Table of Contents

Why Consider A Kikoff Alternative?

Key Features To Compare In Credit Builder Apps

Arro Credit Builder: A Comprehensive Kikoff Alternative

Other Credit Builder Brands Worth Considering

AI Credit Repair Free VS. Paid Options

How Credit Boosting Apps Actually Work

Making Your Decision: Which Alternative Is Right for You?

FAQ

If you're searching for a Kikoff alternative, you're likely exploring options for building or rebuilding your credit. While Kikoff has helped many users establish credit tradelines, it's not the only solution available - and it may not be the best fit for your specific needs.

This guide examines key features to compare when evaluating credit builder brands, with special attention to services that offer AI-driven credit repair tools, personalized coaching, and pathways to actual revolving credit.

Whether you're looking for the best credit builder apps with educational resources or cred.ai alternatives that offer more comprehensive support, understanding what separates one service from another helps you make an informed decision.

Key Takeaways

Two-bureau reporting (Experian and Equifax) covers most lenders- Kikoff's three-bureau coverage isn't always worth sacrificing AI coaching and education

AI-powered coaching separates modern credit builders from basic tradeline services, with some offering AI credit repair, free guidance included

Pathways to real credit cards matter more than tradeline amounts - Arro provides integrated credit card access, while others require separate applications

Mid-tier pricing ($10-15/month) often delivers the best value through comprehensive features versus budget tradeline-only or premium repair services

Customer service quality and cancellation ease vary significantly - always check recent reviews before committing

Credit building takes 6-12 months regardless of service - prioritize long-term financial education over quick score boost promises

Why Consider A Kikoff Alternative?

Kikoff has established itself as an affordable entry point for credit building at $5-$35/month. However, several factors might lead you to explore alternatives:

Limited Credit Line Utility

Kikoff's credit lines can only be used within their proprietary store for e-books and courses. While this still builds payment history, it doesn't provide the practical spending flexibility of a real credit card. If you're looking for a path to real purchasing power alongside credit-building, you'll need to consider alternatives that offer integrated credit card access.

Customer Service Concerns

Multiple user reviews across platforms highlight difficulties reaching Kikoff customer support and challenges canceling subscriptions. While experiences vary, the consistency of these complaints suggests potential friction points that alternatives with more responsive support teams may avoid.

Missing Educational Guidance

Kikoff offers basic credit-building but lacks the personalized coaching that helps you understand why certain financial decisions affect your credit. If you're rebuilding credit after past mistakes, having an AI coach to answer questions 24/7- essentially, AI credit repair free guidance included in your subscription - can accelerate your financial education alongside your credit building.

No Integrated Card Pathway

While Kikoff offers a secured card as a separate product, it requires additional steps and doesn't integrate with your credit builder subscription. Best credit builder apps in 2026 increasingly offer pathways to unsecured credit as part of the core service, helping you transition from building payment history to accessing actual revolving credit.

Key Features To Compare In Credit Builder Apps

When evaluating credit builder brands, certain features separate adequate solutions from comprehensive ones. Here's what to compare:

Bureau Reporting Coverage

What it is: The number of major credit bureaus (Experian, Equifax, TransUnion) that receive your payment history reports.

Why it matters: More reporting doesn't always mean better credit building. While Kikoff reports to all three bureaus, most lenders primarily pull from Experian and Equifax. Services reporting to two bureaus may deliver similar practical results at better value points, especially if they offer additional features like AI coaching or card access.

What to look for: Confirm which bureaus receive reports and whether your target lenders (mortgage, auto, etc.) typically use those bureaus for approval decisions.

Tradeline Amount

What it is: The credit line amount reported to bureaus as your available credit.

