Team Arro

Learn the right credit sequence for newcomers, how to secure an apartment first, then build credit safely without slowing your progress and rental approval now.

Table Of Content

Why Order Matters More Than You Think

How Landlords Actually Evaluate Applications

Where Credit Helps And Where It Can Hurt

The Smart Credit Sequence For Newcomers

Why This Approach Works And What To Watch Out For

Your Next Smart Move Starts Here

FAQs

Moving to a new place, or a new country, comes with a lot of “firsts.” For instance, most newcomers wouldn't know that applying for a credit card and securing an apartment are actually linked. Understanding this connection can help you sequence these steps to your advantage and avoid unnecessary obstacles.

This confusion is incredibly common. In the U.S., more than 31% of people rent their homes, with over 100 million renters navigating similar decisions. If the rules aren’t clear, it’s easy to feel frozen. But you don’t need to guess, and you can actually use the right sequencing steps to your advantage.

In this guide, we’ll show how renting and credit connect, and how to move forward with confidence, step by step.

Key Takeaways

The order in which you apply for credit matters more than a “perfect” credit score.

Applying for new credit at the wrong time can complicate apartment approval, even with good intentions.

Landlords prioritize stability and reliability over future credit potential.

You can often rent successfully without strong credit by showing consistency in other ways.

Following a smart credit sequence helps reduce rejections and extra deposits.

Once housing is secured, building credit becomes safer and more effective.

Why Order Matters More Than You Think

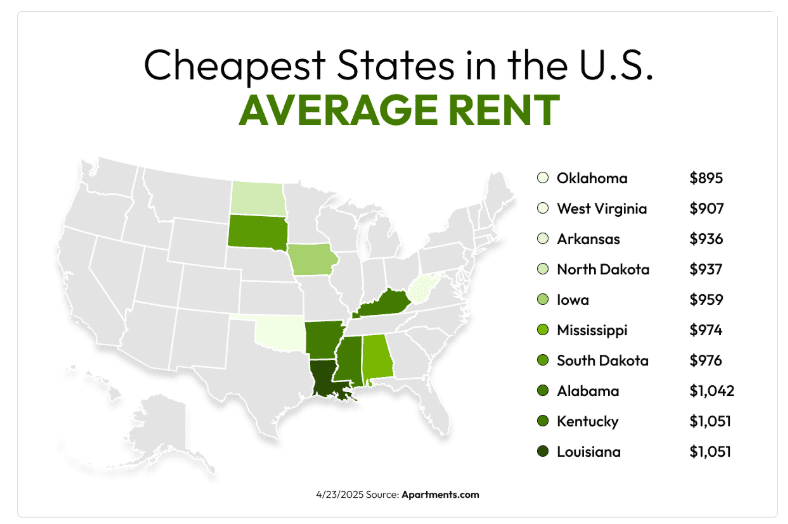

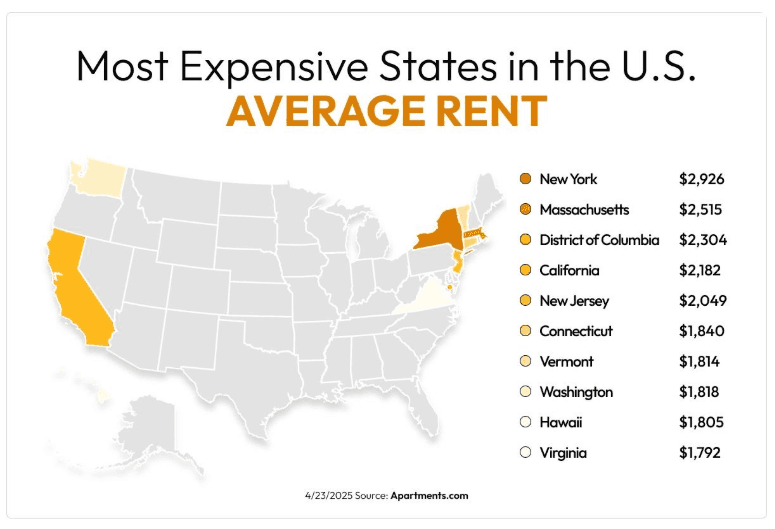

Housing decisions carry real weight. The average one-bedroom rent in the U.S. is over $1,600 per month, and nearly half of renters spend more than 30% of their income on rent.

Source: Apartments.com

That’s why timing matters. Some financial moves help you long-term but can create short-term friction if they happen at the wrong moment. This is where understanding the credit sequence becomes powerful.

If you’re new to the U.S. or new to credit, it’s natural to think, “I should build credit first so landlords trust me.” That instinct shows you’re thinking ahead. The issue is that rental systems and credit systems don’t always reward activity the same way.

Newcomers often feel stuck because they:

Haven’t been taught how credit timing affects rental applications

Assume more financial activity equals faster progress

Don’t realize that even positive actions can raise short-term flags

This uncertainty leads to hesitation, or well-meaning moves that work against you in the moment. That’s why the credit sequence matters. It replaces guesswork with clarity.

How Landlords Actually Evaluate Applications

Landlords aren’t looking for perfection. They’re looking for confidence that rent will be paid on time.

To make that call, they typically review:

Proof of income or employment

Rental history (if available)

Credit report or score

Background checks

Savings or upfront funds

Each item helps reduce risk. Credit is part of the picture, but it’s rarely the whole story.

The key insight: landlords care about stability right now, not whether you’re in the middle of building credit. Understanding this mindset explains why application order matters so much.

