Abby Butkus

Table of Content

What It Means To Pay Your Credit Card Early

How Grace Periods Work

Is It Better To Pay Credit Card Early Or On Time?

Should You Make Multiple Payments Per Month

Build Credit With Confidence, One Smart Step At A Time

FAQs

Paying your credit card early can feel confusing when you’re still learning how credit works or worrying you might be doing it “wrong.” If you’ve ever asked, “Is it better to pay credit card early or on time?”, you’re not alone. After all, U.S. credit card holders reported an average utilization rate of 20.7% as of March 2025. Early payments can help you stay in control, reduce stress, and build healthier habits.

To guide you through it all, in this article, we will explore what early payments mean, how grace periods work, compare paying early vs on time, look at “too early” payments, review monthly payment rhythms, and cover lesser-known considerations.

Key Takeaways

Paying early can help lower your credit utilization and improve your score.

If you’re asking, “Is it better to pay credit card early or on time?” consistency wins first; early payment helps second.

Making multiple smaller payments can reduce stress and keep your utilization low.

Grace periods give you an interest-free window if you pay in full.

Early payments aren’t mandatory, but when they fit your rhythm, they can be very beneficial.

Pick a payment strategy you’ll stick with month after month.

What It Means To Pay Your Credit Card Early

Paying early simply means making a payment before the due date on your statement. If you’ve ever wondered “Is it better to pay credit card early or on time?”, this is the starting point. An early payment still counts as “on time”, and nothing negative comes from doing it ahead of schedule. Many people choose to pay early because it feels calmer and gives them a sense of control.

Paying early also brings your balance down sooner, which can make your month feel more organized. It helps you stay aware of what you are spending and can make your everyday decisions feel more intentional. For many people, the benefits show up in simple but meaningful ways, including:

A clearer picture of how much money is truly available

Less pressure as the due date gets closer

A steadier rhythm for tracking spending and staying aligned with personal goals

These small changes add up, and paying early often becomes a habit that makes your credit card feel easier to manage, not something to stress over.

How Grace Periods Work

Most credit cards offer a grace period, usually about 21 to 25 days between the day your statement closes and the day your payment is due. During this time, you can pay your balance in full and avoid interest, as long as you have not carried a balance from the previous cycle. If you are asking whether it's better to pay credit card bills early or on time, understanding this window really helps you see why timing matters.

The grace period is a built-in buffer that gives you room to manage your spending and your payment without feeling rushed. It also helps you align your payments with your income or budget in a way that feels steadier. Many people find that knowing how much time they have makes credit feel a lot less stressful.

A grace period can support you by giving you:

A clear window where paying in full keeps interest away

Extra time to review your purchases and make sure everything looks right

Space to plan your payment in a way that fits your monthly rhythm

Using your grace period effectively helps you stay ahead, stay organized, and feel confident in how you manage your credit card.

