Table of Content

Understanding Why International Students' Credit Matters

The Challenge: No Cosigner, No Credit History

No-Cosigner Student Loans: What You Need To Know

Credit Cards For International Students Without A Cosigner

Building International Students Credit: Step-By-Step Strategies

Common Mistakes To Avoid When Building Credit

Your Credit-Building Journey Starts Here

FAQs

Starting your academic journey in the United States is exciting, but navigating the American financial system can feel overwhelming. Building credit without a U.S. cosigner or any prior credit history can feel impossible, but it doesn't have to be.

According to the Institute of International Education, over 1 million international students enrolled in U.S. colleges in recent years, and most face the same challenge: how do you prove financial reliability in a country where you're just getting started? Without an established credit history, securing loans, renting apartments, or even getting a phone plan becomes unnecessarily complicated.

Building credit for international students without a cosigner is now easier thanks to innovative financial products for newcomers. In this article, we'll explore strategies to establish your U.S. credit: from no-cosigner student loans to credit-building cards, and take control of your financial history.

Key Takeaways

Building international students' credit without a cosigner is achievable with specialized products designed for newcomers to the U.S. financial system.

Payment history is your most powerful tool; making every payment on time builds the foundation of excellent credit.

Credit cards designed for international students eliminate traditional barriers such as deposits and hard credit checks while providing education and support.

Starting early during your student years gives you time to build a strong credit foundation before entering the workforce.

Regularly monitoring your progress keeps you informed, motivated, and able to catch problems before they become serious.

Understanding Why International Students' Credit Matters

Your credit score is a financial passport that opens doors throughout your time in the U.S. and beyond. For international students, credit building isn't just about getting approved for loans; it's about creating opportunities that shape your entire American experience.

A strong credit history helps you secure better loan rates, saving thousands of dollars. It makes apartment rentals easier without excessive deposits, helps you get approved for phone plans and utilities without prepayment, provides access to reward credit cards, and prepares you for post-graduation life in the U.S.

Financial inclusion, including access to credit, significantly impacts economic mobility and long-term financial success. Starting your credit journey early gives you a competitive advantage that extends far beyond your student years.

The Challenge: No Cosigner, No Credit History

Most traditional U.S. lenders require two things international students simply don't have: an established credit history and a U.S. citizen or permanent resident willing to cosign. This creates a frustrating cycle where you need credit to build credit, but getting that first approval feels impossible when no one will give you a chance.

What Is A Cosigner?

A cosigner is someone who legally agrees to repay your loan if you can't. They're typically U.S. citizens or permanent residents with good credit who have lived in the country for at least two years. For international students, finding someone who meets these criteria and is willing to take on this financial responsibility can be nearly impossible.

Why Traditional Lenders Require Cosigners

Lenders view international students as higher-risk borrowers for several specific reasons. You have no U.S. credit history to evaluate, which means they can't assess your past financial behavior. Your future in the country may be uncertain due to visa limitations, and you may not have substantial U.S.-based income to demonstrate repayment capacity.

Without a cosigner to share the risk, most traditional banks and credit card companies simply say no. The good news is that a growing number of specialized lenders and financial products now recognize that international students' creditworthiness can be measured in different ways, opening new pathways to financial independence.

No-Cosigner Student Loans: What You Need To Know

Despite the challenges, several specialized lenders now offer student loans to international students without requiring a U.S. cosigner. These loans represent a fundamental shift in how financial institutions evaluate risk, focusing on your future potential rather than your past financial history.

How No-Cosigner Loans Work

Instead of evaluating your credit score, these lenders assess your school's reputation and whether it's on their approved list of eligible institutions. They examine your program of study and projected post-graduation earnings based on industry data. Your academic performance, likelihood of degree completion, country of origin, visa status, and proximity to graduation all factor into their decision. You need to be within 2 years of completing your degree.

