Team Arro

Table of Content

What Is A Credit Card Hardship Program?

Common Types Of Hardship Relief

When Should You Contact Your Lender?

How To Prepare Before You Reach Out

Step-by-Step: Talking To Your Lender

Hardship Letter Templates You Can Use Today

What Happens After You Request Relief?

What If You're Denied?

Protecting Your Credit During Financial Hardship

Start Building Credit With Confidence

FAQs

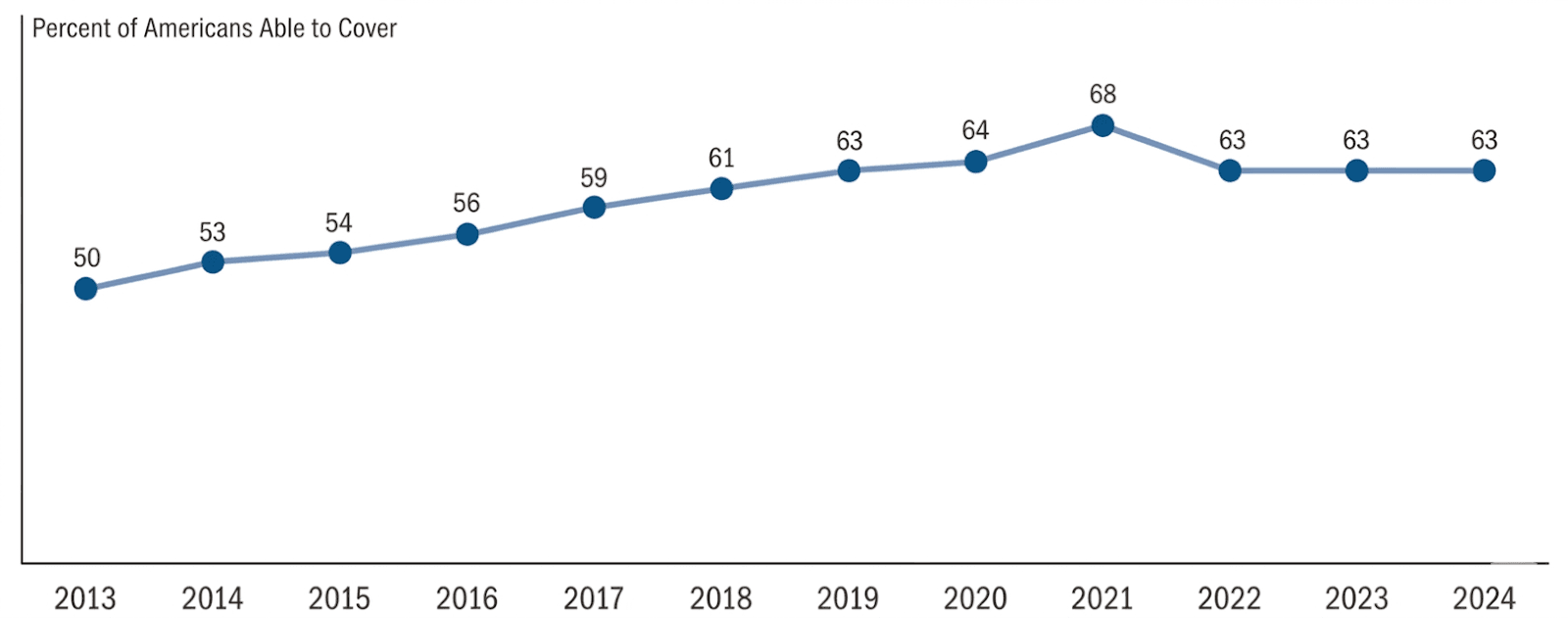

Life doesn't always go according to plan. A job loss, medical emergency, or unexpected expense can flip your finances upside down. According to a Federal Reserve study, nearly 37% of Americans would struggle to cover a $400 emergency with cash.