Where Credit Helps And Where It Can Hurt

Credit is useful, but timing determines how it’s perceived.

When Credit Helps

Showing a pattern of on-time payments

Keeping balances low and manageable

Supporting trust when rental history is limited

These benefits come from consistency over time, not from opening something new right before applying.

When Credit Can Hurt

Applying for new credit immediately before renting

Triggering hard inquiries that temporarily affect your profile

Creating the appearance of financial changes during review

Even responsible actions can look risky if they happen at the wrong time. This is exactly why following the right credit sequence matters.

The Smart Credit Sequence For Newcomers

Let’s walk through the order that protects your momentum and reduces stress.

Step 1: Secure Your Apartment First

Housing gives you stability, an address, and breathing room. Before applying for new credit, strengthen your rental application with:

Clear proof of income or an offer letter

Bank statements showing savings

A guarantor or co-signer, if needed

These signals build trust without adding new credit activity. This step anchors your financial foundation.

Step 2: Pause On New Credit During Review

While your rental application is under review:

Avoid applying for credit cards

Avoid personal or auto loans

Avoid anything that triggers a hard inquiry

This pause actually protects it. You’re keeping your financial snapshot steady while it’s being evaluated.

Step 3: Build Credit After Approval

Once your lease is signed, the pressure lifts, and this is the safest time to start building credit. Now you can:

Apply for a beginner-friendly credit card

Build on-time payment history

Use credit lightly and intentionally

Together, these steps form a clean, low-risk credit sequence: approval first, growth second.

Why This Approach Works And What To Watch Out For

This order aligns with how systems actually work. Apartments prioritize short-term reliability, whereas credit scores improve over time with consistent behavior. In fact, half of renter households in the U.S. spent more than 30% of their income on housing and utilities in 2022, making upfront signals of stability especially important to landlords.

At the same time, inquiries tend to matter more before approval than after. By separating “approval mode” from “building mode,” you avoid sending mixed signals. That clarity is the real power of a smart credit sequence.

Even prepared newcomers can make missteps if the timing is off. Opening a credit card “just to show activity,” draining savings to pay everything off at once, or applying to multiple apartments and lenders simultaneously can all work against you in the moment. Avoiding these actions helps keep your application calm and your options open.

If you have no credit at all, that doesn’t mean you have no options. It simply means landlords lean more heavily on other signals. Proof of steady income, savings for deposits or upfront rent, or a guarantor or co-signer can all strengthen your application. This approach works especially well for newcomers and first-time renters and fits seamlessly into a healthy credit-building sequence.

What To Do After You’re Approved

Once you’re settled into your apartment, credit-building becomes an opportunity instead of a risk. Smart moves after approval include opening a credit card designed for beginners, keeping balances low and payments on time, and treating credit as a long-term tool, not a test. Consistency, not speed, is what builds momentum here.

Also Read:

Your Next Smart Move Starts Here

Getting approved for an apartment and building credit doesn’t have to feel like competing goals. When you follow the correct order, everything clicks: secure your home first, then build credit with confidence. That’s the power of a smart credit sequence; it turns uncertainty into momentum.

That’s where Arro comes in. We believe building credit shouldn’t be confusing, expensive, or out of reach. With no hard credit checks, no deposit, and 1% cashback on gas and groceries, Arro makes it easy to start improving your credit while living your everyday life. Inside the app, Artie, your AI Money Coach, is there 24/7 to answer questions, celebrate wins, and help you make smart financial moves.

Every on-time payment, every lesson, and every small step forward helps unlock higher limits and stronger credit over time. Thousands of people are already building credit with Arro and enjoying the journey.

Ready to take your next step? Start building credit the smart way, right when the timing is right.

FAQs

What if I’m relocating for a job and have a tight timeline?

If you’re on a deadline, prioritize stability. Focus on securing housing using offer letters, proof of income, or a guarantor if needed. Credit-building can wait a few weeks; housing provides the foundation for every subsequent financial decision. Landlords are often familiar with job-based relocations and may be more flexible when income is clearly documented. Once you’re settled, you’ll have more bandwidth to build credit without added pressure.

Does applying for utilities or internet affect my credit?

Most utility and internet providers don’t run hard credit checks, but some may require a deposit if you have limited history. These accounts usually don’t impact credit unless payments are missed. It’s always smart to ask upfront. Knowing this in advance helps you plan for deposits without surprises. Setting up automatic payments can also help you stay organized during a busy move.

What if a landlord asks why I don’t have much credit history?

That’s common. A clear, honest explanation paired with proof of income, savings, or references often goes a long way. Many landlords value transparency and consistency more than a long credit file. Sharing context shows responsibility, not risk. It also opens the door to conversation rather than assumptions.

Can applying together with a roommate affect approval if one of us has limited credit?

Yes. Joint applications are often reviewed as a whole, so one person’s higher income or history can help. Just remember that shared leases mean shared responsibility, so alignment on budgeting matters. It’s important to discuss expectations upfront so there are no surprises later. Clear communication can make shared applications work smoothly for everyone involved.

Does having money in a foreign bank account help with a U.S. rental application?

Sometimes. While foreign accounts don’t replace U.S. credit, some landlords may accept translated statements as proof of funds. It helps to ask what documentation they’ll consider and be ready to explain the source. This can be especially helpful for newcomers who are early in their U.S. financial journey. Being proactive shows preparedness and can build trust during the application process.