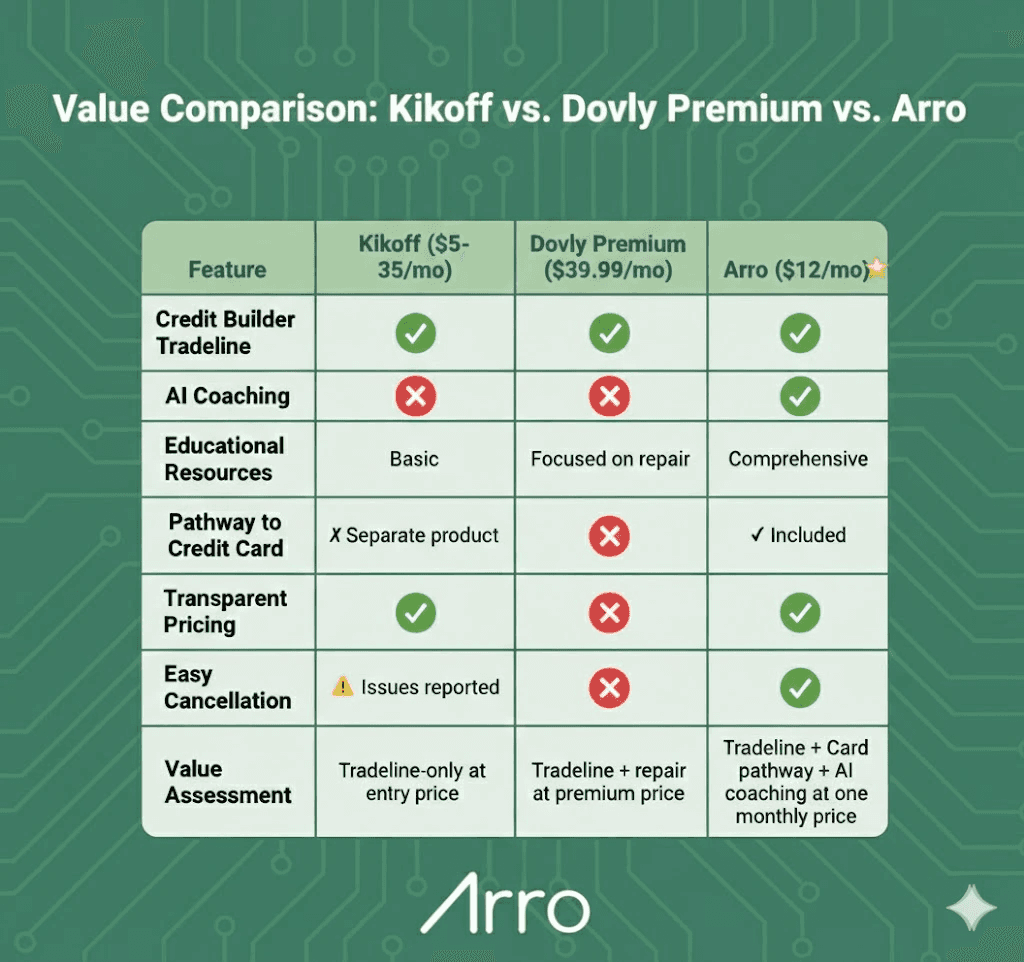

Why it matters: Higher tradeline amounts can improve your credit mix and available credit, though the impact varies based on your overall credit profile. Kikoff offers $750-$2,500 tradelines depending on plan, while alternatives like Arro and Dovly report $2,000 tradelines.

What to look for: Balance tradeline amount against other features - a $2,000 tradeline with AI coaching may provide more value than a $2,500 tradeline without educational support.

AI-Powered Coaching and Support

What it is: Intelligent financial guidance available through chatbot interfaces, often described as AI credit repair free resources when included in subscriptions.

Why it matters: Credit building is more effective when you understand the principles behind the process. AI coaches can answer questions instantly, provide personalized budgeting insights, and help you make informed financial decisions without waiting for human support representatives.

What to look for: Services that include 24/7 AI coaching as part of the base subscription, not as an upsell. The AI should offer personalized guidance based on your spending patterns and credit goals.

Pathway to Revolving Credit

What it is: Integrated access to actual credit cards or lines of credit beyond just tradeline reporting.

Why it matters: Revolving credit (like credit cards) typically carries more weight with lenders than installment credit or tradeline-only products. Best credit builder apps increasingly provide pathways to unsecured credit cards, helping you transition from building history to accessing practical credit tools.

