Arro Team

Table of Content

What Is A Credit Card’s ‘Closing Date’?

Key Differences Between Due Date And Closing Date

Why Minimum Payments Aren’t Enough

What Is A Grace Period?

How Late Payments Can Damage Your Credit

Why Choose Arro?

FAQs

All the dates and deadlines on a credit card can be confusing. But making sense of what you see on your statement matters. Especially the ones that matter most: your closing date, payment due date, billing cycle, and grace period.

Understanding these can help you use your card smarter, improve your credit, and learn how the statement date vs the due date really affects your financial health.

In this article, we’ll break down everything you need to know about credit card statement date vs due date and why understanding the payment due date vs statement date can make a big difference in how you manage your money.

You’ll learn how these dates impact your credit score, interest charges, and payment strategy, all in simple, clear terms, so you can stay confident and in control of your finances.

Key Takeaways

Understanding credit card statement date vs due date helps you avoid late fees, interest charges, and credit score drops.

Paying your balance before the statement date lowers your reported balance and boosts your credit score.

Your grace period gives you at least 21 days of interest-free time use it to stay debt-free.

Making only minimum payments keeps you in debt longer and costs you more in interest.

Even one late payment can stay on your credit report for up to seven years, so consistency matters.

Tracking your due date and payment habits with Arro makes building credit easier and stress-free.

What Is A Credit Card’s Closing Date?

The closing date of a credit card refers to the final day of the billing cycle. This date is important because it determines the timeframe for transactions included in that billing statement. To better understand it, let’s start with the billing cycle itself.

A billing cycle, also known as the billing period or “open-to-close dates,” is the time between one closing date and the next.

The typical duration is between 28 and 31 days, but doesn’t always match calendar months (for example, Dec. 1–31) because it depends on when your account was opened. The closing date simply marks the end of that cycle.

It’s also called a statement date, since it’s when your credit card issuer generates your billing statement. The word “closing” can sound intimidating, but don’t worry, your account isn’t shutting down. It just means your activity for that cycle is finalized, and a new one is about to begin.

Here’s what happens on your credit card statement date

Your activity for the billing cycle is totaled (purchases, payments, credits, etc.)

Your statement balance is calculated and sent

Your minimum payment is determined

Any interest charges are applied

Your balance and activity are typically reported to the credit bureaus

Understanding your statement date vs due date is key to knowing when your payments will count toward your next billing cycle.

