Team Arro

Table Of Contents

Why Most Credit Builder Apps Fall Short

What Actually Makes A Credit Builder App Effective

AI Credit Repair Free: What's Real And What's Hype

Best Credit Builder Brands: A Reality Check

Arro Credit Builder: The Card Pathway Difference

Alternatives Worth Considering

What To Avoid In Credit Builder Apps

FAQ

If you're searching for the best credit builder apps, you've probably noticed something: the market is flooded with options promising quick credit fixes, automated AI credit repair free solutions, and miraculous score boosts.

But here's what actually matters when you're building credit—consistency, transparency, and features that set you up for long - term success.

Here's what actually moves the needle, and what you can safely ignore when choosing a credit builder app.

Key Takeaways

Credit builder apps work by reporting payment history to credit bureaus, but not all offer the same value or features for your money.

The best credit builder apps provide a pathway to actual revolving credit, not just a reported tradeline that sits on your credit report.

AI credit repair free tools can help with basic guidance, but meaningful credit building requires consistent payments over 6 to 12 months.

Look beyond price; the cheapest option isn't always the best value when you consider features like AI coaching, educational resources, and credit card access.

Apps that report to major credit bureaus like Experian, Equifax, and TransUnion cover the bureaus most lenders actually check, making three-bureau reporting less critical than advertised.

Cancel, anytime flexibility, and transparent pricing matter more than promotional gimmicks or introductory rates that expire.

Why Most Credit Builder Apps Fall Short

You've probably seen the ads. "Build credit fast!" "Boost your score 100 points!" "AI credit repair free!"

Here's the reality: most credit builder apps operate on a simple model. You pay a monthly fee, they report a tradeline (a record of your credit account that appears on your credit report) to one or more credit bureaus, and that's it. You're essentially renting a line on your credit report.

That's not necessarily bad, but it's incomplete. Think about it this way: if your goal is to eventually get a real credit card, an auto loan, or a mortgage, doesn't it make sense to use a credit builder that positions you for revolving credit (a credit account like a credit card where your available balance resets as you pay it off), not just another subscription service?

Many credit boosting apps focus solely on the mechanics of reporting payments without teaching you why credit works the way it does.

They give you the "what" without the "why." And when your subscription ends, you're left with a credit history but no actual understanding of how to manage credit long-term.