What to look for: Services that offer integrated card access as part of the credit building journey, not as completely separate products requiring new applications and qualifications.

Educational Resources

What it is: In-app lessons, articles, and guided content that teach financial literacy alongside credit building.

Why it matters: Understanding credit utilization, payment timing, and credit mix helps you make better decisions long after you've built your score. Services that educate while you build create lasting financial knowledge.

What to look for: Bite-sized lessons that fit your schedule, progress tracking for educational goals, and content that addresses your specific credit situation (rebuilding vs. building from scratch).

Transparent Pricing and Cancellation

What it is: Clear monthly costs with straightforward cancellation processes.

Why it matters: Hidden fees and difficult cancellations plague some credit boosting apps. Services that respect your time and make leaving as easy as joining demonstrate customer-first priorities.

What to look for: Month-to-month pricing with no long-term commitments, documented cancellation processes, and recent user reviews confirming easy exits when needed.

Credit Score Access and Monitoring

What it is: Ongoing visibility into your credit score and the factors affecting it.

Why it matters: Regular score updates help you track progress and understand which behaviors improve your credit most effectively. While all services eventually report to bureaus, not all provide transparent score access within the app.

What to look for: In-app credit score visibility with explanations of score factors, not just basic number updates. Understanding why your score changed matters as much as seeing that it did.

Also read:

Arro Credit Builder: A Comprehensive Kikoff Alternative

When comparing credit builder brands, Arro Credit Builder emerges as a strong Kikoff alternative for users seeking more than basic tradeline reporting. Here's how Arro differentiates itself:

What Makes Arro Different

Integrated Pathway to the Arro Card

Unlike Kikoff's separate secured card product, Arro Credit Builder provides a pathway to the Arro Card - an actual unsecured revolving credit card. While a credit builder subscription isn't required to apply for the card, it helps build payment history that supports future approval. This integration means you're not just building a tradeline; you're positioning yourself for real purchasing power and the type of revolving credit that lenders often weigh heavily in approval decisions.

24/7 AI Money Coach (Artie)

Meet Artie, your AI money coach - essentially, AI credit repair free guidance included with your subscription. Get instant answers to credit questions, personalized budgeting advice, and recommendations tailored to your financial situation, available anytime you need support. No other major credit builder in this comparison offers intelligent, always-available coaching without additional fees.

Ongoing Credit Score Access

Arro provides ongoing access to your credit score and score factors directly in the app. While credit scores typically update monthly when bureaus receive new data (regardless of which service you use), you always have transparent access to understand where you stand and what's affecting your credit.

Educational Focus

Arro doesn't just help you build credit mechanically - it helps you understand why credit works the way it does through built-in resources, real-time insights, and AI coaching. This knowledge serves you for life, not just during your subscription.

