Table of Content

What Are Charge-Offs And Collections?

The Complete Timeline: Month By Month

How Do Collections Credit Impacts Your Credit Report

When Status Changes Actually Appear

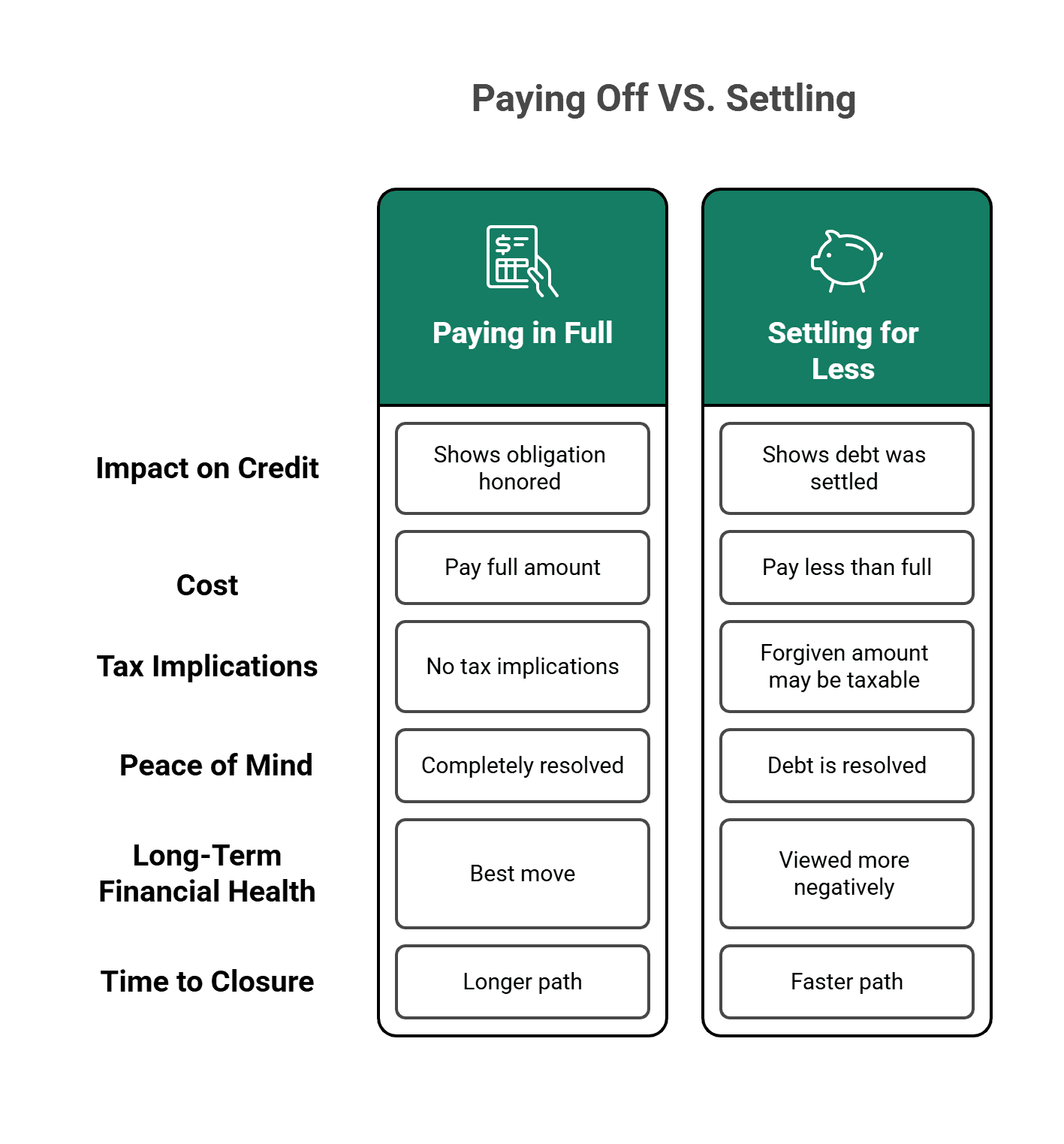

Paying Off VS. Settling: What's The Difference?