This approach recognizes that international students' creditworthiness can be assessed based on academic achievement and career potential, rather than credit history alone. It's a more holistic view that considers who you're becoming, not just where you've been.

What To Look For In No-Cosigner Loan Options

When exploring no-cosigner student loans, research lenders that specialize in international student financing and verify whether your school is on their approved institution list. Compare fixed versus variable interest rates carefully, as this significantly impacts your total repayment amount. Understanding repayment terms is crucial. Some lenders allow you to defer payments until after graduation, while others require interest-only payments during school.

Look into the total loan amounts available and whether they'll cover your full Cost of Attendance as calculated by your school. Check the application timeline and disbursement process, since these loans typically take 6 to 8 weeks to process and fund. Consider whether the lender offers additional resources, such as career support or financial education, beyond just providing funds.

Typical Requirements For No-Cosigner Loans

Most no-cosigner loan programs require enrollment at an approved institution with a valid student visa, such as an F-1 or J-1. You'll need at least half-time enrollment in a degree program and must be within 2 years of graduation. Proof of identity and academic records are standard requirements, and you'll need to demonstrate U.S. residency during your studies.

Keep in mind that interest rates on no-cosigner loans are often higher than those on traditional student loans, typically ranging from 11% to 14%, because lenders assume greater risk. However, for many international students, having access to funding without a cosigner makes this trade-off worthwhile.

Credit Cards For International Students Without A Cosigner

While student loans help fund your education, a credit card is often the fastest and most effective way to start building your credit as an international student. The challenge? Most require either a cosigner or an established credit history, creating the same barrier you're trying to overcome.

The Traditional Secured Card Route

Secured credit cards have long been the go-to option for building credit from scratch. You provide a cash deposit, typically $200 to $500, which serves as your credit limit and collateral. While these cards are useful for credit-building, they have significant drawbacks for international students who need every dollar for living expenses.

Your money is tied up as collateral when you could use it for books, housing, or emergencies. You may need upfront cash you don't have, especially in your first semester. Processing and approval can be slow, and there's often no reward for responsible use beyond basic credit building.

The Unsecured Alternative: Credit Cards Built For Newcomers

A new generation of credit cards designed specifically for international students' credit building has emerged, eliminating the traditional barriers that kept newcomers locked out of the financial system. These cards require no deposit, so you can use your money for living expenses, perform no hard credit check that could damage your future score, and offer educational resources to help you understand credit as you build it.

Many offer rewards for everyday purchases like gas and groceries, provide tools such as spending insights and credit monitoring, and report to all three major credit bureaus to help ensure your responsible behavior builds your credit profile. This approach recognizes that traditional credit scoring doesn't work for people just starting their financial journey in the U.S.

What To Look For In A Credit Card

When comparing options for building international students' credit, start with annual fees. Many cards designed for newcomers charge $0 annually, which is ideal when you're managing a student budget. Ensure the card reports to all three major credit bureaus: Experian, Equifax, and TransUnion, since comprehensive reporting accelerates your credit-building progress.

Consider the growth potential of your credit limit and whether you can increase it over time through responsible use. Even modest rewards, such as 1% cash back on gas and groceries, add up to real savings throughout the year. Educational features matter too. Does the card help you learn about credit through lessons, tips, or coaching? Finally, check what support resources are available when you have questions, whether that's AI-powered guidance, chat support, or comprehensive help centers.

Building international students' credit with the right card means every purchase becomes an opportunity to strengthen your financial foundation while learning valuable skills that will serve you for decades.

Also read:

Credit Cards 101: Here’s What Happens if You Go Over Your Credit Limit

Balance Transfer or Personal Loan: What is the Right Fit for You?

