Table Of Content

Understanding Your Fresh Start After Bankruptcy

Month 1-3: Foundation Phase

Month 4-6: Building Momentum Phase

Month 7-9: Growth Phase

Month 10-12: Upgrade Phase, Level Up Your Credit

Mistakes That Slow Down Credit Recovery

Your Credit-Building Journey Starts Here

FAQs

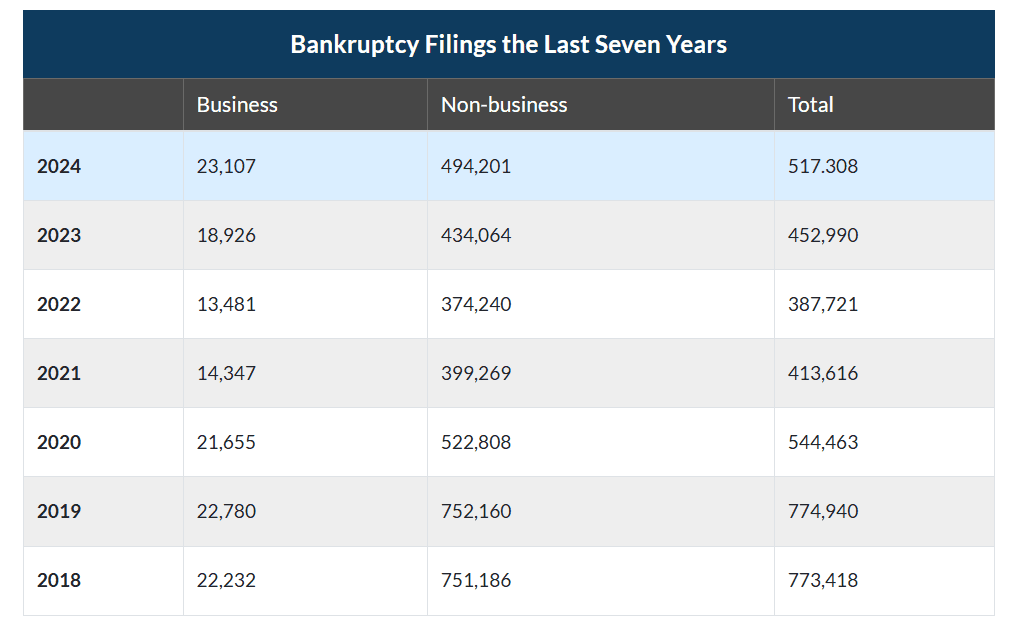

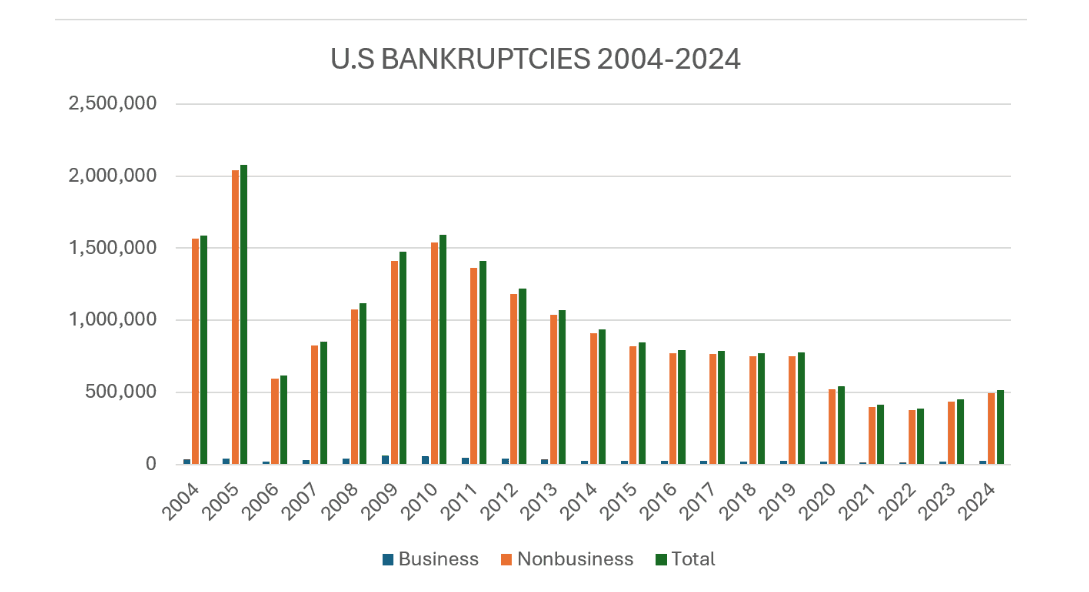

Rebuilding your credit after bankruptcy can feel overwhelming, especially when you’re also navigating a broader economic landscape where financial stress is rising. In the U.S., more than 517,000 bankruptcy cases were filed in 2024, showing that financial challenges remain widespread.

