there's no hard credit check to get started.

Real Talk: Credit Myths That Need To Go

Let's clear up some common misconceptions about credit that might be holding you back.

Myth: "Checking My Credit Hurts My Score"

Reality: Checking your own credit is a soft inquiry and does not hurt your score. You should be checking regularly to monitor for errors and track your progress. What hurts your score is when a lender performs a hard inquiry as part of a credit application.

Arro provides ongoing access to your credit score and factors in the app - check as often as you want with zero impact on your score.

Myth: "I Need Perfect Credit To Get Approved for Anything"

Reality: While excellent credit certainly opens more doors, you don't need perfect credit for most things. There are plenty of products designed specifically for people building or rebuilding credit.

Credit builders like Arro don't require any existing credit score. You can start building today regardless of your credit situation.

Myth: "Carrying a Balance on My Credit Card Builds Credit Faster"

Reality: You don't need to carry a balance or pay interest to build credit. Using your card and paying it off in full every month is just as effective (and much cheaper) than carrying a balance and paying interest.

This myth costs people money for zero additional credit benefit.

Start Your Credit Love Story Today

The best time to start building credit was a year ago. The second-best time is right now.

This Valentine's Day, invest in something that keeps giving back: your financial future. Building better credit opens doors - lower interest rates save thousands, rental applications get approved, and car loans become accessible.

You deserve better than hoping your credit will magically fix itself. You deserve the tools, support, and education to make meaningful progress. You deserve transparency about what you're paying for and realistic expectations.

That's what Arro provides: an honest, supportive partner in your credit-building journey. Not just a tradeline, but comprehensive AI coaching, educational resources, transparent pricing, and a pathway to the Arro Card.

Ready to swipe right on better credit?

Start building credit with Arro for just $12/month. No credit check required. No deposit needed. No hidden fees. Cancel anytime.

Your credit score in six months will thank you for starting today.

FAQ

What credit score do I need to qualify for the Arro Card?

You don't need a credit score to apply for the Arro Card. Unlike traditional credit cards, Arro uses alternative data like your income, bank account balance, and cash flow to determine approval, not your credit score. The application only requires a soft credit inquiry, which won't affect your credit score. As long as you have a positive bank account balance (at least $50), you'll likely be approved.

How is the Arro Card different from a secured credit card?

The Arro Card requires no security deposit, unlike secured cards that typically require $200-$500 upfront. You get instant approval and immediate virtual card access without locking up any cash. Plus, the Arro Card offers 1% cash back on gas and groceries (including Walmart and Target), a rarity for cards designed for those building credit. You can also increase your credit limit up to $2,500 and even lower your APR by completing financial education activities in the app.

Does the Arro Card have an annual fee?

The Arro Card requires an Arro membership, which costs $60 per year. However, if you're approved for a $50 starting credit limit, your first-year membership is discounted to just $12 (then $60 annually after that). This membership includes access to the card, 24/7 AI coaching with Artie, credit score monitoring, and educational resources that help you build financial literacy while building credit.

How quickly can I increase my credit limit with the Arro Card?

Your starting credit limit will be between $50 and $300, depending on your approval. The unique feature of the Arro Card is that you control how quickly you grow your limit, complete bite-sized financial education modules in the app, make on-time payments, and demonstrate responsible credit use to unlock credit limit increases up to $2,500. Many users report reaching higher limits within 9-18 months of active engagement.

Will applying for the Arro Card hurt my credit score?

No. Arro only performs a soft credit inquiry during the application process, which does not affect your credit score. Once approved, your payment history gets reported to all three major credit bureaus (Experian, Equifax, and TransUnion), helping you build positive credit history. As long as you make on-time payments, the Arro Card only helps your credit, it doesn't hurt it.

Can I use the Arro Card immediately after approval?

Yes. Once approved, you get instant access to a virtual card that you can use right away for online purchases, Apple Pay, Google Pay, and other digital wallet transactions. Your physical Mastercard arrives in the mail shortly after, but you don't have to wait to start using your credit line.