Team Arro

Table Of Contents

What Is The Lowest Possible Credit Score?

What Happens Just Above The Floor: Understanding Poor Credit Ranges

How Does A Score Get This Low? The Real Causes

The Real-World Cost Of A Low Credit Score

There Is No Such Thing As A Permanent Score

How To Start Climbing From A Low Score

No Credit VS. Low Credit: What It Means And How To Move Forward

FAQ

A 300 credit score isn’t just low, it’s a financial red flag. Most people know that credit scores range from 300 to 850, but very few understand what life looks like at the bottom of that scale. It’s not just a number. It can mean denied applications, higher costs, and limited financial options at every turn.

Whether you are starting from zero, rebuilding after a rough patch, or simply trying to understand where you stand, this guide breaks down the lowest possible credit score, what it means in practical terms, and exactly what you can do about it.

Key Takeaways

The lowest credit score is 300, but most people struggle in the “poor” range just above it.

Low scores are usually caused by late payments, high balances, and negative events, not by a single mistake.

Poor credit affects more than loans. It impacts housing, jobs, insurance, and everyday costs.

Your credit score is not permanent; negative items fade, and positive habits rebuild it over time.

The fastest way to improve your score is simple: pay on time, lower balances, and build a positive history.

No credit and low credit lead to similar challenges, but both can be fixed with consistent, reported activity.

What Is The Lowest Possible Credit Score?

The lowest credit score for the two most widely used scoring models, FICO and VantageScore, is 300. Both models use the same 300–850 range, with 300 as the floor and 850 as the ceiling.

In practice, almost no one actually has a score of 300. Getting there would require a sustained pattern of severe financial problems: multiple missed payments, accounts in collections, a bankruptcy, defaulted loans, and maxed-out credit lines, all at once, over an extended period. A single bad event, even a serious one, will not drop most people to the absolute minimum.

That said, reaching the lowest credit score is not the only scenario worth understanding. Scores below 580 (FICO) or 600 (VantageScore) are generally classified as poor or subprime and face many of the same obstacles as scores near 300. Roughly 13% of Americans fall into the poor FICO range, that is, tens of millions of people navigating the financial system with a significant disadvantage.

What Happens Just Above The Floor: Understanding Poor Credit Ranges

Because the absolute lowest credit score is rare, most people dealing with credit problems have scores somewhere in the poor or fair range, not at 300, but low enough to face real consequences.

Here is how the major scoring models classify these ranges:

Bureau | Their "Personality" | Why It’s Important |

TransUnion | The Techie | They use advanced data science and provide real-time updates for things like auto loans and credit lines. They also offer a "score simulator" so you can see how your choices might change your score. |

Equifax | The Historian | They are the oldest bureau (founded in 1899) and have the deepest records. Because they have extensive long-term data, they are the favorite among mortgage lenders. |

Experian | The Builder | They are very user-friendly for people starting out. With Experian Boost, you can add "extra" things like Netflix or utility bills to your file to help raise your score faster. |

The practical takeaway: if your score is below 580 on FICO or below 600 on VantageScore, you are in subprime territory. You are not dealing with the lowest credit score in an absolute sense, but you will encounter many of the same obstacles, denied applications, higher interest rates, and fewer financial options.

How Does A Score Get This Low? The Real Causes

A low credit score rarely comes from a single mistake. It’s usually the result of repeated behaviors that signal risk to lenders. Understanding these patterns is the first step to fixing them.

Late payments (≈35% of your score): Payment history is the biggest factor. Any payment more than 30 days late is recorded as a negative mark. The longer and more frequent the delays, the greater the damage. A single 90-day late payment can drop a strong score by 100+ points.

High credit utilization (≈30%): This is how much of your available credit you use. Maxed-out cards suggest financial strain. Aim to stay below 30%, though excellent scores typically come from keeping it under 10%.

Major negative events: Bankruptcy, foreclosure, repossession, and charge-offs have the most severe impact. For example, a Chapter 7 bankruptcy can drop a good score by 200+ points and remain on your report for up to 10 years.

Thin or no credit history: A lack of credit history can lead to a low score or no score at all. This is common for young adults and new immigrants. While not the same as poor credit, being “credit invisible” creates similar barriers.