Despite this, data show that individuals who adopt consistent financial habits, like budgeting and disciplined saving, are more likely to improve their long‑term financial outcomes.

Source: Debt.org

In this article, we'll walk you through a 12‑month, bite‑sized plan to rebuild credit after bankruptcy step by step, with progress badges and smart guidance from Arro.

Key Takeaways

Bankruptcy gives you a fresh starting line to rebuild credit with clarity and purpose.

The first 12 months matter most; every positive move carries extra weight when starting fresh.

Focus on payment history (35%) and credit utilization (30%); they control two-thirds of your score.

Track progress weekly to achieve 40% better results than those who don't monitor consistently.

Understanding Your Fresh Start After Bankruptcy

When you file for bankruptcy, it provides a legal reset. But rebuilding your credit takes consistent action over time. In the U.S. alone, bankruptcy cases surpassed 500,000 in 2024, highlighting how common financial resets have become.

Source: Debt.org

While bankruptcy stays on your credit report for up to 7–10 years, most people see meaningful improvement much sooner when they begin to rebuild credit after bankruptcy with focused actions like monitoring reports, making on-time payments, and building positive credit accounts.

When bankruptcy clears your slate, something powerful happens that many don’t expect: your debt-to-income ratio improves overnight, making you a less risky borrower in the eyes of lenders. Additionally, your credit score often begins to rise within just a few months as the constant damage from late payments stops.

Think of bankruptcy as a reset button that stops the bleeding and allows healing to begin. With proven methods, you now have the opportunity to rebuild credit after bankruptcy and move forward without the burden of unmanageable debt holding you back.

Month 1-3: Foundation Phase

The first 90 days after bankruptcy set the tone for everything that follows. This is when you establish systems that remove friction and build habits that stick.

Check Your Credit Reports For Errors

Start by pulling your free reports from AnnualCreditReport.com. Look specifically for discharged debts that should show "included in bankruptcy" with $0 balances. Creditors mess this up more often than you'd think.

What to do:

Download reports from all three bureaus (Equifax, Experian, TransUnion)

Create a spreadsheet noting any accounts that look wrong

Dispute errors directly with bureaus and creditors online

Include your bankruptcy discharge papers as proof

Setting up a rotation to check one bureau every four months gives you year-round monitoring without paying for expensive services.

Set Up Free Credit Monitoring

Sign up for Credit Karma, Credit Sesame, or check if your bank offers free monitoring. These tools show which factors currently help or hurt your score in real-time.

The two factors to watch most closely when you rebuild credit after bankruptcy: payment history (35% of your score) and credit utilization (30% of your score). Together, these account for nearly two-thirds of your entire credit rating.

Open Your First Secured Credit Card

A secured card is your fastest path to a positive credit history. You put down a refundable deposit (typically $200-$500) that becomes your credit limit.

Top secured card features to look for:

No annual fee

Reports to all three credit bureaus (this is critical!)

Opportunity to graduate to unsecured after 6-12 months

Mobile app for easy payment tracking

Use your secured card for one small recurring purchase each month, like a streaming subscription or gas fill-up, then pay it off completely. This creates consistent positive reporting without risk.

Build Your Emergency Mini-Fund

Start with just $500. This small cushion prevents you from reaching for credit when unexpected expenses arise, protecting your rebuilding progress.

🎖️ Progress Badge Earned: Foundation Builder

You've set up monitoring, opened your first credit account, and created a safety net. Your rebuild has officially begun!

Month 4-6: Building Momentum Phase

You've proven you can manage a single credit account responsibly. Now it's time to strategically layer in additional positive data points.

Maintain Perfect Payment History

By month 4, you should have made three consecutive on-time payments. This is huge! Payment history makes up 35% of your credit score, so every single month you add to that streak matters.

Set up autopay for at least the minimum payment as a safety net

Schedule calendar reminders 5 days before due dates

Make payments even earlier when possible; there's no penalty for paying early

Your perfect payment streak is the foundation of everything else you'll build.

Keep Credit Utilization Under 10%

Here's a game-changer most people miss: credit scoring models check your balance on the statement closing date, not when you actually pay. So even if you pay in full every month (which you should!), a high balance at statement close hurts your score.

Make mid-cycle payments to keep your reported balance low. If your $500 secured card typically shows $200 at statement close, that's 40% utilization. Pay it down to under $50 before the statement cut, and you're suddenly at optimal 10% utilization.

Become An Authorized User (If Possible)

Getting added as an authorized user on someone else's established credit card can instantly add years of positive history to your report. The ideal account would be 5+ years old with perfect payment history and low utilization.