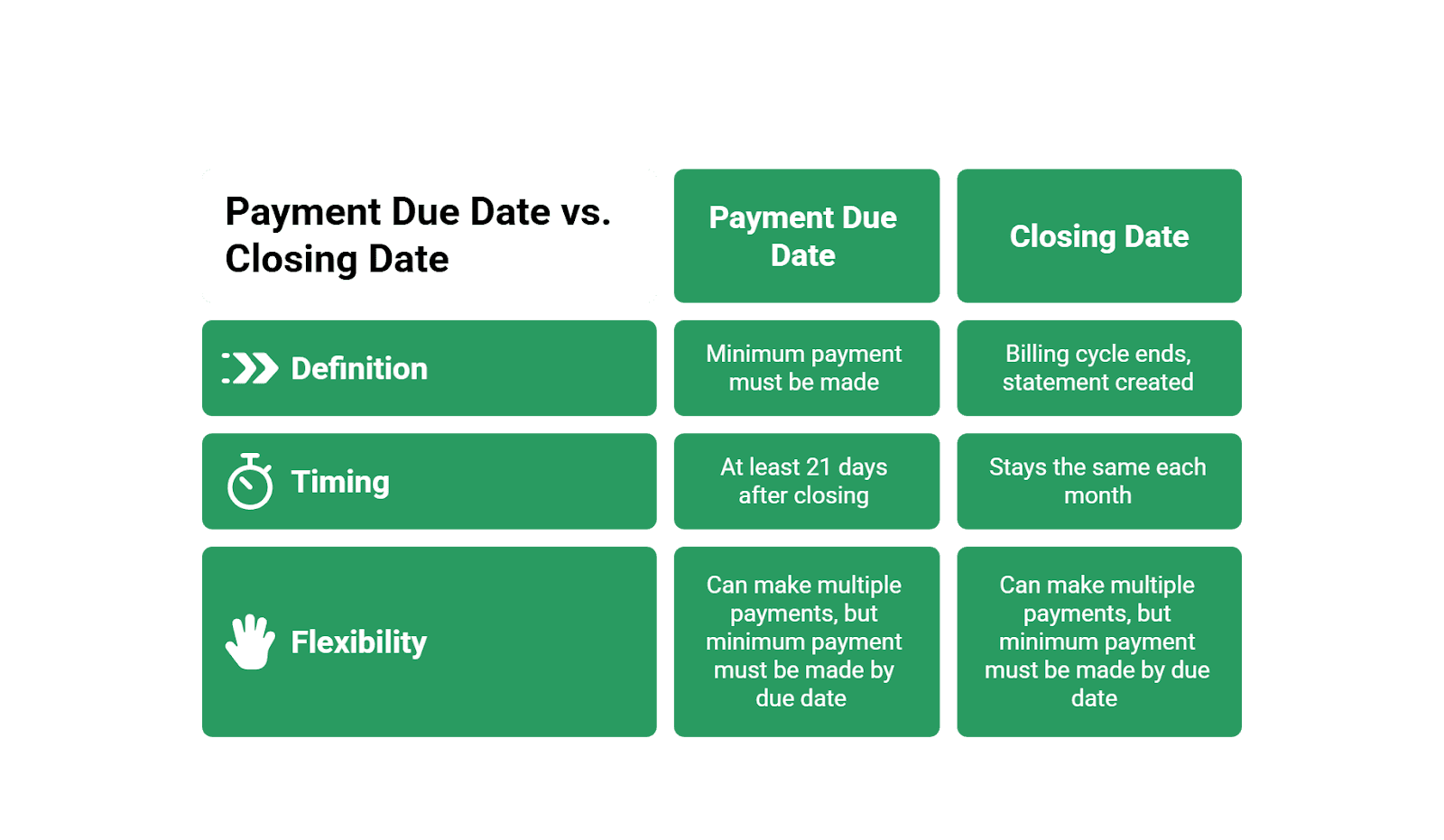

Key Differences Between Due Date And Closing Date

Do you know the difference between your payment due date and your closing date? Many people refer to this as the difference between the payment due date and the statement date, and it’s one of the most important concepts in managing your credit wisely.

Your payment due date is when you must make at least your minimum payment to be considered on time. Your closing date (or statement date) is when your billing cycle ends and your statement balance is created.

Your due date usually falls at least 21 days after your closing date and stays the same each month (or moves to the next business day if it lands on a weekend). Federal law also ensures your credit card company can’t change this date unless you ask for it.

You can make one payment or several before the due date. As long as the total equals or exceeds the minimum, you’ll avoid late fees.

If you pay after the due date, you could face

Late fees

Interest rate increases (penalty APR)

Loss of promotional rates

Interest charges on your remaining balance

Knowing how statement date vs due date works helps you stay in control, avoid surprise fees, and keep your credit moving in the right direction.

Also Read:

Aim High: What an 800 Credit Score Means and How to Get There

Arro Credit Card: Increase Your Odds of Passing Tenant Credit Checks

Why Are These Two Dates Important?

Understanding the statement date vs the due date gives you more control over your credit. Staying aware of them helps you.

Make on-time payments

Avoid interest charges

Protect your credit score

At Arro, we make it easy to track these key dates so you can build credit without the stress.

Why Does Your Closing Date Matter For Credit?

Credit card companies report balances and activity to credit bureaus monthly, typically on or shortly after your statement date. You can use this to your advantage by paying down your balance before that date to build your credit score.

Why? Because payments made before your statement date vs due date lower the balance that’s reported to the bureaus, improving your credit utilization ratio (the percentage of available credit you’re using). Keeping your utilization below 30% is recommended, especially if you want a top-tier score.

Let’s make it simple with an example:

It’s Dec. 13, and your balance is $3,000 on a $4,000 limit. Your closing date (statement date) is Dec. 17, and your payment due date is Jan. 9.

If you wait until January 7 to pay the full amount of $3,000, it’s technically on time, but your balance will already have been reported on December 17, and that high number can lower your score.

If you pay the $3,000 on Dec. 15, your reported balance will be $0, which is great for your credit.

The key takeaway is simple: paying before your statement date vs due date helps lower your reported balance and gives your credit score a boost.