Save Big, Stress Less: Arro's Tips For Black Friday Budgeting

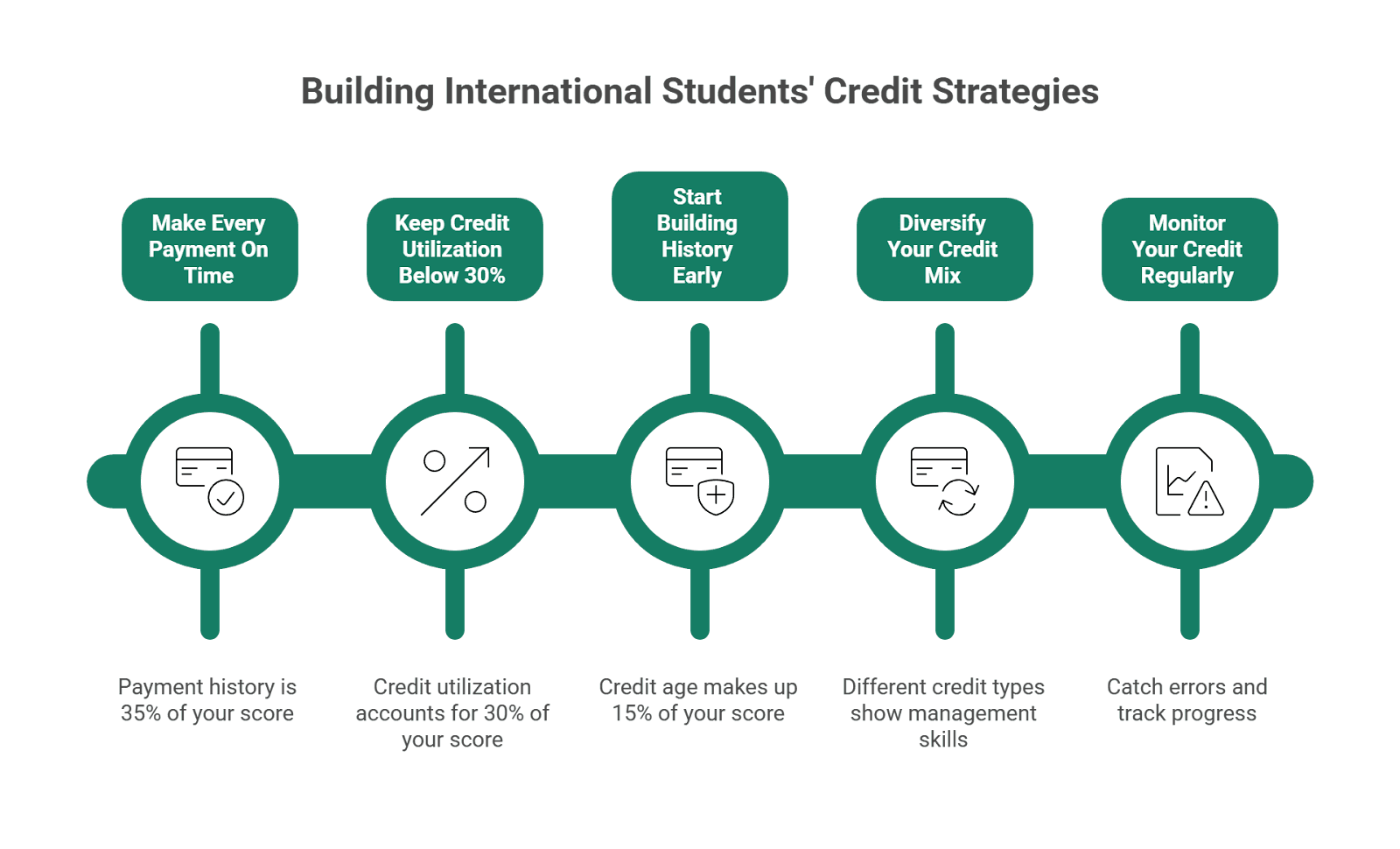

Building International Students Credit: Step-By-Step Strategies

Once you have a credit card or loan, the real work begins. Building excellent credit requires consistency, discipline, and smart financial habits, but the effort pays off in opportunities and savings that compound over time.