Share of Americans Able to Cover a $400 Emergency Expense (2013–2024)

Source: The Federal Reserve

When credit card payments feel overwhelming, many issuers offer a credit card hardship program that can lower payments, reduce interest, or provide temporary relief. If you’re unsure how to ask, this guide explains how these programs work and how to communicate with lenders effectively.

In this article, we'll cover common hardship relief types, when to contact your lender, preparation steps, conversation strategies, and actionable letter templates you can customize today.

Key Takeaways

Credit card hardship programs offer temporary relief through pauses, lower rates, or modified payments.

Contact lenders early, before falling behind, to maximize your negotiating power and relief options.

Hardship letters confirm verbal agreements in writing and create documentation for your records.

Programs typically last 3 to 12 months and require proof of genuine financial need.

Some lenders won't report late payments if you're enrolled in their hardship program.

Prepare documentation, such as pay stubs or termination letters, to strengthen your relief request.

What Is A Credit Card Hardship Program?

A credit card hardship program is a temporary assistance option that creditors offer to help you manage your debt when you're going through genuine financial difficulty. Think of it as a safety net designed for moments when life throws you off balance, whether that's a job loss, medical crisis, divorce, or natural disaster.

These programs aren't advertised on billboards or website homepages, but they exist at most major credit card companies. The goal is simple: help you avoid default while giving you breathing room to stabilize your finances.

What Qualifies As Financial Hardship?

Lenders typically recognize several situations as legitimate hardship:

Job loss or reduced income (furlough, layoff, hour cuts)

Medical emergencies (unexpected hospital bills, long-term illness)

Death in the family (especially if it affects household income)

Divorce or separation (sudden change in financial responsibilities)

Natural disasters (hurricanes, floods, fires that impact your home or income)

Military deployment (especially if it reduces household income)

The key is that the hardship must be unforeseen and temporary. Lenders want to see that you had the ability to pay before the crisis hit and that you'll be able to resume payments once you recover.

A credit card hardship program is a bridge to get you through a rough patch. Most programs last between 3 and 12 months, though some may offer extensions depending on your circumstances.

Common Types Of Hardship Relief

When you contact your lender about entering a credit card hardship program, they may offer one or several of these relief options. Understanding what's available helps you know what to ask for.

Payment Pause or Deferral: Your lender temporarily pauses payments for a short period while you get back on your feet.

Reduced Minimum Payment: Your required monthly payment is lowered to make it easier to stay current.

Lower Interest Rate: Your APR is temporarily reduced so more of your payment goes toward your balance.

Waived Fees: Late, over-limit, or annual fees may be waived during the hardship period.

Extended Payment Plan: Your balance is spread over fixed monthly payments for a longer repayment timeline.

Not every lender offers the same options, but most will work with you if you ask. Providing documentation helps, and you should always confirm how relief programs affect your credit.