Arro's Key Features

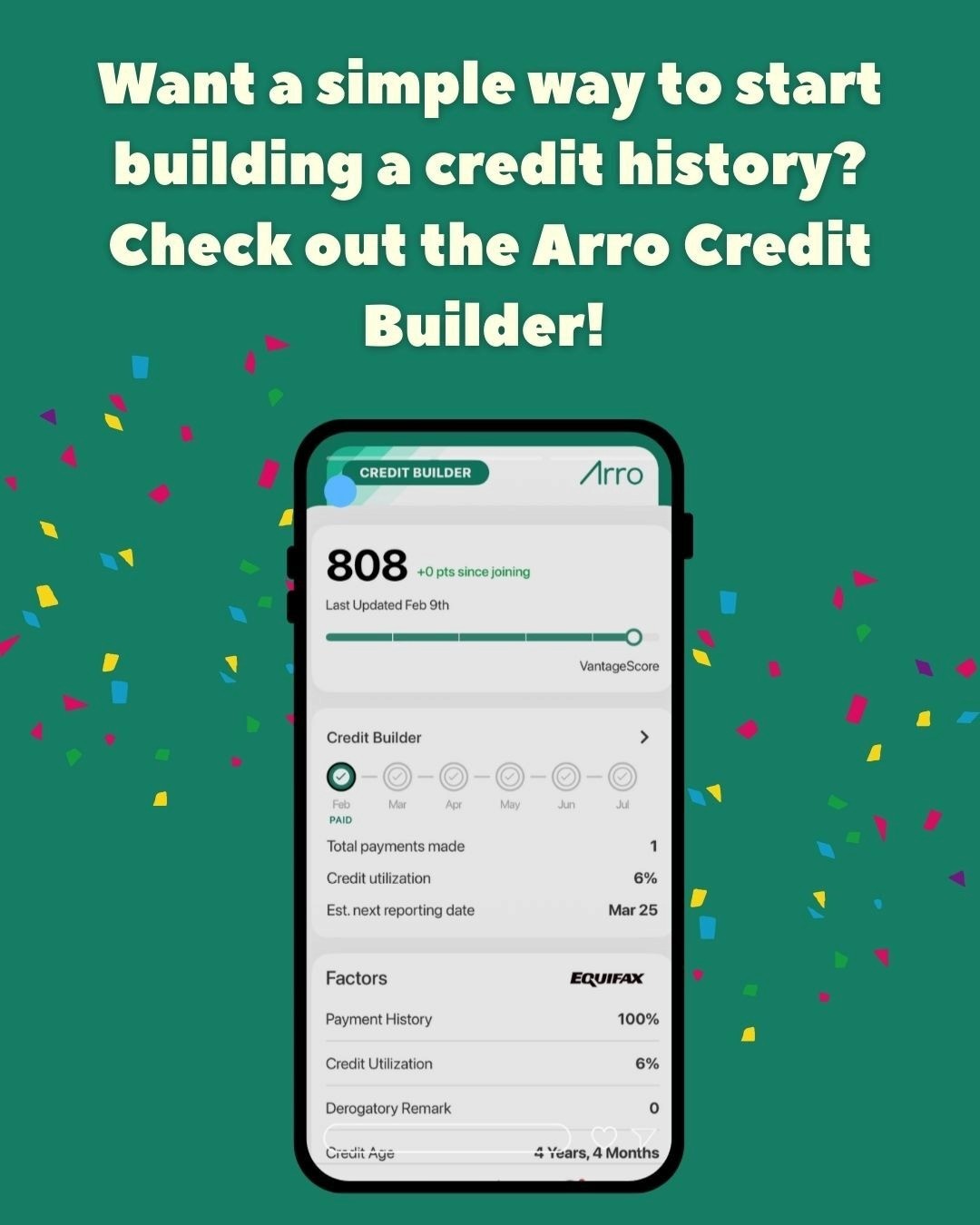

$2,000 reported tradeline to Experian and Equifax

AI coaching with Artie is available 24/7 for credit questions

Budgeting insights to understand spending patterns

Real-time credit insights and score factors in-app

Financial education resources are integrated throughout the experience

Pathway to the Arro Card for actual revolving credit access

Transparent $12/month pricing with no hidden fees

Month-to-month flexibility with straightforward cancellation

Who Arro is Best For

Arro Credit Builder works best for users who:

Want a pathway to actual revolving credit, not just a reported tradeline

Value AI-powered financial guidance and 24/7 coaching support

Prefer transparent educational resources during their credit-building journey

Need ongoing access to their credit score and factors affecting it

Appreciate mid-tier pricing ($12/mo) that balances affordability with comprehensive features

What Arro Doesn't Offer

Like several best credit builder apps, Arro reports to two major credit bureaus (Experian and Equifax) rather than all three. For most users, this covers the bureaus that lenders primarily use for approval decisions. However, if comprehensive three-bureau reporting is critical for your situation (e.g., applying for a mortgage in the near future and knowing your lender uses TransUnion), you may prefer services like Kikoff, which report to all three bureaus.

Other Credit Builder Brands Worth Considering

While Arro offers the most comprehensive feature set for most users, other credit builder brands may fit specific needs:

Dovly: Best for Credit Repair + Building

Pricing: $0 (Free) or $39.99/month (Premium)

Key Features:

Free plan with basic TransUnion monitoring

Premium includes a $2,000 tradeline reported to Experian and Equifax

AI-powered automated disputes with all three bureaus

Rent, telecom, and utility bill reporting (up to 24 months)

$1 million identity theft insurance

Best for: Users who need credit repair through disputes alongside credit building. If you have errors on your credit report or need to dispute inaccurate information, Dovly's automated dispute services justify the premium pricing.

