Arro Team

If you have a debit card and a credit card, do you really know the difference between them?

Table Of Content

The Benefits And Drawbacks Of Debit Cards

The Benefits And Drawbacks Of Credit Cards

What To Know About Fraud Protection And Credit Impact?

So, Which Card Should You Use?

Choosing The Right Card Based On Your Spending Habits

FAQs

Have you ever just grabbed one without thinking when you pay? It really doesn't matter which one you choose, right? Choosing between a debit card vs credit card isn’t as simple as it may seem.

Although these types of cards may look the same and require you to swipe them, their differences are more significant than just offering some level of fraud protection.

In this article, we’ll explain the key differences between each type of plastic card, including what is a debit card, and help you make a more informed decision when choosing between a debit card and a credit card.

Key Takeaways

Debit cards withdraw directly from your bank account and have no interest or fees.

Credit cards help build credit but can accrue interest if balances aren’t paid in full.

Debit cards don’t affect your credit score, but credit cards do.

Debit cards are simple to use, but they offer fewer perks and protections compared to credit cards.

Credit cards offer rewards like cashback or travel points, but they also come with fees and interest if not used responsibly.

If you want to avoid building debt, using a debit card is a safer choice than a credit card.

The Benefits And Drawbacks Of Debit Cards

When it comes to using plastic for payments, there are two main types of cards: debit and credit. Each type of card has its own advantages and disadvantages, and they can all have a different impact on your personal finances.

Each type of card has its own advantages and disadvantages, and they can all have a different impact on your personal finances.

What is a debit card? A debit card connects to your checking account. When you shop, the money is taken directly from your account. It often has a Visa or Mastercard logo, but is not a credit card.

What is a debit card used for? You can use it to make everyday purchases, pay for services, or withdraw cash from ATMs. It works like a direct link to the funds in your bank account.

The Benefits:

No interest charges; you don’t incur any interest.

No annual fees or late fees.

Helps you avoid accumulating debt; there’s no risk of falling into debt.

Limits overspending if you don’t have enough money available in your checking account.

Can be used at any retailer that accepts credit cards.

The Drawbacks:

Your checking account balance determines the spending limit on your debit card.

There are usually no perks or reward programs.

You may have to pay fees if you do not have enough funds in your account (NSF - non-sufficient funds)

These cards do not have fees unless an overdraft occurs, which may incur charges from your bank.

Debit cards are not always accepted for holds at hotels or car rentals.

While debit cards offer simplicity and help you stay on budget, they come with limits and fewer perks compared to credit cards, so it’s essential to know when to use them wisely.

The Benefits And Drawbacks Of Credit Cards

Simply put, credit cards are loans that let you borrow money, which must be repaid, often with interest if the balance isn't paid in full. Each purchase reduces your available credit, and you'll receive a monthly bill detailing your total owed by a due date. In contrast, debit cards withdraw directly from your checking account.

The Benefits

Helps you manage your budget by allowing you to buy now and pay when the bill is due.

Assists you in building your credit.

These cards offer perks such as cash back or travel rewards points on purchases.

Some credit cards offer additional warranty coverage on certain purchases, especially electronics, beyond the manufacturer's warranty.

The Drawbacks

Credit cards may have late fees, foreign transaction fees, and annual fees.

Interest charges apply when you don't pay your full credit card balance on time each month. A high interest rate will make it take longer to pay off your debt.

Can damage your credit if not used responsibly

Irresponsible use of credit cards can lead to significant credit card debt.

Your credit report includes a hard inquiry that can affect your score.

Many stores, like department stores or gas stations, offer their own credit cards that you can only use at those locations. These cards report to the credit bureaus, which means it’s important to make your payments on time to keep your credit score in good shape.

Retailers like department stores and gas stations often have their own credit cards that you can only use at their locations. These cards report to credit bureaus, so it’s important to make payments on time to keep your credit score healthy. Unlike these store cards, Arro only performs a soft inquiry when you apply for an Arro Card, ensuring that your credit score won't be negatively impacted.

What To Know About Fraud Protection And Credit Impact?

When choosing between these cards, two important features to think about are fraud protection and your credit score. We mentioned these briefly, but they deserve a closer look.

Fraud Protection

Nowadays, it can seem like card fraud is rampant. With threats ranging from skimmers at gas stations to data breaches online, it’s challenging to stay vigilant. If you find yourself facing fraudulent charges and need to file a claim, it’s important to understand the different levels of protection that vary based on the type of card you use.

Debit Cards

Purchases made with your debit card are covered by fraud protection through the Electronic Funds Transfer Act (EFTA). However, the protection isn’t as thorough and robust as it is for credit cards. Depending on how soon you report the fraud, you could be responsible for $0 to the full amount of fraud if it’s not caught quickly enough. Because your card is linked to your bank account, fraudulent charges can tie up funds in your checking account, leading to even more frustration.