Important requirements:

Choose someone financially responsible who always pays on time

Verify their card issuer reports authorized users (Capital One, Chase, and American Express all do)

You don't need actual access to the card to benefit

Their account history typically appears on your report within 30-60 days

This single move can add significant points to your score when you rebuild credit after bankruptcy.

Consider A Second Secured Card (Optional)

If you've maintained a perfect payment history on your first card, adding a second secured card from a different issuer shows you can manage multiple accounts. Wait until month 6 to minimize hard inquiries.

🎖️ Progress Badge Earned: Momentum Master

Three months of perfect payments, low utilization, and strategic account additions. You're building serious credit muscle!

Month 7-9: Growth Phase

The middle months are where you start seeing real score improvements. Your positive payment history is lengthening, your utilization is under control, and you've established a rhythm.

Request Credit Limit Increases

Every 6 months, request a credit limit increase for your existing accounts. Higher limits improve your utilization ratio without changing your spending, which boosts your score.

Most secured card issuers allow online requests. Some will grant increases without a hard credit pull, especially if you've been a model customer. Even a $200 increase on a $500 card drops your utilization from 20% to 14% if you're carrying a $100 balance.

Explore Credit Builder Loans

Credit builder loans are a unique product designed specifically for people rebuilding credit. You make monthly payments toward a "loan," but you only receive the money after completing all payments. The lender holds your funds in a savings account while you pay.

Benefits of credit builder loans:

Adds installment loan diversity to your credit mix (10% of your score)

Creates forced savings while building credit simultaneously

Typically have low monthly payments ($25-$75)

Reports to all three bureaus monthly

Local credit unions commonly offer these products. When combined with your secured cards, you're now demonstrating to lenders that you can manage both revolving and installment credit responsibly.

Check For Secured Card Graduation

Many secured card issuers automatically review accounts for graduation to unsecured status after 6-12 months. But some require you to request it.

Call your card issuer to confirm graduation eligibility. If approved, you'll receive a refund of your deposit and may be granted a higher credit limit. Your account stays open with the same history, so there's no downside to asking.

Monitor Your Credit Score Trends

By month 9, you should see measurable improvement in your scores. Most people who consistently follow these strategies see a 30-60-point increase by this phase.

🎖️ Progress Badge Earned: Growth Champion

You've optimized your accounts, diversified your credit mix, and your score is visibly climbing. This is where it gets exciting!

Month 10-12: Upgrade Phase, Level Up Your Credit

The final quarter of your first year is about capitalizing on all the progress you've made and positioning yourself for even better opportunities ahead.

Consider Entry-Level Unsecured Cards

Once your score reaches 600-650 (which many people hit by month 10-12), entry-level unsecured credit cards become realistic options. These cards often include rewards, higher limits, and better terms than secured cards.

Cards that commonly approve rebuilders include:

Capital One Platinum (no rewards but no annual fee)

Discover it Secured (graduates to unsecured with cashback rewards)

Credit One cards (watch for annual fees, but they report to all bureaus)

Apply strategically, no more than one new application every 6 months, to avoid too many hard inquiries clustering together.

Maintain Your Oldest Accounts

Even after qualifying for better cards, keep your first secured card open and active with a small recurring charge. The age of your oldest account accounts for 15% of your credit score, and closing it would reset that clock.

Make one small purchase on your original secured card every few months to keep it active. Your credit history length is an asset that only grows with time.

Review Your Full Credit Journey

Pull your credit reports again and compare them to where you started 12 months ago. Document your wins, discharged debts properly marked, on-time payment streaks, improved utilization ratios, and that rising score.

Research shows that people who review their goals quarterly are 31% more likely to achieve them at Mooncamp than those who don't track progress. Your year-end review isn't just satisfying, it's strategic.

Set Your Next 12-Month Goals

Now that you've proven you can rebuild credit after bankruptcy successfully, what's next? Maybe it's qualifying for an auto loan, reaching a 700 credit score, or being approved for a premium rewards card.

Write down specific targets. People who write goals down are significantly more likely to achieve them than those who keep goals vague or only think about them.

🎖️ Progress Badge Earned: Year One Graduate

You did it! Twelve months of consistent effort have transformed your credit profile. You've built habits that will serve you for life.

Mistakes That Slow Down Credit Recovery

Even with a solid plan, certain mistakes can stall your progress or even undo months of hard work. Here's what to avoid as you rebuild credit after bankruptcy.

Falling Back Into Old Spending Habits

The biggest reason people struggle to rebuild credit after bankruptcy isn't lack of knowledge; it's repeating the financial behaviors that created problems in the first place.