Considerations: At $39.99/month, Dovly costs more than 3x Arro's price. If you don't have any errors to dispute, you may be paying for features you don't need. The free plan doesn't include the tradeline or multi-bureau reporting.

Cred.ai Alternatives: What Happened to Cred?

Many users searching for cred.ai alternatives are responding to service disruptions or changes with the Cred credit builder platform. While Cred.ai offered features similar to other credit boosting apps, operational challenges have led users to seek more reliable alternatives.

Why Users Look for Cred.ai Alternatives:

Service reliability concerns

Inconsistent credit bureau reporting

Customer service difficulties

Better feature sets are available from competitors

Recommended Cred.ai Alternatives:

Arro Credit Builder: Comprehensive features with AI coaching and card pathway at $12/month

Kikoff: Basic credit building with 3-bureau reporting at $5-$35/month

Dovly: Credit repair focus with premium features at $39.99/month

Ava Credit Builder and Other Emerging Options

The Ava credit builder and similar newer services continue to emerge in the credit builder space. When evaluating any newer platform, consider:

Track record: How long has the service operated reliably?

Bureau partnerships: Which credit bureaus receive your payment reports?

Customer reviews: What do recent users say about service quality and results?

Company stability: Are there any legal or operational concerns?

For newer services, waiting 6-12 months to see established patterns often reveals service quality more clearly than launch-period marketing.

Does Brigit Report to Credit Bureaus?

Users frequently ask, "Does Brigit report to credit bureaus?" when researching credit builder brands.

Brigit primarily focuses on cash advances and budgeting tools rather than traditional credit building. As of early 2026, Brigit offers select credit-building features through partnerships, but it's not primarily positioned as a credit-building service like Arro, Kikoff, or Dovly.

For credit-building specifically, services designed for that purpose (Arro, Kikoff, Dovly) typically offer more focused features and consistent bureau reporting than apps that offer credit building as a secondary feature.

AI Credit Repair Free vs. Paid Options

The term "AI credit repair free" represents different offerings depending on the service:

What "AI Credit Repair" Actually Means

AI-Powered Coaching (Included in Subscriptions): Services like Arro include AI coaching as part of the base subscription - this is essentially AI credit repair free guidance because you're not paying extra for the AI features. The AI coach (Artie) helps you understand credit factors, make better financial decisions, and avoid mistakes that could hurt your credit.

AI-Powered Disputes (Usually Premium): Services like Dovly use AI to automate credit report disputes, identify potential errors, and submit disputes to bureaus. This feature typically requires premium subscriptions ($39.99/month for Dovly) and focuses on removing inaccurate information rather than building a new positive history.

Free Credit Building Tools

Several services offer free tiers with limited features:

Dovly Free Plan:

Monthly TransUnion credit score and report

Manual dispute selection with TransUnion only

Basic credit monitoring

Does not include: The $2,000 tradeline (Premium only)

Credit Karma:

Free credit score monitoring from TransUnion and Equifax

Basic credit education

Does not include: Credit building tradeline or payment reporting

When Free Tools Make Sense

Free credit monitoring tools work well for:

Tracking your existing credit score

Identifying errors that need disputes

Basic credit education and awareness

However, free tools don't build new positive payment history. If you're starting with no credit or low credit, you need a service that reports payment activity to bureaus, which requires paid subscriptions.

When Paid Credit Builders Deliver Better Value

For users with low credit scores or thin credit files, paid credit builders provide:

Consistent payment history reported to major bureaus

Educational resources that explain credit mechanics

AI coaching for personalized guidance (like Arro's Artie)

Pathways to actual credit products (like the Arro Card)

Bottom line: While some AI credit repair free tools exist, comprehensive credit building with AI coaching and bureau reporting requires paid subscriptions. Services like Arro deliver significant value by bundling AI guidance, education, and card access into one transparent monthly fee.