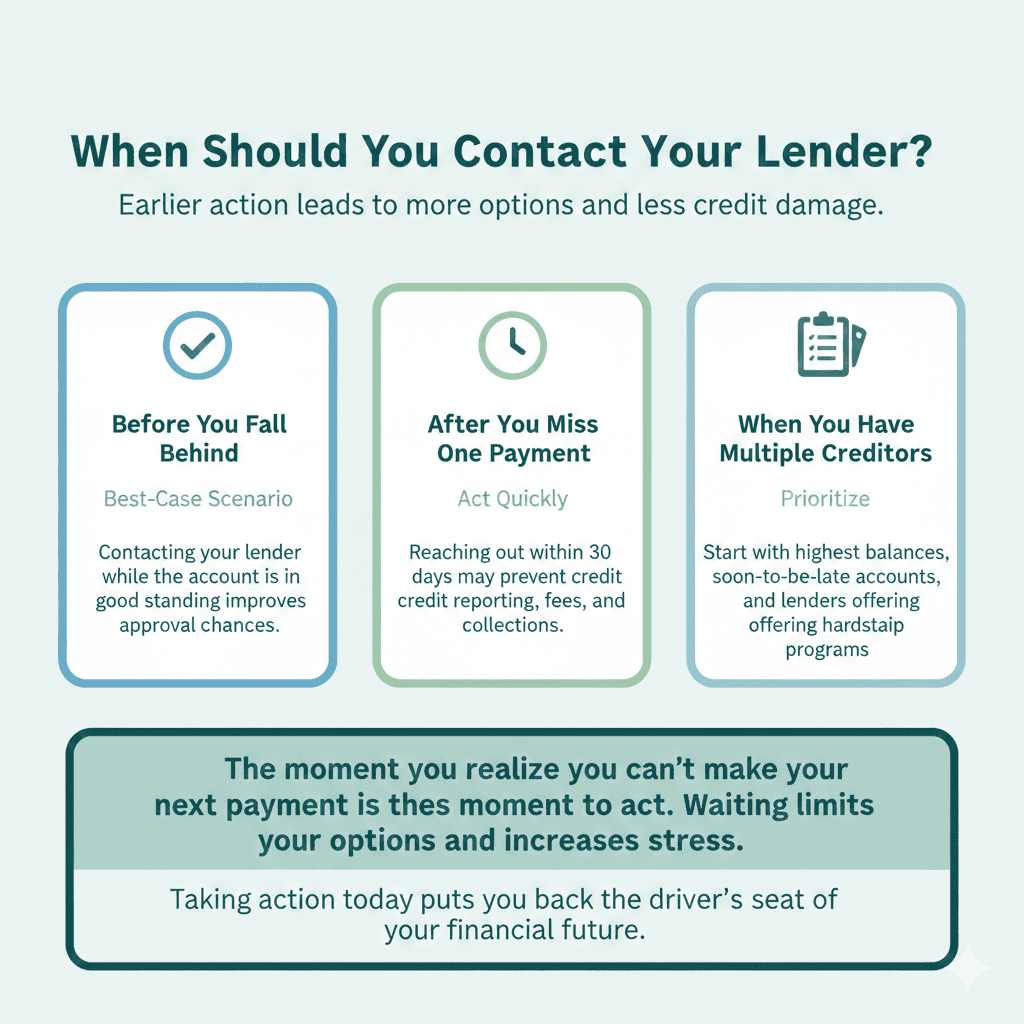

When Should You Contact Your Lender?

Timing matters when you're requesting relief through a credit card hardship program. The earlier you reach out, the more options you'll have and the better your chances of avoiding credit damage.

Before You Fall Behind

The best time to contact your lender is before you miss a payment. Reaching out early, while your account is in good standing, makes lenders more willing to help and can significantly increase your chances of getting a favorable payment arrangement.

After You Miss One Payment

If you’ve missed one payment, don’t panic, but act fast. Contacting your creditor within 30 days may help you avoid credit reporting, extra fees, and collections, especially if you’re honest about your situation.

When You're Facing Multiple Creditors

If you’re struggling with multiple cards, prioritize outreach to the highest balances, accounts closest to being late, and those offering hardship programs. You don’t need to call everyone at once, but aim to contact each creditor within a week.

The moment you realize you can't make your next payment is the moment you should pick up the phone or start drafting a hardship letter. Waiting only shrinks your options and increases your stress.

How To Prepare Before You Reach Out

Walking into a conversation about a credit card hardship program unprepared can leave you flustered and reduce your chances of getting the relief you need. A little preparation goes a long way in making the process smoother and more successful.

Gather Your Documentation

Before you contact your lender, collect evidence that supports your hardship claim. This might include:

Termination or furlough letter from your employer

Recent pay stubs showing reduced income

Medical bills or hospital statements if your hardship is health-related

Divorce decree or separation papers, if applicable

Death certificate if you've lost a family member who contributed to the household income

Insurance claim documents for property damage or disaster relief

You don't need every piece of paper imaginable, but having 2 to 3 documents ready shows your lender that this is a real situation, not an excuse.

Know Your Numbers

Be prepared to discuss your financial situation in concrete terms. You should know your current monthly income (what you're bringing in right now), your monthly expenses (rent/mortgage, utilities, groceries, transportation, the essentials), and what you can realistically afford to pay. Don't lowball or exaggerate; be honest about what you can manage.