If you’re wondering, can you dispute a debit card charge? The answer is yes, but it’s crucial to act fast. Reporting fraudulent activity immediately improves your chances of recovering the lost funds.

Credit Cards

The fraud protection offered on credit cards is more robust. If you have fraudulent purchases or unauthorized activity on your card, you’re only liable for up to $50 under the Fair Credit Billing Act (FCBA). Many card issuers offer $0 fraud liability on credit card fraud, making it an attractive card of choice. Your credit card company will quickly replace your compromised card, allowing you to continue using your credit line without an extended interruption.

2. Impact On Credit

Do all plastic cards affect your credit and your credit score? Whether you're trying to build up your credit or pay down debt, not all cards are created equal when it comes to your credit score.

Debit Cards

What is a debit card? It's a payment method that doesn’t affect your credit score and doesn’t require a credit check. When choosing between debit or credit at checkout, it impacts processing time and merchant fees. Debit transactions are immediate, while credit ones may take a few days to process.

Credit Cards

Credit cards can help you build credit, since they’re loans that have to be approved by lenders. Your balance and activity are reported to the credit bureaus. This builds your credit history, which is a significant factor in calculating your credit score. They can also hurt your credit if you don’t make your payments on time or carry too high a balance.

So, Which Card Should You Use?

Understanding how different types of cards work is key to determining which one best fits your financial situation. It all depends on the scenario and how you manage your finances.