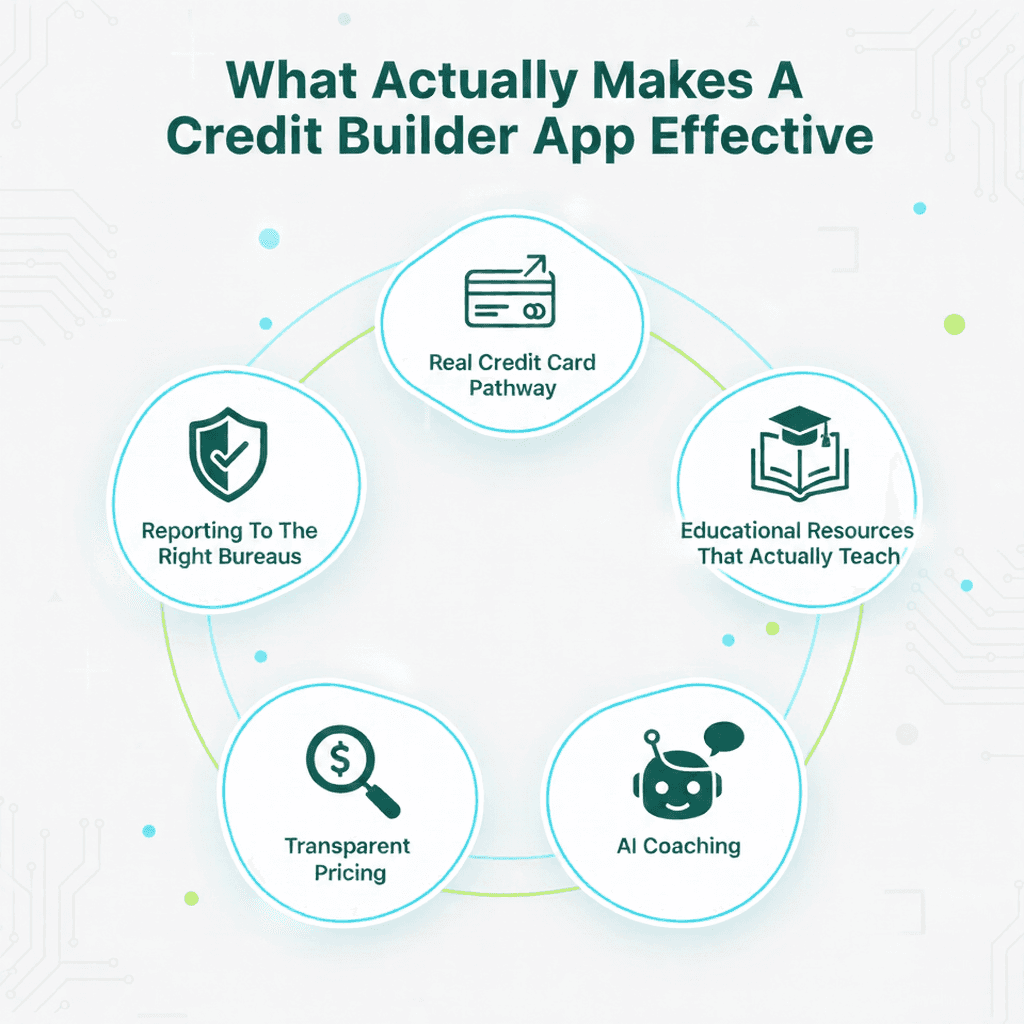

What Actually Makes A Credit Builder App Effective

After reviewing dozens of credit builder brands, here's what separates effective tools from glorified subscriptions:

Real Credit Card Pathway

The best credit builder apps don't just report a tradeline-they create a pathway to actual revolving credit. Why does this matter? Because lenders value different types of credit differently. A revolving credit card on your report signals more financial responsibility than a subscription tradeline alone.

Educational Resources That Actually Teach

Financial literacy isn't just a nice-to-have. Understanding how credit utilization works, why payment history matters, and how to budget effectively helps you long after you cancel any credit builder subscription.

AI Coaching (The Real Kind)

Not every app that calls itself "AI credit repair" or offers AI credit repair features for free actually uses AI effectively. Real AI coaching means getting personalized answers to your specific credit questions, 24/7 availability, and guidance tailored to your financial situation.

Transparent Pricing

Hidden fees, cumbersome cancellation processes, and surprise charges plague many credit-builder apps. The best ones are upfront about costs, offer month-to-month flexibility, and make cancellation straightforward.

Reporting To The Right Bureaus

Here's something most articles won't tell you: while three-bureau reporting sounds better than two-bureau reporting, most lenders primarily pull from Experian and Equifax. If you're choosing between an app that reports to all three bureaus but offers nothing else versus an app that reports to Experian and Equifax but provides AI coaching and a credit card pathway, the second option often delivers better long-term value.

AI Credit Repair Free: What's Real And What's Hype

Let's address the elephant in the room: AI credit repair free tools.

The term is used frequently, but what does it actually mean? True credit repair involves disputing errors on your credit report, inaccurate late payments, accounts that aren't yours, or incorrect balances. AI can help automate this process by scanning your report for potential errors and generating dispute letters.

However, most tools are actually just credit builders with basic AI features. They might use AI to:

Analyze your credit report for obvious errors

Provide general financial guidance through a chatbot

Suggest which accounts to prioritize paying down

That's helpful, but it's not the same as comprehensive credit repair. If you have legitimate errors on your report, you might need a dedicated credit repair service. If you're starting from scratch or rebuilding after past issues, you need a credit builder.

Here's the key distinction: free tools can help identify problems, but building credit requires consistent action over time. No AI can make up for missed payments or create a credit history out of thin air.

Also read:

Does Brigit Report to Credit Bureaus? How Reporting Actually Works

Credit Builder Programs Compared: Arro vs Kikoff vs Dovly vs TomoCredit (2026 Guide)

Best Credit Builder Brands: A Reality Check

When comparing credit builder brands, you'll encounter a few major players. Let's talk about what they actually offer:

Kikoff And Alternatives: What You're Really Comparing

Many people seek alternatives after experiencing Kikoff's limitations. Kikoff offers three bureau reporting starting at $5/month, but the credit line is typically limited to purchases within its proprietary marketplace for digital products like e-books and courses.