Lenders want to see that you've thought this through. If you say, "I can't pay anything," they may push back. But if you say, "I can pay $75 instead of $200 for the next three months," that gives them something concrete to work with.

Review Your Account Details

Before you call or write, pull up your credit card account and note your current balance, your minimum payment amount, your interest rate, and any recent fees or charges. Having these details at your fingertips helps the conversation flow more smoothly and shows the representative that you're engaged and informed.

Decide What You're Asking For

Don't leave it up to the lender to guess what you need. Be clear about the type of relief you're requesting. For example: "I'd like to pause my payments for two months while I search for a new job," "Can we reduce my minimum payment to $50 for the next six months?" or "I'm hoping you can lower my interest rate temporarily so more of my payment goes toward my balance."

The more specific you are, the easier it is for the representative to say yes or offer an alternative that still helps. Write down your talking points before you call so you don't forget important details, practice your explanation with a friend or family member if you're nervous, and keep a notepad handy during the call to jot down names, reference numbers, and next steps.

With the right preparation, you'll walk into the conversation feeling confident instead of desperate, and that confidence can make all the difference in how your lender responds.

Step-by-Step: Talking To Your Lender

Once you're ready, contact your credit card company to enroll in a hardship program. Whether you're calling or writing, here's how to make the conversation as effective as possible.

Step 1: Contact The Right Department

Ask to be transferred to the hardship, financial assistance, or customer solutions department. These teams are trained to handle credit card hardship program requests and can approve relief. If the first representative isn’t familiar, politely ask if there’s a department for financial hardship or payment assistance.

Step 2: Explain Your Situation Clearly

Be honest and specific about what happened, when it started, and why you can’t make your current payment. Share only what’s necessary, such as job loss, medical issues, or reduced income. Clear details help the lender understand your situation and respond appropriately.

Step 3: Make A Specific Request

Clearly state the type of relief you’re asking for, such as a payment deferral, reduced minimum, or lower interest rate. Listen carefully if an alternative is offered and ask questions before agreeing. Don’t feel pressured to accept terms that won’t work for you.

Step 4: Ask About Credit Reporting

Before agreeing, ask how the hardship program will be reported to the credit bureaus. Confirm whether missed payments will be reported, and if your account can remain marked as current. Get clear answers so there are no surprises later.

Step 5: Get Everything In Writing

Request written confirmation of the agreement, including payment terms, duration, interest rate, and credit reporting details. If you don’t receive it within 5–7 business days, follow up. Verbal agreements aren’t enough.

Step 6: Follow Up With A Hardship Letter

Send a formal hardship letter to document the agreement and create a paper trail. Keep notes of who you spoke with, when, and what was agreed upon. Approach the process confidently. You’re working toward a solution, not asking for a favor.

Remember: you're not begging for a favor. You're working with your lender to find a solution that benefits both of you. Approach the conversation with confidence and clarity, and you'll be surprised by how willing most companies are to help.

Hardship Letter Templates You Can Use Today

A well-written hardship letter can make all the difference when you're requesting relief through a credit card hardship program. These templates give you a solid starting point. Just customize them with your specific details and situation.

Template 1: Request for Payment Reduction

Use this template when you can still afford to make some payment, but not your current minimum.

[Your Name]

[Your Address]

[City, State ZIP Code]

[Phone Number]

[Email Address]

[Date]

[Credit Card Company Name]

Attn: Hardship Department

[Company Address]

[City, State ZIP Code]

Re: Request for Temporary Payment Reduction – Account #[Your Account Number]

Dear [Credit Card Company Name],

I am writing to request temporary enrollment in your credit card hardship program due to unforeseen financial difficulties.

On [specific date], I [experienced job loss/had my hours reduced/faced a medical emergency/other qualifying hardship]. As a result, my monthly income has decreased from approximately $[previous amount] to $[current amount], making it impossible for me to meet my current minimum payment of $[current payment amount].