How Long Collections Stay On Your Credit Report

Take Control Of Your Credit Journey

FAQs

When you're dealing with debt that's gone to collections, the uncertainty can feel overwhelming.

According to the New York Fed's 2025 Household Debt and Credit Report, 4.7% of consumers currently have a third-party collection account on their credit report; that's millions of people navigating this challenging situation.

Source: New York Fed

The stress isn't just financial, either. Research shows that people with debt are three times as likely to experience depression, anxiety, and stress compared to those without debt.

Here's the good news: understanding the timeline of what happens when, from charge-offs to collections to settlements, puts you back in control. In this article, we'll break down exactly when changes happen to your collections credit accounts, what you can expect month by month, and how to navigate the process with confidence.

Key Takeaways

Charge-offs occur after about six months of missed payments, marking the debt as a loss for creditors.

Collections accounts stay on your credit report for seven years from the original delinquency date.

Paid collections are excluded from newer scoring models (FICO 9/10, VantageScore 3.0/4.0) but still affect older models (FICO 8).

Settling debt for less than owed is better than ignoring it, but it may have tax implications.

Collections can have significant psychological effects, so it's important to address them promptly.

Changes to your credit report may take 1-2 months after paying off or settling a debt.

What Are Charge-Offs And Collections?

Let's start with the basics. When you stop making payments on a debt, two things can happen: the account is charged off and sent to collections, or both.

A Charge-Off

Happens when your creditor decides the debt probably won't be collected. Usually, after about six months of missed payments, creditors "charge off" the account for accounting purposes. This doesn't mean you no longer owe the money; it simply means the creditor is writing it off as a loss. Think of it as the creditor waving a white flag, but the debt is still very much yours.

Collections

On the other hand, it is the active process of trying to recover that debt. Your original creditor might use an in-house collections department, or they might sell or transfer your account to a third-party debt collector. Either way, collections credit entries on your report signal to future lenders that you've had trouble paying back what you borrowed.

Here's where it gets confusing: an account can be charged off and sent to collections. You might see both notations on your credit report at the same time: the original account marked as "charged-off" and a new collections account from the debt buyer.

Understanding these terms is your first step toward improving your financial health.

The Complete Timeline: Month By Month

So what actually happens, and when? Here's a realistic month-by-month breakdown of the collections credit process:

Months 1-2: The Grace Period Ends

Miss your first payment, and you're typically considered "past due" after 30 days. Most creditors report this to credit bureaus, and your credit score takes a hit. By day 60, if you still haven't caught up, the damage deepens, and your account is now seriously delinquent.

Month 3-5: Internal Collections Kicks In

Between 90 and 150 days past due, many creditors move the account to their internal collections department or begin more aggressive collection efforts. You'll likely get more frequent calls and letters. At this stage, the account hasn't been charged off yet, so you're still dealing with the original creditor.

Month 6: The Charge-Off

Around the 180-day mark (about six months), creditors typically charge off the account. This is when it officially becomes a loss on their books. The charge-off notation hits your credit report, and if the account hasn't already gone to collections, it usually does now.

Your credit report shows: "Charged-off" status on the original account

What you owe: The full balance plus any accumulated interest and fees

What happens next: The debt may be sold to a collection agency

This six-month milestone is critical, as it's when your collections credit situation becomes official on your credit history.

Months 7-12: Collections Takes Over

After the charge-off, your debt is either handled by the original creditor's collection department or sold to a third-party debt buyer. If it's sold, a new collection account appears on your credit report. The original account remains visible but shows as "transferred" or "closed."

During this period, debt collectors will contact you regularly. They're required to follow the Fair Debt Collection Practices Act, which means they can't harass you or use deceptive practices, but they will be persistent.

Month 13 And Beyond: The Long Haul

If you don't pay or settle the debt, it can sit in collections for years. Different collectors might buy and resell your debt multiple times, but each time it changes hands, the original delinquency date should stay the same. This date determines when the collection's credit entry will be removed from your report.

Understanding this timeline shows that, while the situation is serious, it's also predictable, which means you can plan your next moves strategically.

How Collections Credit Impacts Your Credit Report

Collection accounts significantly damage your credit score. The amount of damage depends on several factors: your overall credit profile, the number of collections, and the scoring model used.