Why Minimum Payments Aren’t Enough

As we always say, minimum payment = minimum benefit. Paying only the minimum keeps your account in good standing, but it also means you’ll owe interest on the remaining balance.

For example:

Let’s say your statement balance is $1,500, and your minimum payment is $35 due by Dec. 15.

If you pay $35 on Dec. 12, you’re on time, but you’ll still pay interest on what’s left.

If you pay the full $1,500 on Dec. 12, you’ll skip interest entirely and keep your score in great shape.

Understanding how statement date vs due date impacts your payments helps you make smarter choices. It might feel easier to pay the minimum, but that habit keeps you in debt longer and costs you more in interest. Plus, with Arro, you can earn rewards while building your score.

Improve your credit score.

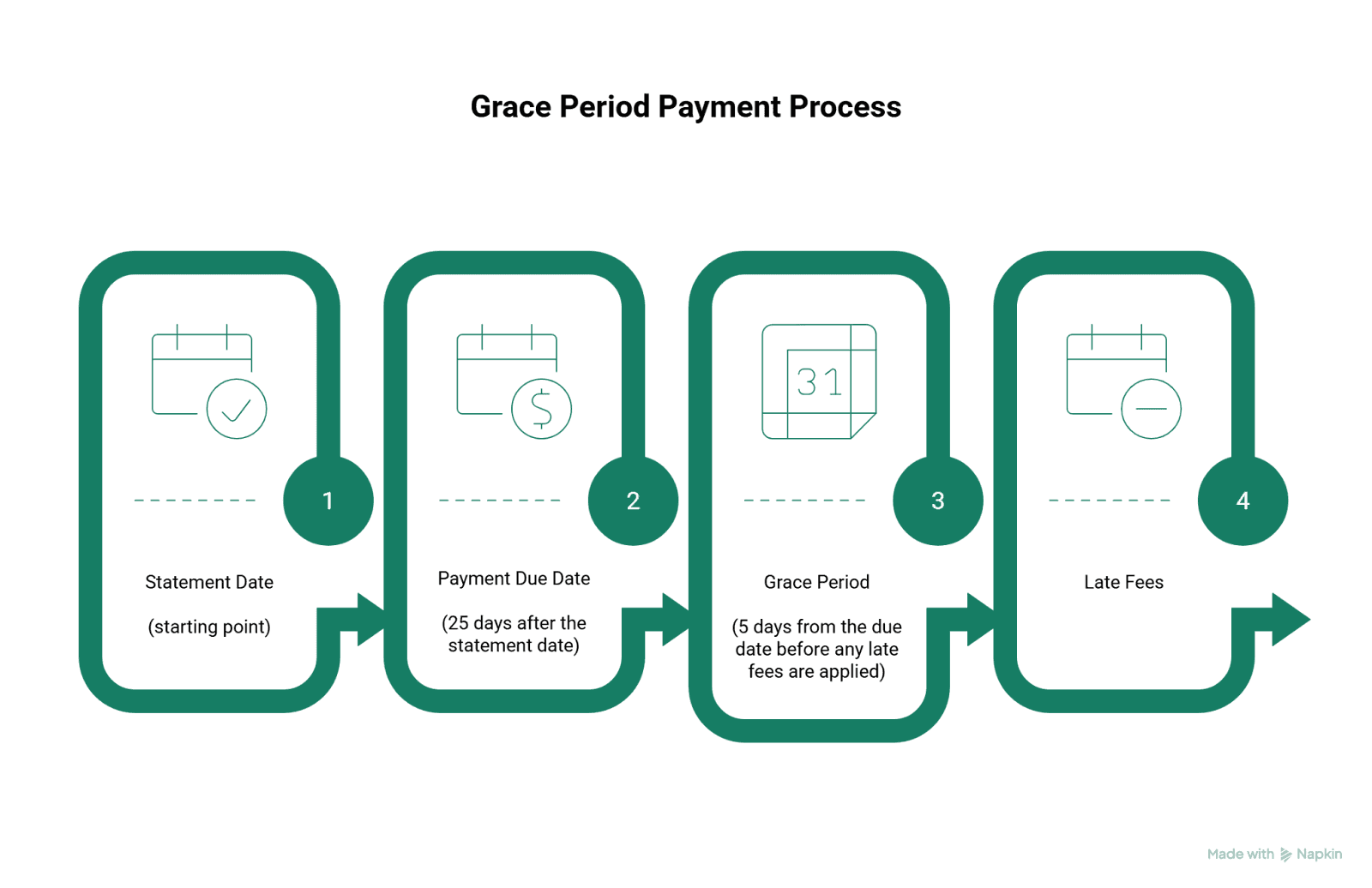

What Is A Grace Period?