I am committed to honoring my debt and maintaining my account in good standing. I am requesting a temporary reduction in my minimum payment to $[proposed amount] for [3 to 6 months], which I can afford given my current budget. I expect to resume regular payments by [estimated date] once my financial situation stabilizes.

I have attached [list any supporting documents: termination letter, recent pay stubs, medical bills, etc.] to verify my circumstances. I would appreciate written confirmation of any hardship arrangement we agree upon, including how it will be reported to the credit bureaus.

Thank you for your consideration and understanding during this difficult time. I can be reached at [phone number] or [email address] to discuss this request further.

Sincerely,

[Your Signature]

[Your Printed Name]

Template 2: Request for Payment Pause/Deferral

Use this when you need to temporarily stop making payments altogether.

[Your Name]

[Your Address]

[City, State ZIP Code]

[Phone Number]

[Email Address]

[Date]

[Credit Card Company Name]

Attn: Customer Solutions Department

[Company Address]

[City, State ZIP Code]

Re: Request for Payment Deferral – Account #[Your Account Number]

Dear [Credit Card Company Name],

I am writing to request enrollment in a credit card hardship program to defer my payments temporarily.

Due to [specific hardship: job loss, medical emergency, natural disaster], which began on [date], I currently have no income and am unable to make any payment toward my credit card balance. I am actively [job searching/recovering/rebuilding] and anticipate resuming payments by [estimated date].

I am requesting a [1 to 3-month] payment deferral to allow me time to stabilize my financial situation. I understand that interest may continue to accrue during this period, and I am prepared to address the deferred payments once I am back on my feet.

Please confirm in writing the terms of this deferral, including:

The duration of the deferral period

Whether interest will continue to accrue

How this will be reported to credit bureaus

Steps required to resume regular payments after the deferral period ends

I have attached [supporting documentation] to verify my hardship. I appreciate your willingness to work with me and can be reached at [phone number] or [email address].

Sincerely,

[Your Signature]

[Your Printed Name]

Template 3: Request for Interest Rate Reduction

Use this when you can continue making payments but need a lower interest rate to make progress on your balance.

[Your Name]

[Your Address]

[City, State ZIP Code]

[Phone Number]

[Email Address]

[Date]

[Credit Card Company Name]

Attn: Hardship Assistance Team

[Company Address]

[City, State ZIP Code]

Re: Request for Temporary Interest Rate Reduction – Account #[Your Account Number]

Dear [Credit Card Company Name],

I am writing to request temporary enrollment in your credit card hardship program to reduce my current interest rate.

On [date], I experienced [hardship event], which has significantly impacted my financial situation. While I can continue making my minimum monthly payments, my current APR of [current rate]% means that very little of my payment reduces my principal balance.

I am requesting a temporary reduction in my interest rate to [proposed rate, such as 0% or a specific lower percentage] for [6 to 12 months]. This would allow me to make meaningful progress on my balance while I work to improve my financial circumstances.

I have been a customer in good standing since [date you opened the account] and have made [X consecutive on-time payments/other positive account history]. I am committed to continuing regular payments and would greatly appreciate this temporary relief.

Please send written confirmation of any interest rate adjustment, including the new rate, the effective dates, and how this will appear on my credit report.

Thank you for your consideration. I can be reached at [phone number] or [email address].

Sincerely,

[Your Signature]

[Your Printed Name]

Template 4: No Ability to Make Any Payments

Use this only if you truly have zero income and cannot make any payment at this time. Be prepared to provide extensive documentation.

[Your Name]

[Your Address]

[City, State ZIP Code]

[Phone Number]

[Email Address]

[Date]

[Credit Card Company Name]

Attn: Hardship Department

[Company Address]

[City, State ZIP Code]

WITHOUT PREJUDICE

Re: Financial Hardship Notification – Account #[Your Account Number]

Dear [Credit Card Company Name],

I am writing to inform you that I am currently unable to make payments toward my credit card balance due to severe financial hardship.

As of [date], my only income consists of [unemployment benefits/disability payments/government assistance/no income], which is insufficient to cover my basic living expenses. I am unable to make any payment at this time.