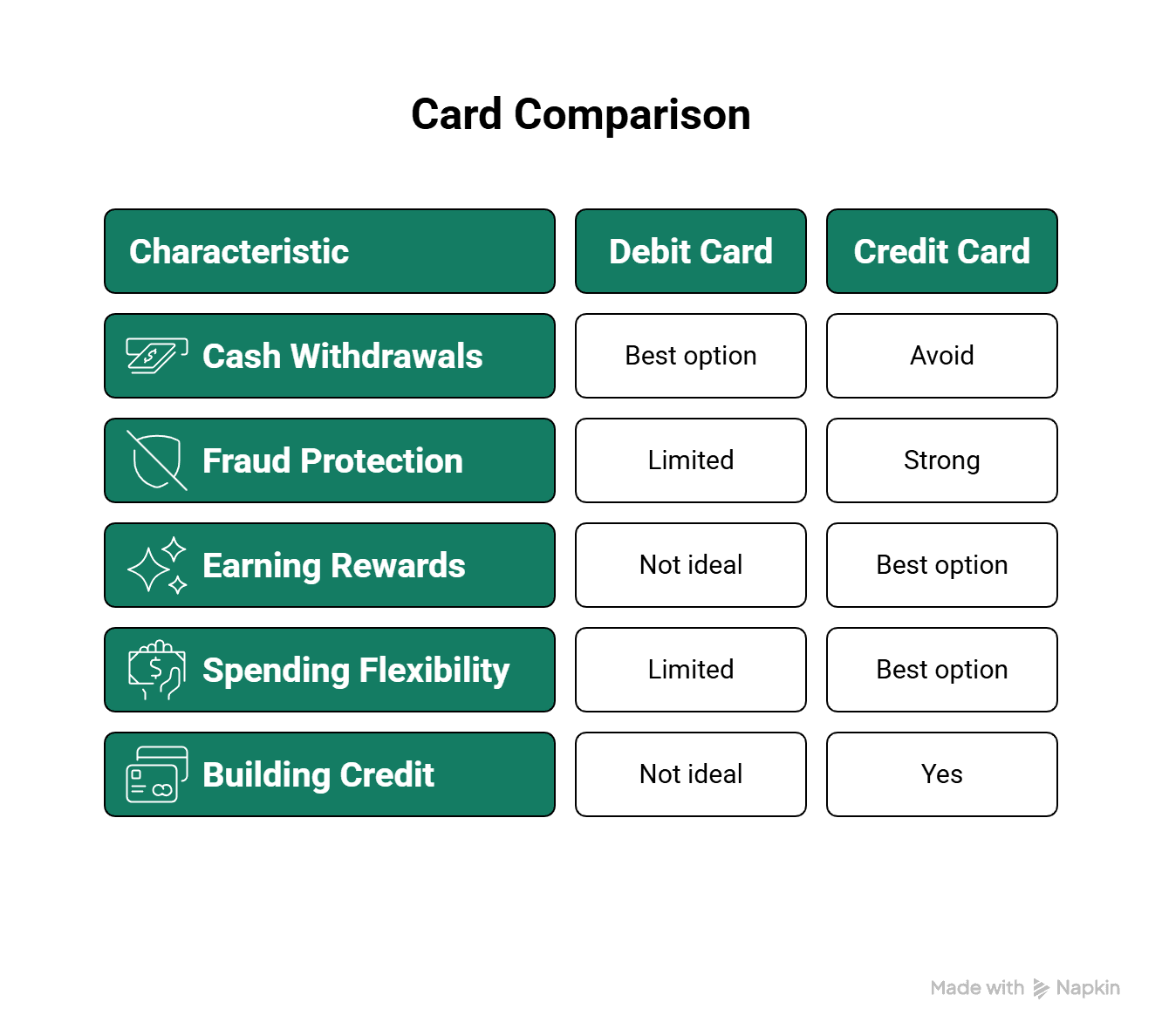

For Cash Withdrawals

If you want to get cash from the ATM or cash back at the register, use a debit card. Using your credit card for cash advances can lead to high fees, higher interest rates, and difficulty repaying your balance. Typically, cash advances carry a much higher interest rate compared to regular purchases. It’s essential to avoid this option to avoid these negative consequences.

For Fraud Protection

Because of strong fraud protection on credit cards, many consumers choose to use them for all purchases, even everyday items like groceries and gas. They then pay it off in full each month. That way, they earn rewards and have the peace of mind of knowing they won't be liable if fraudulent charges occur.

For Earning Rewards

If you’re looking to earn rewards, a credit card is often the best option. Debit cards typically don’t offer rewards like cash back or points, which makes credit cards more attractive for people who want to earn rewards on their spending.

For Debt Conscious

If you're trying to avoid racking up debt or pay down existing credit card debt, stick to using your debit card.

For Spending Flexibility

If you need a little flexibility with your spending, a credit card is your best option. Debit cards are limited to the amount in your checking account, but with a credit card, you can make purchases now and pay later.

For Building Credit

If you’re trying to build credit, using a credit card rather than a debit card will help, since credit cards are reported to the credit bureaus and debit cards are not. Using credit cards responsibly can improve your credit score over time.

Regardless of the card you use, tracking your purchases is essential to avoid overspending and spotting fraudulent charges quickly.

Also read:

Ultimate Guide to FAFSA and Student Loans: Making sense of it all

Where Do I Start? How to Build Credit if You Don’t Have a Credit Score

Choosing The Right Card Based On Your Spending Habits

Picking the right card is key to managing your money the smart way.

Credit cards let you borrow money and help build your credit score.

Debit cards only let you spend what you have in your bank account, no debt, no interest.

What is a debit card? It's a simple way to pay for things like groceries or bills, directly from your checking account. It’s perfect for staying within your budget.

So, which one should you use?

Credit card: Great if you want to build credit and need a little flexibility with payments.

Debit card: Ideal if you want to avoid debt and stick to a budget.

At Arro, we believe building credit should be simple and accessible. That’s why we created a credit card that helps you learn, grow, and earn, all in one app. With no hard credit checks, no deposit, and 1% cashback on gas and groceries, you can start improving your credit while earning rewards. Plus, with Artie, your AI Money Coach, you’ll get 24/7 guidance to make smarter financial moves and unlock higher credit limits as you go.

Every on-time payment and lesson helps you unlock higher credit limits and better credit health. Thousands are already building stronger credit with Arro.

Ready to start your own journey?

Download the Arro app today and see how easy it can be to build credit with confidence.

FAQs

How can I improve my credit score using Arro?

Arro provides a variety of tools to help you improve your credit score. By making on-time payments, completing educational lessons, and following personalized tips from your AI Money Coach, Artie, you can track and boost your credit score over time. Plus, every milestone you achieve, like unlocking higher credit limits, helps strengthen your credit profile. Arro reports to all three major credit bureaus, so you get a score bump as you progress.

Can I apply for an Arro Card if I have no credit history?

Yes! Arro is designed to help those with little to no credit history start building their credit. With no hard credit checks required for approval and no deposit needed, Arro is one of the easiest ways to access credit and begin improving your financial future, even if you’re new to credit or starting over. And if you're wondering what a debit card is, Arro also gives you a simple way to manage everyday spending without worrying about building debt.

What happens if I miss a payment on my Arro Card?

If you miss a payment on your Arro card, you may incur a late fee, and it could negatively impact your credit health. However, Arro provides reminders and tips through Artie, your AI Money Coach, to help you stay on top of payments and avoid any fees. It's essential to make at least the minimum payment to prevent late fees and any potential damage to your credit score.

Can I use my Arro Card internationally?

Yes, you can use your Arro card internationally. However, it's essential to keep in mind that foreign transaction fees may apply when using the card outside the country. Arro accepts Visa or Mastercard worldwide, but it's always a good idea to check with your card issuer for any international fees or restrictions.

Are there any fees for using the Arro app or card?

Arro prides itself on transparency, so there are no annual fees or hidden charges. However, there may be fees for specific actions, such as late payments or cash advances. Arro aims to minimize these costs, making it a more straightforward way to build your credit without the usual surprises.