Here's what you need to know about the credit impact:

Both the original account and the collection account can appear simultaneously. Your credit report may show the original credit card or loan (now closed or transferred) and the new collection account. Both carry negative information, though they shouldn't be counted twice against you in scoring calculations.

The collection stays for seven years from the original delinquency date. That's the date of your first missed payment that led to collections, not the date the account was charged off or sent to collections. Even if your debt gets sold to multiple collectors, that original date doesn't change.

Newer scoring models treat paid collections differently. Research shows that the latest FICO® Score versions (9 and 10) and VantageScore versions (3.0 and 4.0) exclude paid collections from their calculations entirely. That means paying off a collection could immediately improve your score if lenders use these newer models. However, FICO® Score 8, still the most widely used version, only ignores collections under $100.

The psychological toll is real. Beyond the impact on credit scores, dealing with collection issues takes an emotional toll. Among adults with anxiety and medical debt, nearly 40% delayed needed care because of their financial situation. The stress creates a cycle that's hard to break.

The key takeaway: collections hurt your credit, but the damage isn't permanent, and you have options for recovery.

When Status Changes Actually Appear

Let's talk about timing, specifically, how long it takes for changes to show up on your credit report after you take action.

After You Pay Off A Collection

You've finally paid off that collection account. Congrats! But don't expect your credit report to update overnight. Here's the realistic timeline:

1-2 months for the status to update. The collection agency needs to process your payment, update their records, and then report the change to the three major credit bureaus (Equifax, Experian, and TransUnion). Most agencies report monthly, so depending on when in their reporting cycle you pay, it may take 30 to 60 days for your credit report to reflect "paid in full."

Check for accuracy after 60 days. If two months have passed and your collection's credit account still shows as unpaid, contact the collection agency. Get proof of payment and follow up. Reporting errors happen, and you have the right to dispute inaccurate information.

After You Settle A Debt

Settlement is when you negotiate to pay less than the full amount owed. Collectors agree to this because getting something is better than getting nothing.

The account updates to "settled" or "paid settled." This is better than "unpaid," but not as good as "paid in full." Some lenders view settlements negatively because you didn't pay back everything you borrowed.

The timeline is similar: 1-2 months. Just like with paying in full, expect 30 to 60 days for the change to appear on your credit reports.

After You Request Goodwill Deletion

A goodwill deletion is when you ask the creditor or collector to remove the collection account from your credit report entirely, even though you legally owe (or owed) the money. There's no law requiring them to do this, and most won't, but it's worth a shot if:

You had a temporary hardship (medical emergency, job loss)

You've since demonstrated responsible credit behavior

You have a previously strong payment history with that creditor

If they agree (which is rare but possible), removal could happen within 30 days after their decision. Get any agreement in writing before you pay.

Patience is key when dealing with collection credit reporting timelines.

Paying Off VS. Settling: What's The Difference?

When you're facing a collection account, you have options. Let's break down the two main paths:

Important statute-of-limitations note: Be careful about making payments on very old debts. In some states, making a payment can reset the statute of limitations, the time period during which a collector can sue you. Once that clock resets, they have more time to take legal action.

Both options improve your situation compared to ignoring the debt, but which is better depends on your financial circumstances and long-term goals.

How Long Do Collections Stay On Your Credit Report

This is the question everyone wants answered: when will this finally disappear?

The magic number: seven years from the original delinquency date. That's the date you first missed a payment on the account that eventually went to collections. Let's say you stopped paying your credit card bill in March 2023. That account gets charged off in September 2023 and sold to a collector in October 2023. The seven-year clock started ticking in March 2023, meaning the collection should automatically fall off your credit report in March 2030.

This Applies Whether You Pay Or Not

A common misconception is that paying off a collection restarts the seven-year clock. It doesn't. The collection will drop off at the same time regardless of whether you pay it, settle it, or ignore it. However, unpaid collections can lead to lawsuits, wage garnishments, and ongoing stress, so paying is still usually the right move.

The Date Shouldn't Change When The Debt Is Sold

If your debt gets bought and resold by multiple collection agencies, each new collector should report the same original delinquency date. If a collector reports a more recent date (called "re-aging"), that's illegal. You can dispute it with the credit bureaus.