I respectfully request that you:

Pause all collection activities while I work to improve my situation

Communicate with me in writing only (please do not contact me by phone)

Consider enrolling me in your credit card hardship program with deferred payments until my circumstances improve

If my financial situation changes and I am able to resume payments, I will contact you immediately to make appropriate arrangements. I have attached the [income/hardship] documentation for your review.

I appreciate your patience and understanding during this extraordinarily difficult time. Please send all correspondence to the address above.

This letter is provided solely to notify you of my current financial circumstances and does not constitute an acknowledgment of the debt described above.

Sincerely,

[Your Signature]

[Your Printed Name]

Important Tips For Using These Templates:

Always send your hardship letter via certified mail or email with a read receipt to ensure proof of delivery. Keep a copy of every letter you send for your records. Follow up with a phone call 7 to 10 days after sending if you haven't received a response. Never provide false information or exaggerate your hardship. Creditors can verify your claims.

These templates provide a clear, professional way to communicate with your lender and request the relief you need through a credit card hardship program.

What Happens After You Request Relief?

Once you've contacted your lender and submitted your hardship letter, what comes next? Understanding the process can help ease your anxiety and ensure you're taking the right steps to stay on track.

The Review Process

Most credit card companies will review your credit card hardship program request within 5 to 10 business days. During this time, they may verify the documentation you provided and review your account history and payment track record. They may also assess your current financial situation based on what you've shared and determine which relief options they can offer.

Some lenders make decisions quickly (within 2 to 3 days), while others take longer, especially if they need additional documentation from you. Don't panic if you don't hear back immediately. Follow up with a polite phone call if you haven't received a response within two weeks.

Approval And Agreement

If your request is approved, your lender will send you a formal agreement outlining the terms of your credit card hardship program enrollment. This agreement should include the type of relief granted (payment pause, reduced payment, lower interest, etc.), the duration of the hardship program with start and end dates, your new payment amount and due dates, any fees that have been waived, and how your account will be reported to credit bureaus.

Read this agreement carefully before you sign or accept it. Make sure you understand what's expected of you and what happens if you don't meet those expectations. If anything is unclear, call and ask questions.

Your Responsibilities During The Program

Being enrolled in a credit card hardship program doesn't mean you can forget about your credit card entirely. You'll still need to make your agreed-upon payments on time (even if they're reduced or zero during a deferral period, stick to the schedule), avoid using the card for new purchases unless explicitly allowed by your agreement (most programs freeze your account), keep your lender updated if your situation changes significantly (for better or worse), and respond to any requests for updated documentation since some programs require periodic check-ins.

Failing to meet these conditions may result in your lender terminating the hardship arrangement and returning your account to normal terms, including reinstatement of any missed payments or fees.

What If You're Denied?

Not every credit card hardship program request gets approved. If your lender denies your request, don't give up. Ask why you were denied, since the representative should be able to explain the reason. Perhaps you didn't provide sufficient documentation, or your hardship doesn't meet their criteria.

Request to speak with a supervisor because sometimes a manager has more flexibility or authority to approve exceptions. Provide additional documentation if the issue was insufficient proof of hardship, gather more evidence, and resubmit your request. Explore alternatives: even if you're denied enrollment in a formal hardship program, your lender may still be willing to waive a late fee, offer a one-time payment extension, or work out a different arrangement.

Consider credit counseling if you're struggling with multiple creditors or your hardship is long-term, since a nonprofit credit counseling agency can help you negotiate with lenders and create a debt management plan.

Keep detailed records of every conversation, email, and letter related to your hardship request. Set reminders for important dates (such as when your hardship period ends or when payments resume). If your financial situation improves before the hardship period ends, contact your lender. Resuming normal payments early can strengthen your relationship with them.

The key is to stay engaged and proactive throughout the process. Your lender wants to see that you're committed to getting back on track, and your actions during the hardship period will reinforce that.

Also Read:

Pass The Deposit: How Credit Impacts Security Deposits, Utility Bill Deposits, And Phone Plans

Streaming, Subscriptions, And Small Bills: Which Ones Can (And Can’t) Help Your Credit?