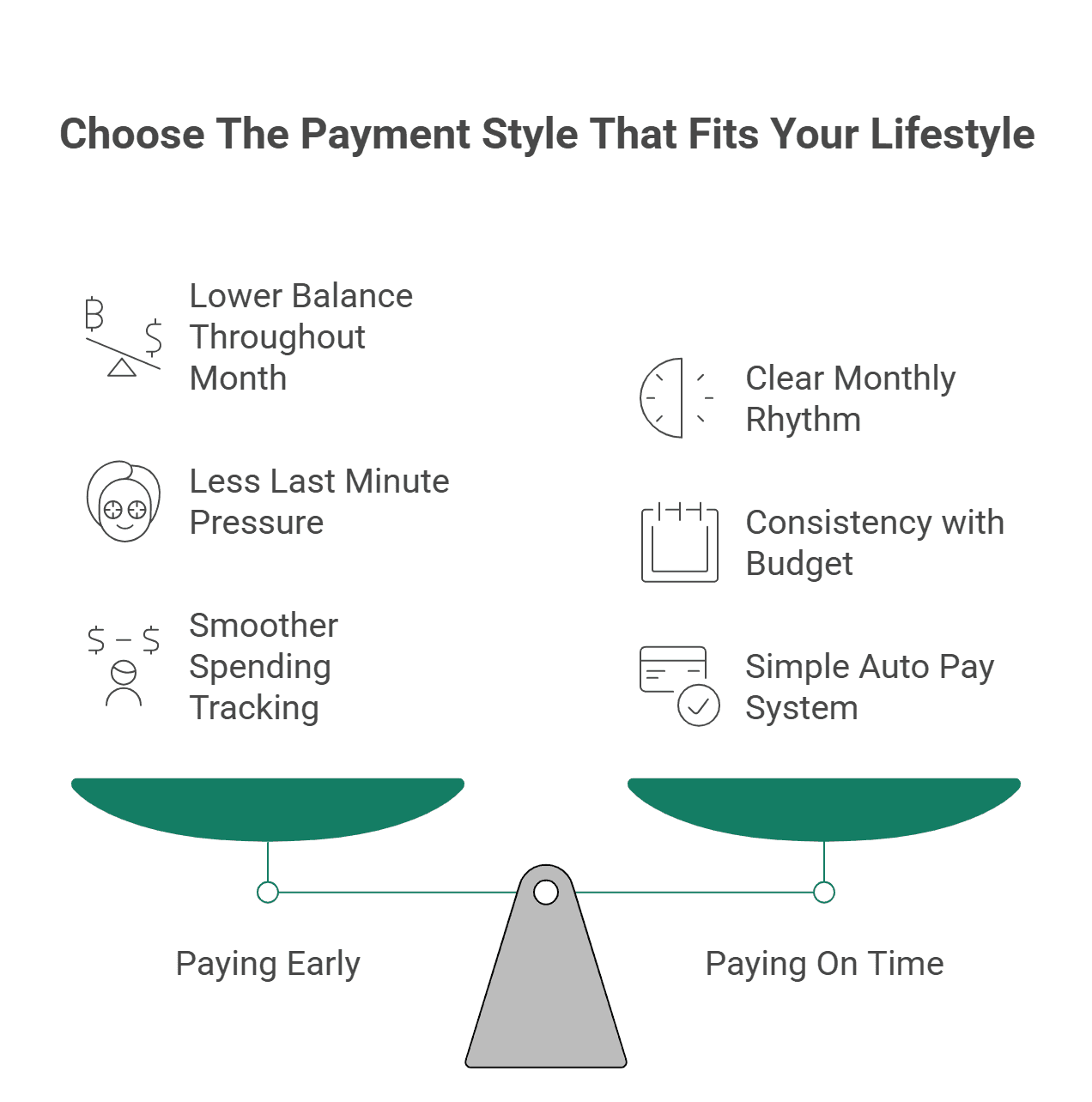

Is It Better To Pay Credit Card Early Or On Time?

This is the question a lot of people come back to: is it better to pay credit card early or on time? The simple truth is that both approaches work, and both support your credit as long as you pay by the due date. The difference comes down to how you like to manage your month and what helps you feel most in control.

Why Paying Early Helps

Paying early gives you more breathing room. It brings your balance down sooner and helps you feel on top of things without the pressure of a deadline. People who pay early often say it makes their money feel more organized and predictable.

Early payments can help you by offering:

A lower balance throughout the month, which can feel more manageable

Less last-minute pressure around your payment date

A smoother, steadier rhythm for tracking your spending

These small wins add up, and early payments become a simple habit that helps you stay calm and in control.

Why Paying On Time Still Works

Paying on time is just as valid and is often the easiest option for people who like a simple routine. If your budget is steady and you rely on a predictable schedule, paying on time might feel more natural.

On-time payments can help you by giving you:

A clear monthly rhythm that is easy to follow

Consistency when budgeting around payday

A simple system if you use auto pay

If this kind of structure fits your lifestyle, paying on time can feel straightforward and stress-free.

So, is it better to pay a credit card early or on time? Early payments offer a slight advantage, especially if they help you stay organized, but the real key is consistency. Choosing a method you can stick with month after month will make the biggest difference in how confident you feel managing your credit.

Should You Make Multiple Payments Per Month

Yes, many people find that making a few smaller payments feels easier than one big one. Multiple early payments work like small check-ins with your account. They help you stay connected to your spending and keep things from piling up all at once.