How Credit Boosting Apps Actually Work

Understanding how credit boosting apps function helps you set realistic expectations and choose the right service:

The Credit Building Mechanism

1. Payment Account Creation

When you subscribe to a credit builder, the service creates a tradeline (a credit account) in your name. This might be:

A credit builder loan where you make monthly payments

A subscription service that reports as an installment account

A hybrid model combining education with reported payments

2. Bureau Reporting

Each month, the service reports your payment activity to one or more credit bureaus (Experian, Equifax, TransUnion). Consistent on-time payments demonstrate financial responsibility, which positively impacts your credit score over time.

3. Credit History Development

Over 6-12 months, your payment history builds. Credit scoring models consider:

Payment history (35% of FICO score)

Length of credit history (15% of FICO score)

Credit mix (10% of FICO score)

4. Score Improvement

As positive payment history accumulates, your credit score typically increases. Users with thin credit files or those rebuilding after past issues often see the most significant improvements.

What Credit Boosting Apps Can't Do

They can't instantly repair credit: Building credit takes months of consistent payments. Services promising immediate score boosts should be viewed skeptically.

They can't remove accurate negative information: Only inaccurate information can be disputed and removed. Accurate late payments, collections, or bankruptcies remain on your report for their designated timeframes.

They work best as part of broader financial responsibility: Credit builders help most when combined with other positive behaviors: paying all bills on time, keeping credit utilization low, and managing debt responsibly.