Balance Transfer Or Personal Loan: What Is The Right Fit For You?

Protecting Your Credit During Financial Hardship

One of the biggest fears people have about entering a credit card hardship program is the impact on their credit score. While any financial difficulty carries some risk to your credit, there are steps you can take to minimize the damage.

Understanding Credit Reporting During Hardship

How a credit card hardship program affects your credit report depends on how your lender reports it. Some accounts stay marked as “current” if you make agreed-upon payments, while others may include a hardship or deferred payment note that doesn’t directly hurt your score but can be visible to lenders. In some cases, a forbearance or modification code may appear, which is less damaging than missed payments or collections.

Avoid These Credit Mistakes

Even during hardship, avoid actions that cause extra credit damage. Stay in touch with your lender, don’t apply for new credit, avoid maxing out other cards, and keep up with essential bills like your mortgage and utilities whenever possible.

Rebuilding After The Hardship Period Ends

After your credit card hardship program ends and your finances stabilize, focus on rebuilding your credit. Make on-time payments consistently, pay down high-interest balances first, and review your credit reports for accuracy. If your score took a hit, an unsecured credit card designed for rebuilding, like the Arro Card, can help you establish a positive credit history again.

The good news is that credit scores are resilient. Most of the negative impacts of hardship programs fade over time, especially if you return to responsible credit behavior. According to FICO, even a single missed payment can be offset by several months of on-time payments.

Remember: protecting your credit during hardship is about damage control and staying engaged with your creditors. The more proactive you are, the better your credit will perform over the long term.

Start Building Credit With Confidence

Financial hardship doesn’t define you, and asking for help shows strength. Whether you’re navigating a credit card hardship program or rebuilding after a setback, these strategies help you communicate with lenders and protect your financial future, setting you up for what comes next.

At Arro, we believe building credit shouldn't be confusing, expensive, or out of reach, especially when you're recovering from financial difficulty. That's why we've created the Arro Card, to support you in learning, earning, and growing, all within one simple app.

With no hard credit checks, no deposit, and 1% cash back on gas and groceries, Arro makes it easy to start rebuilding your credit while rewarding your everyday spending. You'll also get access to Artie, your personal AI Money Coach, who's available 24/7 to answer questions, celebrate your wins, and help you make smart financial decisions.

Every on-time payment you make, every lesson you complete, and every small step forward helps you unlock higher credit limits and better credit health. Thousands of Arro members are already building stronger credit and finding the process clearer and more rewarding than they expected.

Ready to start your own? See how easy it can be to build credit with confidence, one step at a time.

FAQ

What documentation do I need for a hardship program?

You'll typically need proof of your financial situation, such as termination letters, recent pay stubs showing reduced income, medical bills related to health hardships, or documentation of disasters. Having 2 to 3 relevant documents ready demonstrates your hardship is genuine and helps speed approval. Don't exaggerate; creditors verify claims.

Can I negotiate if my hardship request is denied?

Absolutely. Ask why you were denied and request to speak with a supervisor who may have more authority. Provide additional documentation as needed, or explore alternative relief options such as one-time fee waivers or payment extensions. Nonprofit credit counselors can also help negotiate on your behalf.

How can I determine whether my lender offers hardship programs?

Most major credit card issuers offer some form of assistance, though they may call it "financial relief," "payment assistance," or "customer solutions." Call and ask specifically for the hardship or financial assistance department; these programs exist but aren't always advertised.

Can I use my card during a hardship program?

Most credit card hardship programs freeze your account, preventing new purchases while you receive relief. This prevents the accumulation of more debt during a vulnerable period. Once your hardship period ends and you resume regular payments, your lender may reactivate your account and review your specific agreement.

What's the difference between forbearance and deferral?

Forbearance typically means reduced or paused payments with interest continuing to accrue, often with specific reporting to credit bureaus. Deferral usually means payments are paused for a set period, with the balance deferred to the end of your loan term. Both are temporary relief options available through credit card hardship programs.