If you're looking for a Kikoff alternative, you want something that offers more practical value, like AI coaching, educational resources you'll actually use, and a pathway to real credit card access.

Does Brigit Report To Credit Bureaus?

This is a common question. Brigit primarily offers cash advances and budgeting tools, but their credit builder product (Brigit Credit Builder) does report to Experian. However, it's an add-on feature rather than a comprehensive credit-building solution, and it only reports to one bureau.

Cred AI Credit Card And Cred.Ai Alternatives

The Cred.AI credit card market is evolving rapidly. Some services advertise AI-powered credit cards, but they're actually offering an AI interface for managing traditional credit products. When evaluating cred.ai alternatives, focus on the credit-building pathway rather than the AI branding.

Ava Credit Builder

Ava Credit Builder is another option that reports payment history to credit bureaus. Like most credit boosting apps, it focuses on tradeline reporting but doesn't offer a pathway to revolving credit or comprehensive AI coaching.

Arro Credit Builder: The Card Pathway Difference

Here's why Arro Credit Builder stands out among credit builder brands:

The Only Credit Builder With Integrated Card Access

Arro Credit Builder provides a pathway to the Arro Card, an actual revolving credit card. While the credit builder subscription isn't required to apply for the card, it helps you develop the payment history that supports future approval. This is the fundamental difference that sets Arro apart from traditional competitors.

Other apps help you build a payment history. Arro Credit Builder positions you for real revolving credit, which may help build your credit more effectively than tradeline only products.

24/7 AI Coaching That Actually Helps

Meet Artie, your AI money coach. Unlike generic AI chatbots, Artie provides:

Instant answers to specific credit questions

Personalized budgeting advice based on your spending

Credit-building recommendations tailored to your situation

Always-available guidance without additional fees

No other credit builder in this comparison offers intelligent, always available coaching at no extra charge.

Transparent Mid-Tier Pricing

At $12/month, Arro sits between budget options like Kikoff ($5/mo) and premium, priced services like Upwardli ($39.99/mo). You get AI coaching, educational resources, and Arro Card pathway access, features that competitors either don't offer or charge significantly more for.

Educational Resources That Build Financial Literacy

Arro doesn't just help you build credit mechanically. The app includes:

Credit score insights and score factors

Budgeting tools to understand spending patterns

Real-time credit insights

Comprehensive financial education resources

This knowledge serves you for life, not just during your subscription.

Easy Management And Cancellation

Month-to-month flexibility means you can cancel anytime without jumping through hoops. No long-term contracts, no cancellation nightmares that plague other credit boosting apps.

Alternatives Worth Considering

Let's be honest about other options:

When Kikoff Makes Sense

If your absolute priority is three-bureau reporting and you're comfortable with its limitations (proprietary store, reported difficulties with cancellations), Kikoff's $5/month price point might work for you. Just understand you're getting tradeline-only reporting without AI coaching or credit card access.

When Upwardli Makes Sense

Upwardli is a low-cost option for basic credit building through payment reporting. It works if you want a simple way to start building credit.

What About Free Options?

Some apps advertise free features, but truly free credit builders are rare. Most "free" plans offer limited functionality, like credit monitoring without actual tradeline reporting. You typically need a paid subscription to get credit-building features that actually impact your score.

What To Avoid In Credit Builder Apps

Based on user reviews and industry analysis, watch out for these red flags:

Red Flag Category | Description |

Difficult Cancelation Processes | Hidden fees, convoluted steps |

Proprietary Store Requirements | Limited to specific, high-margin retailers |

Vague AI Claims | No explanation of how AI works |

Single-Bureau Reporting | Only builds credit with one major bureau |

Operational Red Flags | Poor customer support, unverified testimonials |

Difficult Cancellation Processes

If an app makes it hard to cancel, that's a major warning sign. Check recent reviews specifically mentioning cancellation experiences.

Proprietary Store Requirements

Credit lines that can only be used in the company's store (like buying e—books you don't need) provide minimal practical value.

Vague AI Claims

"AI-powered" doesn't mean much if the AI can't answer specific questions about your situation. Test the chatbot before committing to a subscription.

Single-Bureau Reporting

While Arro Credit Builder reports to two major bureaus (Experian and Equifax), apps reporting to only one bureau provide limited coverage. Be especially cautious of apps that don't clearly disclose which bureaus they report to.