After Seven Years, Collection Credit Entries Must Be Removed

The Fair Credit Reporting Act requires credit bureaus to delete the collection automatically. You don't need to do anything; it should just disappear.

Understanding this timeline helps you see the light at the end of the tunnel, even if seven years seems like forever right now.

Also Read:

Credit Cards 101: Here’s What Happens if You Go Over Your Credit Limit

Balance Transfer or Personal Loan: What is the Right Fit for You?

Take Control Of Your Credit Journey

Dealing with collection credit issues can feel isolating, but you're not alone, and you're not stuck. Understanding the timeline and your options is the first step toward rebuilding your financial confidence. Whether your collection account is six months or six years old, taking action today will start you on the path to better credit health.

Remember, the seven-year clock is already ticking. The question is: what do you want your credit profile to look like along the way?

Why Choose Arro?

At Arro, building credit shouldn't be confusing, expensive, or out of reach. That's why we've created a credit card that supports you in learning, earning, and growing, all seamlessly integrated within a single app.

With no hard credit checks and no deposit required, Arro makes it simple to start improving your credit from wherever you are today. You'll earn 1% cashback on gas and groceries, turning your everyday spending into rewards while you build your credit score. Every purchase and every on-time payment counts toward your progress.

You'll also get access to Artie, your personal AI Money Coach, who's there 24/7 to answer questions, celebrate wins, and help you make smart financial moves. Got a question about how collections affect your credit? Artie's got you. When is that next credit line increase coming? Just ask. Wondering how to budget for groceries this week? Artie's on it, no judgment, just helpful guidance when you need it.

Every on-time payment, lesson, and small step brings you closer to better credit. Arro makes building credit feel like an exciting journey, not a chore. Thousands are already seeing real score increases and progress toward their financial goals.

Ready to start your own journey? See how easy it can be to build credit with confidence, support, and zero surprises.

FAQs

How long does it take for a paid collection to show on my credit report?

After you pay off a collections credit account, it typically takes one to two months for the status to update on your credit report. Collection agencies usually report to credit bureaus monthly, so timing depends on when in that cycle you make your payment. If the status hasn't updated after 60 days, contact the collection agency with proof of payment and follow up with the credit bureaus if necessary.

Does paying off a collection remove it from my credit report?

No, paying off a collection doesn't remove it from your credit report. The account will update to show "paid" or "paid in full" status, but it remains visible for seven years from the original delinquency date. However, with newer scoring models like FICO 9 and VantageScore 3.0, paid collections are excluded from credit score calculations, so paying off collection accounts can still improve your score.

Should I settle a collection or pay it in full?

This depends on your financial situation. Paying in full demonstrates to future lenders that you fulfilled your full obligation and may result in better treatment under newer scoring models. Settling for less saves money immediately but shows as "settled" rather than "paid in full," which some lenders view less favorably. Additionally, the forgiven amount in a settlement may be taxable income. If you can afford to pay in full, it's generally the better long-term choice for your collection credit recovery.

Will newer credit scoring models help me if I have paid collections?

Yes, newer models such as FICO Score 9 and 10, and VantageScore 3.0 and 4.0 exclude paid collections from their calculations. This means if you pay off a collection credit account and a lender uses one of these newer models, your score could improve immediately. However, FICO Score 8, still the most widely used version, only ignores collections if the original debt was under $100, so paid collections may still affect your score with many lenders.

Can I negotiate a pay-for-delete agreement with collectors?

While some collectors may agree to remove a collection account from your report in exchange for payment (called "pay-for-delete"), this practice is in a legal gray area, and many major collection agencies won't do it. The credit bureaus' reporting agreements discourage it. Instead, consider requesting a goodwill deletion after payment if you had a legitimate hardship, or focus on paying the debt to benefit from newer scoring models that ignore paid collections.

How do I know when my collection will be removed from my credit report?

Find the date of the first delinquency, the first missed payment that led to the account going to collections. Count forward seven years from that date. The collection's credit entry should automatically be removed from your credit report on that date. You can find this date on your credit report, often listed as "Date of First Delinquency" or similar terminology. If it's not automatically removed after seven years, dispute it with the credit bureaus.