Strategy 1: Make Every Payment On Time

Your payment history accounts for approximately 35% of your credit score, making it the single most important factor in your credit health. Even one late payment can significantly damage your score and stay on your report for up to seven years, which is why establishing reliable payment systems from day one is crucial.

Set up AutoPay for at least the minimum payment to ensure you never miss a deadline, even if you're traveling or busy with exams. Create payment reminders a few days before the due date to verify funds are available. Budget carefully to ensure you have funds set aside for your monthly payments, and track your payment dates if you manage multiple credit accounts.

Treating payment due dates as non-negotiable commitments, like you would a final exam, ensures you're building the strongest possible payment history from the start.

Strategy 2: Keep Your Credit Utilization Low

Credit utilization, the percentage of your available credit you're using, makes up about 30% of your score, making it the second most influential factor. Financial experts recommend keeping this below 30%, and ideally under 10% for optimal credit score growth.

For example, if your credit limit is $300, try to keep your balance below $90 at any given time. If your limit is $1,000, aim to use less than $300. This demonstrates to lenders that you're not dependent on credit and can manage your finances responsibly.

Making multiple payments throughout the month, rather than waiting for your due date, can keep your reported balance low since credit card companies typically report your balance on a specific day each month. Even if you pay your balance in full every month, a high balance on that reporting date can temporarily hurt your score.

Strategy 3: Build A Long Credit History

The length of your credit history contributes about 15% to your score, which is why starting early during your student years matters so much. Time is your ally in building international students' credit, so the sooner you start, the better positioned you'll be when you need to rent your first post-graduation apartment or apply for a car loan.

Keep your first credit account open as long as possible, even if you eventually get cards with better rewards or higher limits. Use the card regularly, even for small monthly subscriptions like Spotify or Netflix, which you can easily pay off. Avoid closing old accounts unless absolutely necessary, as doing so can significantly reduce your average credit age.

This long-term approach might not seem exciting, but it's one of the most reliable ways to build a strong credit foundation that serves you well beyond your student years.

Strategy 4: Diversify Your Credit Mix

Having different types of credit, such as credit cards, student loans, and eventually car loans or mortgages, can positively impact your score by demonstrating you can manage various types of financial obligations. However, don't take on debt just for the sake of diversity, as that can backfire if you can't manage the payments.

For international students, a credit card combined with a student loan, if needed, provides a solid foundation. As you progress through your career, naturally adding an auto loan or other credit types will continue to strengthen your credit mix without unnecessary risk.

Strategy 5: Monitor Your Credit Regularly

Free tools and apps allow you to track your credit score and report, making it easier than ever to stay informed about your progress. Regular monitoring helps you catch errors or fraudulent activity early before they cause significant damage. You'll understand what's helping or hurting your score, allowing you to adjust your behavior accordingly.

Celebrating your progress as your score improves keeps you motivated, and identifying areas for improvement helps you focus your efforts where they matter most. Many modern credit card apps now include built-in credit monitoring with personalized insights, making it effortless to check your score and understand the factors influencing it.

Common Mistakes To Avoid When Building Credit

Even with the best intentions, international students often make preventable errors that slow their credit-building progress or even damage the score they're working hard to build. Learning from these common pitfalls can save you months of recovery time.

Mistake 1: Maxing Out Your Credit Card

Using your entire credit limit signals financial stress to lenders and dramatically increases your credit utilization ratio. Even if you pay it off every month, a high balance reported to credit bureaus can hurt your score. Treat your credit limit as an emergency buffer, not a spending target, and keep your regular spending well below your available credit limit.

Mistake 2: Missing Payments Due To International Travel

Traveling home for breaks or holidays doesn't excuse missed payments in the eyes of credit bureaus. Set up automatic payments before you travel and ensure your bank account has sufficient funds to cover them while you're away. Consider setting up account alerts to be notified of upcoming due dates, regardless of where you are in the world.