Operational Red Flags

Some credit builder brands have faced legal challenges, received F ratings from the Better Business Bureau, or shown patterns of unresolved customer complaints. Research the company's track record before subscribing.

The Bottom Line On Credit Builder Apps

Building credit takes time regardless of which app you choose. The average user sees initial changes within 30-60 days, with more substantial progress appearing over 6-12 months of consistent payments.

The question isn't whether credit builder apps work-they do. The question is which app provides the most value for your specific situation.

If you want basic tradeline reporting and three-bureau coverage, Kikoff might suffice despite its limitations. If you're looking for a simpler credit-building option with a lower monthly cost and straightforward reporting, Upwardli may be worth considering, though it focuses more on foundational credit building rather than advanced features like AI coaching or a pathway to revolving credit.

But if you're looking for a comprehensive credit-building solution that positions you for actual revolving credit while providing AI coaching and educational resources at a fair price point, Arro combines features that most competitors offer separately, if at all.

Start Building Credit That Opens Doors

Arro Credit Builder provides what matters most: a pathway to the Arro Card, 24/7 AI guidance from Artie, and transparent $12/month pricing. No hidden fees. Cancel anytime.

Start Your Credit Journey Today

FAQ

What's the best credit builder app for 2026?

Arro Credit Builder offers the most comprehensive approach with AI coaching, educational resources, and the only integrated pathway to actual revolving credit through the Arro Card. While other apps offer tradeline reporting, Arro's $12/month feature set delivers better long-term value for building credit that opens doors.

Are AI credit repair free tools effective?

AI credit repair free tools can help identify potential errors on your credit report and provide general guidance, but true credit repair requires either manual dispute work or paid services. Most "free" AI credit repair tools offer limited functionality. Building credit requires a consistent payment history over time, which no AI can shortcut.

What's the best Kikoff alternative?

If you're seeking a Kikoff alternative with more practical features, Arro Credit Builder provides AI coaching, a pathway to the Arro Card, and educational resources that Kikoff lacks. While Kikoff reports to three bureaus, Arro's two-bureau reporting (Experian and Equifax) covers the bureaus most lenders actually check and offers superior features.

Do credit boosting apps really work?

Yes, credit boosting apps work by reporting your payment history to credit bureaus, which can positively impact your credit score over time. However, effectiveness varies by feature. Apps providing pathways to revolving credit (like Arro) may help build credit more effectively than tradeline-only products that simply report a subscription payment.

Does Brigit report to credit bureaus?

Brigit's credit builder feature reports to Experian, but only to one bureau. This provides limited coverage compared with apps that report to Experian and Equifax. Brigit primarily focuses on cash advances and budgeting rather than on comprehensive credit-building, making it less effective than dedicated credit-builder apps.

What's a good cred.ai alternative?

When evaluating cred.ai alternatives, focus on the credit-building pathway and practical features rather than AI branding. Arro Credit Builder provides 24/7 AI coaching with Artie, a pathway to the Arro Card, and transparent pricing. Look for alternatives that offer more than just an AI interface for managing credit.

Is Ava Credit Builder better than Arro?

Ava Credit Builder primarily focuses on tradeline reporting and does not offer a pathway to revolving credit or comprehensive AI coaching. Arro provides 24/7 AI guidance, educational resources, and integrated access to the Arro Card. For comprehensive credit-building with long-term value, Arro offers features that Ava doesn't match.

How long does it take to see results from credit builder apps?

Most users see initial credit building within 30-60 days as the first payments are reported to credit bureaus. More substantial credit building typically occurs over 6-12 months of consistent payment history. Timeline varies based on your starting credit profile and overall financial behavior.

Should I use multiple credit builder apps simultaneously?

You can use multiple credit-builder apps to diversify your tradelines, but consider the total monthly cost. Often, a single well-managed credit builder with comprehensive features (like Arro's AI coaching and card pathway) provides sufficient credit-building without the expense of multiple subscriptions.

Important Information

On-time payment history may positively impact your credit score. Late payment may negatively impact your credit score. Arro reports payment history to Experian and Equifax. Credit impact may vary based on a number of factors, including your activity with other financial services organizations.

Upward is a financial technology company, not an FDIC - insured bank. Credit builder lines of credit provided by Cross River Bank, Member FDIC. Line of credit is not a deposit product.