View credit cards as rebuilding tools, not spending tools. Use them for small, planned purchases you can immediately pay off. A recurring subscription or one tank of gas monthly is perfect. Anything beyond that requires careful budgeting.

Making Only Minimum Payments

One dangerous myth: carrying a balance improves your credit score. This is completely false. Making only minimum payments keeps you in debt longer and costs thousands in interest without any score benefit.

Example of a minimum payment trap:

$3,000 balance at 22% APR

Minimum payment only: 12+ years to pay off, $4,200+ in interest

Paying $150/month instead: 27 months to freedom, $1,050 in interest

Always pay your full statement balance every month. If you can't pay in full, you're overspending on the card.

Applying For Too Many Cards At Once

Each credit application creates a hard inquiry, which temporarily lowers your score and remains on your report for 2 years. Multiple inquiries within a short period signal risk to lenders and increase the likelihood that future applications will be denied.

Stick to one new account every 6 months maximum. This measured approach builds your credit profile without triggering red flags.

Ignoring Your Credit Reports

Many people review their reports once after bankruptcy, then avoid reviewing them again for years. This emotional avoidance prevents you from tracking progress and catching errors early.

Set up a simple rotation: check Experian in January, TransUnion in May, Equifax in September. Three free reports per year, perfectly spaced. Most credit rebuilding problems start small and grow through neglect.

Falling For Credit Repair Scams

Companies promising to "erase bankruptcy" or remove negative information overnight are almost always scams. Legitimate credit repair takes time and consistent effort; there are no shortcuts.

Red flags of credit repair scams:

Upfront fees before any service

Promises to remove accurate information

Claims about "new credit identity" tactics

Pressure to dispute everything regardless of accuracy

No written contract explaining your rights

Save your money. Everything these companies do, you can do yourself for free by disputing legitimate errors directly with the credit bureaus and building positive payment history.

Also Read:

Your Must-Read Guide to Understanding a Negative Balance on Your Credit Card

How to Build Credit: Your Complete Guide to Building Credit from Scratch

Your Credit-Building Journey Starts Here

Rebuilding credit after bankruptcy isn't about perfection; it's about persistence, smart habits, and having the right support system in place. You've learned the 12-month roadmap, the mistakes to avoid, and the strategies that actually move your score upward. Now it's time to put this knowledge into action.

The most successful credit rebuilders share one thing in common: they track their progress consistently and celebrate small wins along the way. Every on-time payment, every point your score climbs, every month of low utilization, these aren't just numbers; they're proof that you're building something better.

Why Choose Arro?

At Arro, we believe building credit shouldn't be confusing, expensive, or out of reach. That's why we've crafted a credit card that supports you in learning, earning, and developing, all seamlessly integrated within a single app.

With no hard credit checks, no deposit, and 1% cashback on gas and groceries, Arro makes it simple to start improving your credit while rewarding your everyday spending. You'll also get access to Artie, your personal AI Money Coach, who's there 24/7 to answer questions, celebrate wins, and help you make smart financial moves.

Every on-time payment, every lesson completed, every small step forward helps you unlock higher credit limits and better credit health. Thousands of people are already building stronger credit with Arro, and having fun doing it.

Ready to rebuild credit after bankruptcy with confidence? Download the Arro app today and see how easy it can be when you have the right tools and support in your corner. Your fresh start is waiting.

FAQs

Will bankruptcy affect my ability to rent an apartment or get a job?

Landlords often review credit reports, and bankruptcy will appear on them. However, many landlords place greater emphasis on rental history and income verification. Be prepared to explain your situation and provide references. Most employers cannot check your credit unless the position involves financial responsibilities, and even then, bankruptcy alone rarely disqualifies candidates in states where it's legal to check.

What credit score do I need to buy a house after bankruptcy?

FHA loans may be available 2 years after a Chapter 7 bankruptcy discharge or 1 year after a Chapter 13 (with court approval). Most FHA lenders require a minimum credit score of 580, though a score of 620+ can get you better rates. Conventional mortgages typically require 4 years to have passed since bankruptcy and a score of 620 or higher. Focus on rebuilding to at least 650 for decent rates and options.

Does paying off collections help rebuild credit after bankruptcy?

If the collection accounts were included in your bankruptcy discharge, they should already show $0 balances. Paying them won't improve your score since they're already settled. However, if you have post-bankruptcy collections, yes, paying them helps. For pre-bankruptcy collections properly marked as discharged, focus on building a new positive payment history instead.

How much will my credit score drop after filing for bankruptcy?

The score drop varies based on your credit profile before filing. People with higher pre-bankruptcy scores (680+) typically see larger drops (150-240 points), while those with already damaged credit from missed payments may see smaller drops (80-150 points). The key is that active rebuilding can improve scores within months, regardless of the starting point.