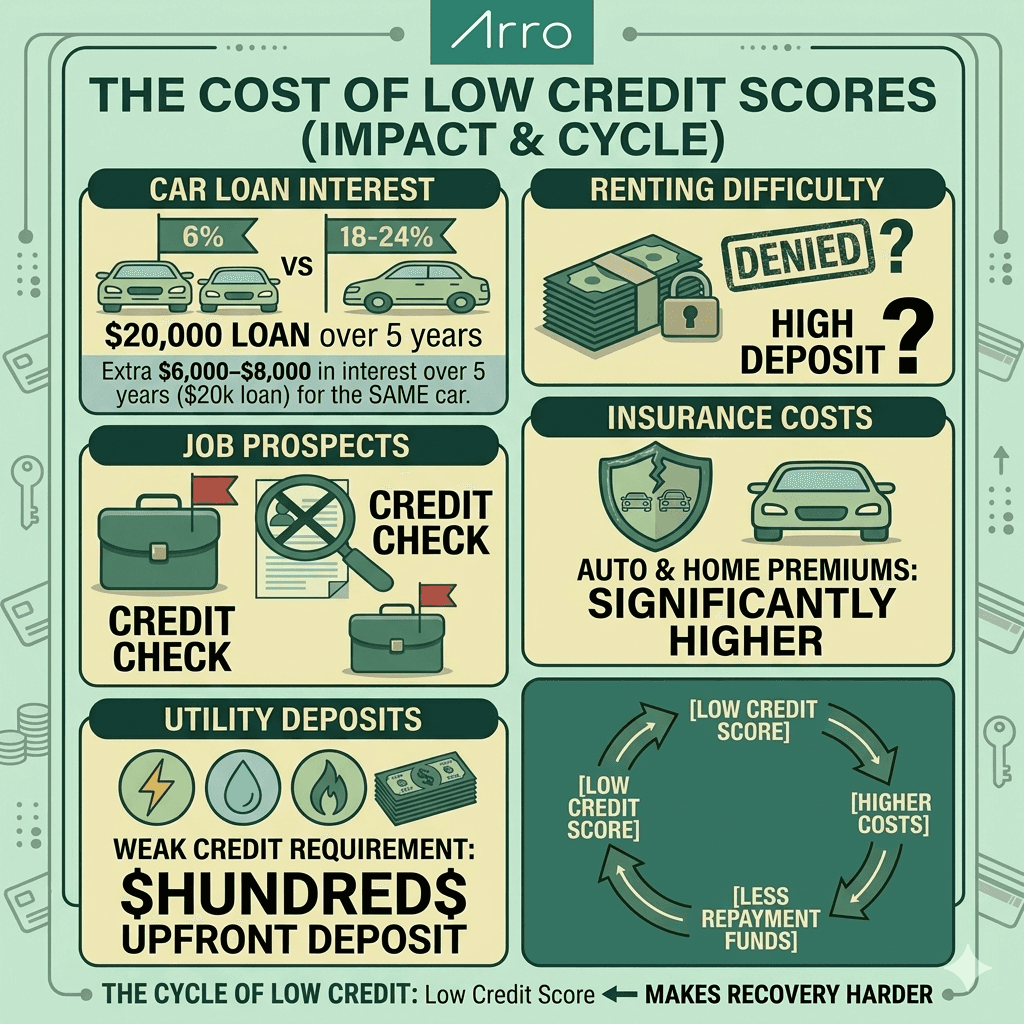

The Real-World Cost Of A Low Credit Score

This is where a low credit score turns into real-life consequences. A score in the poor range affects far more than just your ability to borrow.

A low credit score doesn’t just limit access. It quietly raises the cost of almost everything in your life. Over time, those extra costs add up, making it harder to get ahead and easier to fall behind. Improving your credit isn’t just financial housekeeping; it’s a way to break that cycle and regain control.

Also, read:

Swipe Right On Your Credit Score: Fall in Love With Better Credit This Valentine's Day

Where Do I Start? How To Build Credit If You Don’t Have A Credit Score

There Is No Such Thing As A Permanent Score

This is the most important thing to understand about the lowest possible credit score, or any low score: it is a snapshot of the past, not a life sentence.

Every negative item on your credit report has an expiration date. Late payments, collections, and most other negative marks drop off after seven years. A Chapter 7 bankruptcy disappears after ten years. And crucially, the older a negative item gets, the less impact it has on your current score, even before it drops off entirely.

More importantly, positive behavior starts working in your favor almost immediately. Your credit score is a living calculation that updates whenever new data is reported. When you make an on-time payment, it gets recorded. When you pay down a balance, your utilization drops. When a new account in good standing appears, your mix improves. These changes do not happen overnight, but they do happen.