Remember that time between your closing date and due date? That’s at least 21 days, and it might include something called a grace period. This is your interest-free window, and using it wisely can save you money.

A grace period is the stretch of days (at least 21) after your closing date when you won’t pay interest on new purchases, as long as you’ve paid your previous balance in full.

To keep your grace period active

Pay your statement balance in full every month

Always pay your balance in full each month to take control of your finances and avoid unnecessary interest charges

Track your due date to make the most of that interest-free time

If you don’t pay in full, you’ll lose your grace period, and it can take a couple of months of full payments to earn it back. Not all cards offer grace periods, so check your terms or ask your issuer.

Also, grace periods don’t apply to cash advances. Even if you pay off your balance later, you’ll still owe interest on that part.

Keeping your grace period intact means more control, less interest, and extra breathing room between spending and paying.

How Late Payments Can Damage Your Credit

Even one late payment can throw off your finances. You might get hit with fees or higher interest rates, and if you’re 30 days or more past due, it can show up on your credit report. Since payment history is a major factor in your score, staying on top of your statement date vs due date is essential.

Here’s what can happen if you pay late

You’ll likely be charged a late fee

Your interest rate can increase (sometimes up to 30%)

You could lose promotional rates or special offers

Your late payment might be reported to the credit bureaus

Your minimum payment could rise since more goes toward interest

Late payments can stick around for up to seven years and make lenders hesitant to approve you or offer good rates.

If you’ve already missed a payment, don’t panic. Catch up as soon as possible to minimize the damage. Paying on time going forward shows lenders you’re back on track and helps your score recover faster.

Try Arro’s card today and invest in your future!

Why Choose Arro?

At Arro, we believe building credit shouldn’t be confusing, expensive, or out of reach. That’s why we created a credit card that supports you in learning, earning, and developing, all seamlessly integrated within a single app.

With no hard credit checks, no deposit, and 1% cashback on gas and groceries, Arro makes it simple to start improving your credit while rewarding your everyday spending. You’ll also get access to Artie, your personal AI Money Coach, who’s there 24/7 to answer questions, celebrate wins, and help you make smart financial moves.

Every on-time payment, every lesson, every small step forward helps you unlock higher credit limits and better credit health. Thousands of people are already building stronger credit with Arro and having fun doing it.

Ready to start your own journey?

Download the Arro app today and see how easy it can be to build credit with confidence.

FAQs

1. What happens if my payment due date falls on a weekend or holiday?

If your due date lands on a weekend or holiday, most credit card companies automatically move it to the next business day. However, it’s best not to wait until the last minute, so using AutoPay or making payments a few days early can ensure your payment is processed on time.

2. How can I check when my payment is reported to the credit bureaus?

Each lender has its own reporting schedule, usually tied to your statement or closing date. You can check your credit card account settings, call your issuer, or monitor your credit report to see when updates appear. This helps you plan payments strategically. Arro reports payments to the bureaus at the end.

3. What should I do if I accidentally miss a payment?

Pay as soon as you can, even if it’s just the minimum. After that, give your card issuer a call and ask if they’ll waive the late fee, especially if it’s your first time. To avoid this happening again, consider setting up AutoPay or setting reminders so you never miss a payment!

4. Can making multiple payments a month help improve my credit score?

Yes, making multiple payments throughout the month can help lower your credit utilization ratio, which is beneficial for your credit score. When you pay down your balance more frequently, you keep your utilization rate lower, which is a positive signal to credit bureaus. It’s especially helpful if you tend to use a large portion of your credit limit but want to avoid paying interest and maintain a healthy score.

5. What happens if I miss a payment but catch up quickly? Will it still hurt my credit?

Even if you catch up on your payments soon after missing one, your credit score could still be affected. Credit card issuers typically report missed payments to the credit bureaus once you are 30 days late, which can negatively impact your credit score. The longer the delay before you make your payment, the greater the potential impact on your score. The sooner you get back on track, the better, but it’s essential to prioritize making payments on time to avoid this scenario.