Setting Realistic Timelines

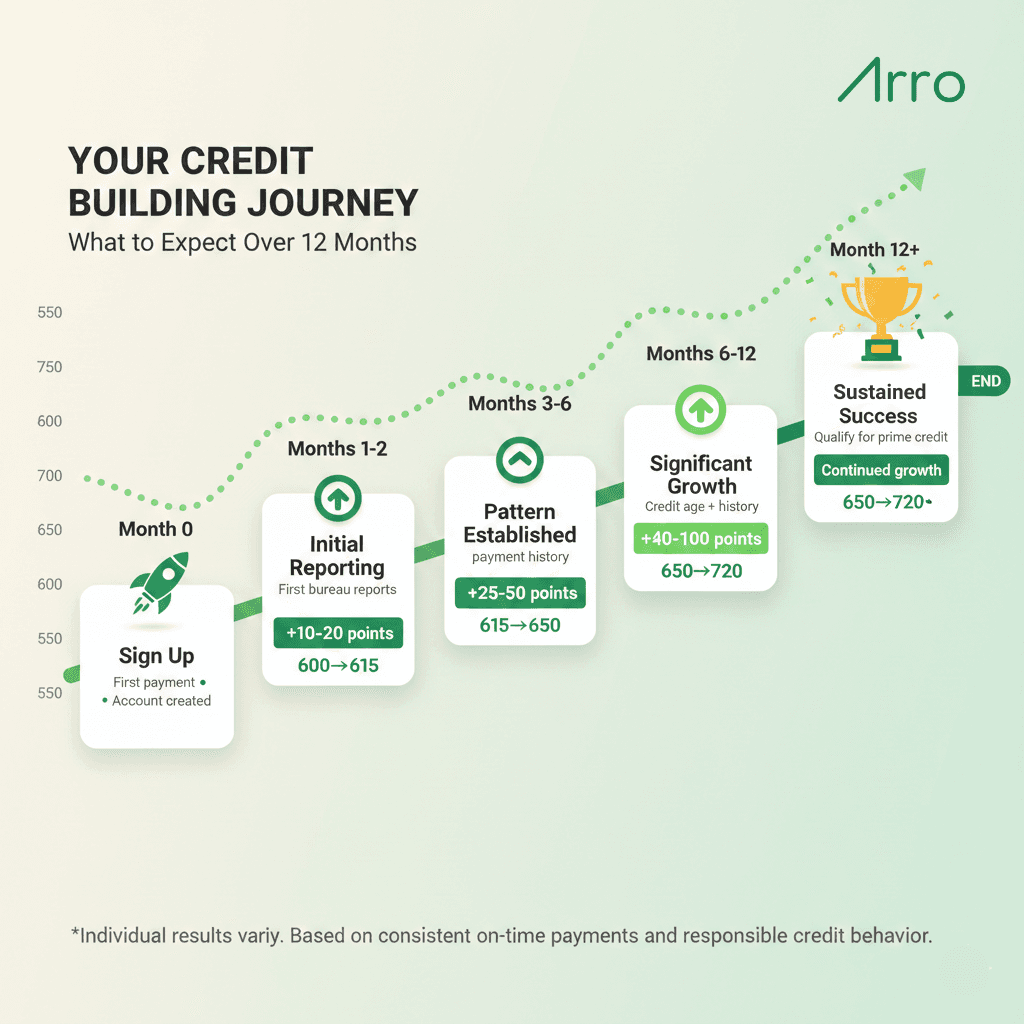

First 30-60 days: Initial payments reported; users often see first score movements (often 10-30 points for those with thin files)

3-6 months: Consistent payment pattern established; more substantial progress becomes visible

6-12 months: Full impact of sustained payment history; users often see significant score improvements (40-100+ points depending on starting position)

Beyond 12 months: Credit age continues building; a combination of payment history and credit age strengthens the credit profile

Making Your Decision: Which Alternative Is Right for You?

Choosing the right Kikoff alternative depends on your specific credit situation and financial goals:

Choose Kikoff If:

✓ You need reporting to all three credit bureaus specifically

✓ You want the absolute lowest entry price ($5/mo basic plan)

✓ You're comfortable with basic credit building without AI coaching or educational resources

✓ You don't need pathway to actual credit cards (or you're willing to apply for their secured card separately)

Choose Dovly Premium If:

✓ You have errors on your credit report that need professional dispute services

✓ You can afford premium pricing ($39.99/mo) for comprehensive credit repair features

✓ You need automated disputes across all three bureaus

✓ You want to report rent, telecom, and utility payments alongside credit building

Choose Free Tools If:

✓ You already have established credit and just need monitoring

✓ You want to identify errors before deciding on paid credit building

✓ You're researching credit basics before committing to a paid service

Questions to Ask Before Deciding

1. What's my primary goal?

Building credit from scratch → Arro or Kikoff

Repairing credit with errors → Dovly

Monitoring existing credit → Free tools

2. What's my budget?

$5-12/month → Kikoff or Arro

$40/month → Dovly Premium

$0 → Free monitoring tools

3. Do I value AI coaching and education?

Yes → Arro (includes 24/7 AI coach)

No → Kikoff (basic credit building only)

4. Do I want a pathway to actual credit cards?

Yes → Arro (integrated card pathway)

Separate is fine → Kikoff (secured card as separate product)

5. How important is 3-bureau reporting?

Critical → Kikoff

Experian + Equifax sufficient → Arro or Dovly

Choose Arro Credit Builder If:

✓ You want more than just a tradeline - you're looking for AI coaching, education, and pathway to a real credit card

✓ You value 24/7 support through AI credit repair free guidance (Artie)

✓ You appreciate mid-tier pricing ($12/mo) that balances affordability with comprehensive features

✓ You want ongoing access to your credit score and factors in-app

✓ You're building credit for long-term financial health, not just a quick score boost

Start building credit the comprehensive way → Try Arro Credit Builder

Frequently Asked Questions

What's the best Kikoff alternative for 2026?

Arro Credit Builder is the best comprehensive Kikoff alternative for most users, offering AI coaching, educational resources, and the only integrated pathway to actual revolving credit through the Arro Card. While Kikoff provides three-bureau reporting at a lower entry cost, Arro delivers significantly more features at $12/month, including 24/7 AI money coach Artie, ongoing credit score access, and comprehensive financial education that helps you understand the "why" behind credit building, not just the mechanics.

Are there any credit-builder apps with free AI credit repair?

Yes, Arro Credit Builder includes AI coaching (Artie) as part of the $12/month subscription, providing what's essentially AI credit repair free guidance - you're not paying extra for AI features. Artie offers 24/7 personalized advice on credit questions, budgeting, and financial decisions. However, this is different from automated dispute services (which Dovly offers at $39.99/month). Arro's AI coaching helps you understand credit and make better decisions, while AI-powered dispute services focus on removing inaccurate information from reports.