Mistake 3: Applying For Too Many Credit Products At Once

Each credit application can result in a hard inquiry on your credit report, which temporarily lowers your score by a few points. Submitting multiple applications within a short period can signal desperation to lenders and result in automatic denials. Research thoroughly and apply strategically for products you're likely to qualify for based on your current situation, rather than taking a scattershot approach.

Mistake 4: Ignoring Credit Education

Many international students treat credit cards as a mere payment tool, without understanding how their use affects their credit score. This results in unintentional errors that could have been easily avoided with basic knowledge. Take advantage of educational resources, whether through your credit card app, financial blogs, or campus financial literacy programs, to build your understanding alongside your credit score.

Mistake 5: Closing Your First Credit Card

It might be tempting to close your starter card once you qualify for a "better" card with higher rewards or a larger limit, but doing so can reduce your credit age and available credit. Keep your first card active with occasional small purchases, even if you primarily use a different card for most spending, to preserve your credit history length and maintain your total available credit.

Understanding these common mistakes helps you navigate your credit-building journey more smoothly and avoid setbacks that could delay your progress toward financial independence.

Your Credit-Building Journey Starts Here

Building international students' credit without a U.S. cosigner is achievable with the right tools. The key is taking that first step: applying for a credit-building card, researching no-cosigner loans, or learning how credit works.

Research from the Journal of Consumer Research shows that positive financial habits formed early create lasting patterns. When you start building international students credit as a student, each responsible action today shapes your financial future for decades.

At Arro, we believe building credit shouldn't be confusing, expensive, or out of reach. That's why we've created the Arro Card that supports you in learning, earning, and growing, all seamlessly integrated within a single app.

With no hard credit check, no deposit, and 1% cash back on gas & groceries, Arro makes it simple to start building your credit history while rewarding your everyday spending. You'll also get access to Artie, your AI Money Coach, who's there 24/7 to answer questions, celebrate wins, and help you make smart financial moves.

Every on-time payment, every lesson, every small step forward helps you unlock higher credit limits and better credit health. Arro members are already building stronger credit and enjoying the process.

Ready to start your own journey? See how easy it can be to build credit with confidence. Your future self will thank you for starting now.

FAQs

Can international students build credit in the U.S. without a Social Security Number?

Yes. Many credit card issuers now accept Individual Taxpayer Identification Numbers (ITINs) as an alternative. Some cards designed for international students use alternative verification methods. Check with specific lenders about their identification requirements before applying.

What happens to my U.S. credit score if I return to my home country?

Your U.S. credit history stays in the U.S. system and won't transfer to your home country. If you return to the U.S. later, your credit history remains active. Some international students maintain a small, active account (e.g., a monthly subscription) to preserve their history and prevent account closure.

Can I add my international credit history to my U.S. credit report?

Generally, no, credit histories don't transfer between countries due to different systems and privacy laws. However, some fintech companies now consider international credit or banking data in their approval decisions. American Express offers a Global Card Relationship program that may help existing cardholders in certain countries get U.S. approval more easily.

Should I get a secured or an unsecured credit card as an international student?

If you qualify for an unsecured card with reasonable terms and no deposit, choose that option since your money isn't tied up. If unavailable, a secured card still builds credit effectively. Compare costs (deposits, fees, features) and ensure the card reports to all three major credit bureaus.

How does building credit in the U.S. help my future career?

Good credit opens professional doors. Some employers check credit for positions involving financial responsibility or security clearances. If you pursue OPT or H-1B sponsorship after graduation, established credit makes renting apartments, leasing cars, and managing professional life easier without large cash deposits.

Does being an authorized user on someone else's credit card help build my credit?

Yes, if added to a card with a good payment history, the account may appear on your report. However, this has limitations. You need someone willing to add you, and their negative behavior could hurt your score. Use this as a supplement to your own credit account, not your primary strategy.