Table Of Content

The Money In Your Pocket: Cash & Debit

Reward & Risk: Credit Cards

Buy Now, Pay Later? A Good Option, But Proceed With Caution

Personal Finance Is PERSONAL

Choosing Your Best Payment Path

FAQs

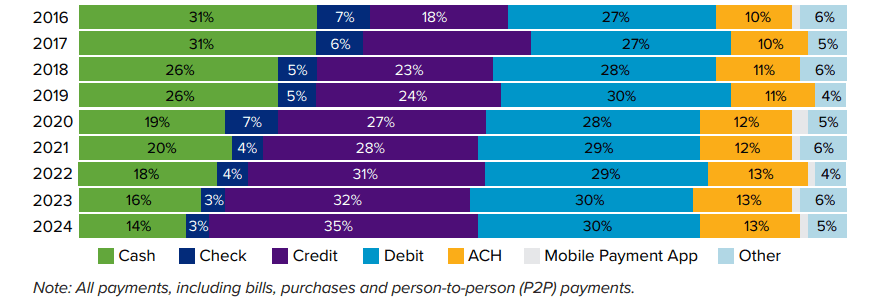

You probably don't spend as much time thinking about how you spend your money as you do actually spending it. Or maybe you have found yourself in freeze mode before you click the "pay now" button. With more ways to pay than ever before, cash, debit cards, credit cards, buy now pay later, the trick is understanding which payment method works best for you.

In fact, U.S. consumers made an average of 48 payments per month in 2024, with credit cards making up 35% of all transactions.

Source: The Federal Reserve Financial Services

A survey by FinTech Strategy found that 52% of consumers are more likely to impulse purchase with card payments, highlighting how our payment choices directly impact our spending behavior.

In this article, we'll explore the pros and cons of different ways to pay so you can make smarter choices that align with your financial goals.

Key Takeaways

Cash and debit cards help manage budgets without risk of overspending.

Credit cards build credit and offer rewards when used responsibly.

Buy now, pay later works for essential purchases but requires careful management.

Choose ways to pay based on your priorities: rewards, credit building, or budget control.

The Money In Your Pocket: Cash & Debit

For convenience (and your budget's sake), use your most liquid payment methods: cash and debit cards. Given these are your readily available funds and, most importantly, finite, you can conveniently spend the dough without the risk of overspending. This is a significant perk if you're trying to build your savings, learn to budget, or avoid credit card debt.

Research supports the psychological power of cash. Studies on Spendception show that digital payments reduce the psychological visibility of spending, making it easier to overspend without realizing it. When you're exploring different ways to pay, cash creates what researchers call the pain of paying, a natural brake on impulse purchases.

Debit cards can be an excellent tool for managing your budget because transactions appear on your account in real time and are categorized, making it easy to monitor where your money is going. That means time and money in your pocket! The quick swipe of a plastic card can make us feel like we're not really spending money, making it easy to spend more than we would when handing over our hard-earned cash.

When deciding between different ways to pay for everyday expenses, consider:

Cash keeps spending tangible and helps you stick to the limits you've set

Debit cards offer convenience while pulling directly from your available funds

Real-time tracking with debit makes budgeting easier than paper receipts

These payment methods work exceptionally well when you want the assurance that you're only spending money you actually have.

Reward & Risk: Credit Cards

By swiping your card, you'll have the opportunity to build credit in the long run. If you already have credit but need to boost your credit score, credit cards are the best way to do so, as long as you pay on time. Having a consistent, on-time payment history boosts your credit score, which can give you the power to buy and rent housing, qualify for loans, secure insurance, and more.

Depending on the type of card you have, you can earn easy rewards on simple, everyday purchases. Get back up to 5% cash back on every dollar you spend, earn points, and other rewards. Some cards even allow you to choose specific categories to earn rewards on, such as groceries, restaurants, and gas, talk about value!

Like debit cards, credit cards are useful for tracking your spending. Track your spending by category via your online account. Spending too much on those iced coffees? Now you know!

Credit Cards Shine For Larger Purchases

If you're considering paying in cash for a large purchase but don't have the funds immediately available, credit can bridge the gap. Let's not forget that credit cards can come in handy for those larger purchases that you need but don't have sufficient funds to cover right away. Just be sure you pay off your bill every month to avoid interest and keep increasing your credit score. Borrowing money on a credit card isn't a good substitute for careful saving or planning, but it's a useful backup plan for large, essential, unexpected purchases you can't pay off immediately.

Psychology Matters When Choosing Ways To Pay

Another word of caution: psychology shows that using a credit card instead of cash can lead to overspending because we're less aware of what we're spending. This is why it's always necessary to be extra attentive to following a spending plan, staying on top of payments, and asking ourselves, "Is this purchase necessary?" while swiping.

Credit cards work best when you:

Pay your full balance every month to avoid interest charges

Use them strategically for categories that earn the best rewards

Monitor your spending regularly through your online account

Treat your credit limit as a tool, not extra money to spend

Among the many ways to pay available today, credit cards remain one of the most powerful for building your financial future, when used responsibly.

Buy Now, Pay Later? A Good Option, But Proceed With Caution

Buy Now Pay Later (BNPL) is the button you see at online checkout when you're about to make an $80 purchase, prompting you to pay in 4 installments of $20 each. Seems too good to be true and makes me think I might add those sneakers back to my online shopping cart after all.