What this means practically: the best time to start building credit was years ago, but the second-best time is right now.

How To Start Climbing From A Low Score

Recovery looks different depending on where you are starting from, but the fundamentals are the same, whether your score is near the lowest credit score or just lower than you would like.

Pay on time: Payment history makes up 35% of your score. One missed payment can set you back for months, while consistent on-time payments steadily rebuild your profile. Set up AutoPay for at least the minimum to avoid mistakes.

Lower your credit utilization: High balances hurt your score. Bringing utilization down, even from 90% to 50%, can help quickly. Aim for under 30%, and ideally below 10% for the best results.

Add positive, reporting accounts: Building credit requires accounts that report consistently. Tools like Arro Credit Builder help by reporting your monthly payments to all three credit bureaus, Experian, Equifax, and TransUnion, thereby strengthening your profile across the board.

Check for errors: Mistakes on credit reports are common and can drag your score down. Review your reports regularly at AnnualCreditReport.com and dispute any inaccuracies.

Be selective with applications: Each hard inquiry can lower your score slightly. When your score is low, those drops matter more. Apply selectively and prioritize options that use soft checks when possible.

Stay consistent and patient: Credit improvement takes time, but results can show within 6–12 months. Progress isn’t always linear, but consistent habits lead to steady gains.

No Credit VS. Low Credit: What It Means And How To Move Forward

Being “credit invisible” can be just as limiting as having a low credit score. The difference is simple: you haven’t made mistakes; the system just has no data on you yet. This is common for young adults, new U.S. residents, or anyone who has relied on cash or debit, but lenders still see it as a risk.

At the other end, a very low score (near 300) can result from a negative history, missed payments, high balances, or major financial setbacks. While the causes differ, the outcome is similar: limited access to credit, higher costs, and fewer financial options.

The path forward is the same in both cases: build positive, consistent data. Open accounts that report to all three major credit bureaus, make every payment on time, keep balances low, and avoid unnecessary applications. Whether you’re starting from zero or rebuilding, these actions move your score in the right direction.

Tools like the Arro Credit Builder are designed to support that process. With no hard credit check or deposit required, it helps you establish a payment history and gives you a clear path to stronger credit over time.

You also get guidance from Artie, your AI Money Coach, who helps you understand how each action impacts your score so you’re not just building credit, you’re learning how to manage it.

Start Building Your Credit Today

FAQ

Can the lowest credit score ever go below 300?

For the standard FICO and VantageScore models used in most consumer lending, 300 is the absolute floor. However, some industry-specific FICO models designed for auto loans or credit cards use a scale of 250 to 900, with 250 as the lowest possible credit score in those contexts. For everyday purposes, you will virtually never encounter those specialized models.

Does having the lowest possible credit score mean I will never get approved for anything?

No. Even borrowers near the lowest possible credit score can access certain financial products, typically secured credit cards (which require a deposit), credit-builder loans, or products specifically designed for subprime borrowers. What changes is the cost: higher interest rates, larger deposits, and more limited choices. The goal is to use those accessible products strategically to build a history that opens better doors over time.

How long does it take to recover from a score near the lowest possible credit score?

It depends heavily on what caused the low score in the first place. If the main issue is a thin file with no derogatory marks, a consistent credit-builder approach can produce a scoreable credit file within three to six months and meaningful score improvement within a year. If the file includes bankruptcies, charge-offs, or collections, the timeline is longer, but progress still happens. Most negative items lose their scoring impact significantly within two to three years of being reported, even before they drop off the report entirely at the seven-year mark.

Is the lowest possible credit score the same as having no credit score?

No, these are two different situations. Someone with the lowest credit score still has a credit file, but it contains mostly negative information. Someone with no credit score (also called "credit invisible") has a file that is too thin to generate a reliable score, typically because they have fewer than two active accounts or have not had any credit activity in the past six months. Both situations create barriers to accessing credit, but the solutions are slightly different: credit-invisible consumers need to build a positive history from scratch, while those near the floor need to add positive data while waiting for older negatives to age off.

Can I check where my score falls without making it worse?

Yes. Checking your own credit score is classified as a soft inquiry, which has zero impact on your score. You can check it as often as you like without any penalty. Hard inquiries, the kind that temporarily lower your score, only happen when you formally apply for new credit and authorize a lender to pull your full report. When you are working to recover from a low score, using soft-pull monitoring tools to track your progress is not just safe.

References

United States Courts. Alternatives to Chapter 7