How do the best credit builder apps compare to Kikoff?

The best credit builder apps in 2026 offer features beyond basic tradeline reporting. Kikoff provides three-bureau coverage at $5-$35/month with tradeline-only credit building. Arro adds AI coaching, educational resources, and integrated credit card access at $12/month. Dovly includes automated disputes and credit repair services at $39.99/month. The "best" depends on your needs: Kikoff for basic building with three-bureau coverage, Arro for comprehensive features and education, or Dovly for credit repair alongside building.

What are good cred.ai alternatives?

Strong Cred.ai alternatives include Arro Credit Builder (AI coaching and card pathway at $12/mo), Kikoff (basic credit-building with 3-bureau reporting at $5-35/mo), and Dovly (credit-repair focus at $39.99/mo). Arro provides the most comprehensive alternative with features Cred.ai users value: AI-powered guidance, transparent pricing, and a pathway to actual credit cards. When evaluating alternatives, prioritize services with proven track records, consistent bureau reporting, and responsive customer service - factors that separate reliable credit builders from services with operational challenges.

Does Arro report to the same bureaus as Kikoff?

Arro reports to two major credit bureaus (Experian and Equifax), while Kikoff reports to all three (Experian, Equifax, and TransUnion). However, most lenders primarily rely on Experian and Equifax for approval decisions, so Arro's two-bureau reporting covers most lending situations. The additional TransUnion reporting from Kikoff provides broader coverage, which may benefit users applying for mortgages or loans where they know TransUnion will be pulled. For most credit-building purposes, two-bureau reporting combined with Arro's additional features (AI coaching, card pathway) delivers greater overall value than three-bureau reporting alone.

How long does it take to see results from credit builder apps?

Most users begin building credit history within 30-60 days, as their first payments are reported to the bureaus. More substantial credit building typically occurs over 6-12 months of consistent payment history. Timeline varies based on starting credit profile, overall financial behavior, and whether you're building from scratch or rebuilding. Services offering pathways to revolving credit (like Arro Card) may help build credit more effectively than tradeline-only products. All credit boosting apps require months of consistent payments - there are no instant credit repair solutions, and services promising immediate results should be viewed skeptically.

Can I use multiple credit builder apps at the same time?

Yes, you can use multiple credit builder brands simultaneously. Adding multiple tradelines can diversify your credit mix and accelerate credit building across different accounts. However, consider the total monthly cost and whether incremental benefits justify the expense. Often, one well-managed credit builder with comprehensive features and a pathway to revolving credit (like Arro) is sufficient for meaningful credit building. If you combine services, ensure you can afford all monthly payments; missed payments on any account could negatively impact the credit you're working to build.

What's better: Kikoff's 3-bureau reporting or Arro's AI coaching?

The answer depends on your priorities. Kikoff's three-bureau reporting provides comprehensive coverage across Experian, Equifax, and TransUnion. Arro's two-bureau reporting (Experian and Equifax) covers most lender requirements while adding 24/7 AI coaching, educational resources, and a pathway to the Arro Card. For users who need basic tradeline reporting with maximum bureau coverage, Kikoff works well. For users who want to understand credit deeply, receive personalized guidance, and position themselves for actual revolving credit, Arro's additional features deliver greater long-term value despite reporting to one fewer bureau.

Ready To Build Credit The Comprehensive Way?

While Kikoff offers solid basic credit building, Arro Credit Builder provides something more: AI-powered guidance, educational resources, and the only integrated pathway to actual revolving credit through the Arro Card.

What makes Arro different:

24/7 AI Money Coach (Artie) for personalized guidance

Ongoing access to credit score and factors in-app

Comprehensive financial education resources

Pathway to the Arro Card (real revolving credit)

Transparent $12/month pricing with no hidden fees

Don't settle for tradeline-only credit building. Start building credit that opens doors.

Start Building Credit with AI Guidance → Try Arro Credit Builder for $12/Month

No hidden fees. Cancel anytime. Build credit history starting today.