According to PYMNTS Intelligence, nearly 50% of Generation Z and millennial consumers have used BNPL in the past 12 months as of June 2024, making it one of the fastest-growing payment methods in the current market.

There are many factors to consider when choosing a BNPL payment plan, but one of the most important is: "Is this purchase necessary?" BNPL is a great option when you are in a pinch and don't have the funds needed to purchase an essential item. They offer zero- to low-interest options, with no credit score requirement (for now).

However, just like credit cards, you are still taking on debt when you use BNPL at checkout, and BNPL installments are often higher than credit card minimum payments, so be sure that you pay off your balance to avoid costly late fees or damaging your credit score.

Before choosing BNPL from your available ways to pay, ask yourself:

Is this purchase truly essential, or am I being tempted by the easy installment option?

Can I afford all four installment payments on time without stretching my budget?

Have I compared this to using a rewards credit card that I'd pay off in full?

BNPL can be an innovative tool when used thoughtfully, but it's essential to recognize it's still debt that requires careful management.

Personal Finance Is PERSONAL

As we always say, personal finances are just that, personal. By considering what is most important to you, rewards, building credit, and sticking to a budget, you can feel confident when you choose the payment method that will work best for you and your financial goals.

When evaluating payment methods, remember that nearly 80% of U.S. consumers carry cash as a backup, showing that even in our digital age, having multipleoptions gives you flexibility and control. The best approach often involves using different payment methods for different situations: cash for small daily purchases to control spending, debit cards for regular bills and groceries, and credit cards strategically for rewards and credit-building.

If you need a support system along the way, join us at Arro. We will give you the financial confidence and control you are looking for.

Choosing Your Best Payment Path

With more ways to pay than ever before, finding the right payment strategy isn't about choosing just one method. It's about understanding how each option works with your spending style and financial goals.

Throughout this guide, we've explored how cash keeps spending real, debit cards offer convenience with built-in limits, credit cards build your financial future while earning rewards, and buy now pay later provides flexibility for essential purchases. With Americans making an average of 48 payments per month, mastering your payment mix isn't just smart; it's essential.

The reality? Most successful budgeters use a combination of these payment methods, strategically matching each to different spending categories. They use cash for where they tend to overspend, debit cards for everyday bills, and credit cards for rewards on regular expenses they'd buy anyway.

Also read:

Balance Transfer or Personal Loan: What is the Right Fit for You?

Your Must-Read Guide to Understanding a Negative Balance on Your Credit Card

At Arro, building credit shouldn't be confusing, expensive, or out of reach. That's why we've created a credit card designed to support you in learning, earning, and growing, all in one app.

With no hard credit checks, no deposit required, and 1% cashback on gas and groceries, Arro makes it easy to start improving your credit while getting rewarded for everyday spending. You'll also have access to Artie, your personal AI Money Coach, available 24/7 to answer questions, celebrate your wins, and help you make confident financial decisions.

Every on-time payment, every lesson completed, every small step forward unlocks higher credit limits and better credit health. Thousands of people are already building stronger credit with Arro while actually enjoying the journey.

Ready to find your best way to pay while building the credit score you deserve? Discover how simple building credit can be with the right partner by your side.

FAQs

How can I identify which payment method is costing me the most?

Track all your purchases for one month using each payment method separately. Calculate impulse buys made with each. Research shows that card purchases lead to 12-18% higher spending than cash purchases. Look at fees too: overdraft charges on debit cards, interest on credit cards, or late fees from BNPL. The method with the highest total of unnecessary purchases and fees is the most costly, even if it offers rewards.

What's the psychological reason people overspend more with specific payment methods?

Digital payments create what researchers call "payment decoupling, separating the pleasure of purchasing from the pain of payment. Cash provides immediate tactile feedback, making your brain register the loss. Cards and digital payments lack this physical reminder, reducing mental friction around spending. This psychological detachment explains why the same person making identical purchases will spend less when paying with cash than with any other payment method.

Should I avoid credit cards if I'm trying to build better spending habits?

Not necessarily, eliminating credit cards could hurt your credit score and forfeit valuable rewards. Instead, use strategic limits: designate one card for recurring bills you'd pay anyway (such as utilities or subscriptions), then set up automatic full payments. Remove the card from your wallet and delete it from online shopping sites. This approach builds credit history while reducing the temptation to use impulsively.

How do BNPL services affect my credit differently from credit cards?

Currently, most BNPL services only report harmful activity (missed payments) to credit bureaus, not positive payment history. Credit cards report both, meaning on-time credit card payments actively build your score, while BNPL doesn't. However, BNPL missed payments damage your credit just as much. Some newer BNPL providers are starting to report positive payment histories; check your specific provider's reporting policies before assuming it will help your credit.

What's a practical way to transition from overspending with cards to better control?

Try the "reverse budget" approach: Keep one credit card for emergencies only and switch to a debit card for two weeks. Track what you don't buy during this period, items you would've purchased with credit but skipped with debit. After two weeks, identify your trigger spending categories (e.g., dining out, online shopping). For those categories, commit to paying with cash or debit cards, while using credit cards responsibly for planned purchases in other areas.