Why Multiple Payments Help

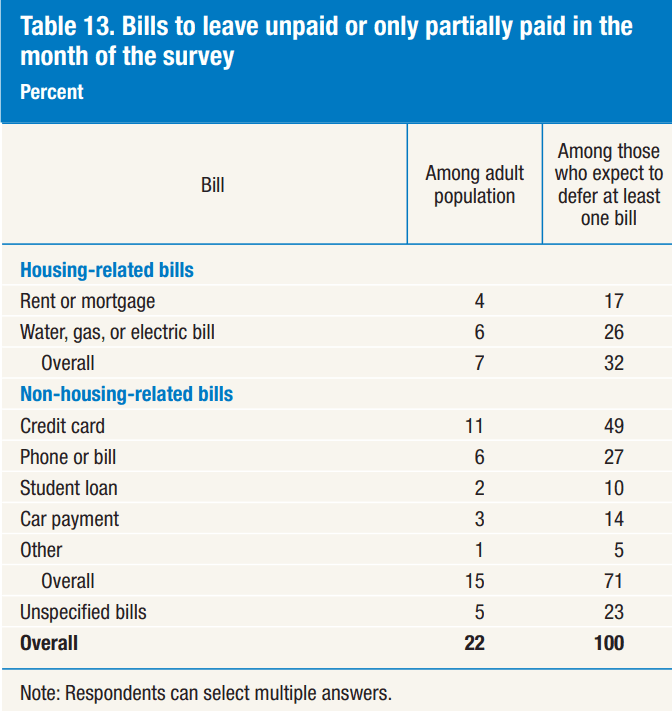

In fact, only 45% of U.S. cardholders always pay their full credit card balance each month. Making several payments throughout the month can support you in simple, practical ways.

Source: Report on the Economic Well-Being of U.S. Households

Your balance stays steadier instead of jumping up and down

Your bill feels more manageable when it is broken into smaller pieces

Your payments can line up with your paycheck, which keeps things orderly

If this kind of rhythm helps you feel calm and organized, multiple payments can be a great way to stay in control. The goal is to choose the pace that keeps your stress low and your confidence high.

Also Read:

How to Build Credit: Your Complete Guide to Building Credit from Scratch

Ask the Experts: How to start your side hustle and earn extra income

Build Credit With Confidence, One Smart Step At A Time

Early payments offer a small advantage, but the biggest impact comes from staying consistent and building habits you can maintain. Small steps, repeated over time, are what move your credit forward.

And when you are ready to build credit with support, guidance, and zero judgment, Arro is here for you.

At Arro, we believe credit should feel simple and accessible, not confusing or out of reach. That is why we created a card and app that help you learn, earn, and grow, all in one place.

With no hard credit checks, no deposit, and 1 percent cashback on gas and groceries, Arro turns everyday spending into meaningful progress.

You will also meet Artie, your AI Money Coach, who is there anytime you need answers, motivation, or a quick confidence boost.

Every on-time payment, every lesson, and every small win helps you unlock higher limits and stronger financial health. Thousands of people are already growing their credit with Arro and feeling good about it.

Start building credit the easy way.

Download Arro App today

FAQs

Can my credit card issuer limit how much I’m allowed to pay at once?

Some issuers place temporary limits on unusually large payments, especially for new accounts or for security reasons. This doesn’t mean something is wrong; it’s simple fraud protection. If a payment ever fails for size, you can divide it into two smaller payments or verify your identity, ensuring everything clears smoothly and safely.

Do credit card payments affect my available credit immediately?

Not always. Some card issuers update available credit instantly, while others take a day or two. Even if it takes time to show, your payment still counts from the moment you submit it. If you need available credit quickly, knowing your issuer’s normal update speed helps you plan purchases without feeling limited or stressed.

Can paying with a mobile wallet or third-party app delay my payment?

Sometimes, yes. Payments made through bill-pay services or wallets like Apple Pay or your bank’s payment system may take an extra day or two to arrive. It isn’t harmful, it just takes longer. Paying directly through your credit card’s app or website usually offers the fastest processing and the least waiting around.

Does my payment method (bank transfer, debit card, etc.) matter?

Generally, yes. Bank transfers made inside your credit card’s app often process the quickest. External bill-pay tools can batch payments and send them later. If timing matters to you, using your card issuer’s own payment portal provides the most predictable, reliable experience for every monthly cycle.

Can I schedule payments in advance even if I’m not sure how much I’ll owe?

Yes, most issuers let you schedule flexible future payments. You can choose a fixed amount or let the system pay your entire statement once it's generated. If you’re unsure of the final total, scheduling a partial payment now and adding another later can help you stay ahead while keeping your budget comfortable and steady.