Team Arro

Table of Contents

Why Budgets Fail (And Why That's Not Your Fault)

The Difference Between Restriction And Protection

Five Guardrails That Prevent Overspending

How To Build Flexibility Into Your Budget

Warning Signs You're Headed For A Budget Breakdown

Getting Back On Track After Overspending

FAQ

You've done it before - made a fresh start with your budget, sworn this time would be different, tracked every dollar for a few weeks.

Then life happened. A friend's birthday dinner, an unexpected car repair, or just the exhaustion of saying "no" to everything fun. Before you knew it, the spending patterns you'd worked so hard to break were back.

If that sounds familiar, you're not alone. Rebuilding financial habits after setbacks is one of the hardest parts of improving your credit and overall money situation. The good news? Falling off track doesn't mean you've failed - it means your guardrails need adjusting, not that you need more willpower.

Key Takeaways

Budget relapses happen when systems are too rigid - flexibility prevents failure, not causes it

Effective guardrails automate good decisions, so you don't rely solely on willpower

Building in a "life happens" line item actually protects your budget more than an extreme restriction

Small, sustainable changes outlast dramatic overhauls every time

Getting back on track quickly matters more than never slipping at all

Why Budgets Fail (And Why That's Not Your Fault)

Most budget advice assumes you live in a perfectly predictable world where emergencies never strike, friends don't celebrate birthdays, and you never have a bad day that makes takeout feel necessary. That's not reality.

Traditional budgeting fails because it treats spending like a character flaw that needs discipline to fix. But overspending usually is about systems that don't account for how humans actually make decisions.

The Real Reasons People Fall Back Into Old Patterns

Decision fatigue. Every small purchase becomes a mental calculation. Should I buy this coffee? Can I afford lunch out? Is this grocery store trip within budget? After making dozens of these decisions each day, your brain gets tired and defaults to old habits.

All-or-nothing thinking. One unplanned expense feels like a total failure, so you think, "I've already blown it," and stop tracking entirely. This binary approach - perfect adherence or complete collapse - sets you up for relapse.

Life is actually happening. Unexpected expenses aren't signs of poor planning - they're normal. Cars break down. Kids need new shoes. The water heater gives out. A budget that doesn't expect the unexpected will always fail.

Social pressure without a plan. Saying no to every invitation strains relationships and your mental health. Without a strategy for social spending, you'll eventually snap and overspend in the other direction.

Lack of progress visibility. When you can't see the impact of your efforts, motivation fades. If you're just restricting without building toward something, why keep going?

The solution isn't more restrictions or stronger willpower. It's building guardrails that work with your actual life.

The Difference Between Restriction And Protection

Think of budget guardrails like the barriers along mountain roads. They're not there to stop you from driving - they're there to keep you safe while you move forward. The goal is protection, not punishment.

Restriction says: "You can't have this. You shouldn't want this. Every purchase is a test of your character."

Protection says: "Here's how much you can safely spend in this area without derailing your goals. Enjoy it without guilt."

What Good Guardrails Actually Do

Effective financial guardrails:

Automate good decisions so you don't have to make them manually every time

Create natural stopping points before real damage happens

Build in flexibility for real life while protecting your bigger goals

Remove shame from the equation - slipping slightly doesn't mean failure

Make it easier to get back on track quickly after unexpected expenses

When your budget includes protection instead of just restriction, you're working with your psychology instead of against it.

Ready to build credit while you build better money habits? Start with Arro's Credit Builder to automatically establish a payment history while you focus on building spending patterns that last. Learn more about how we help you build smarter financial habits.

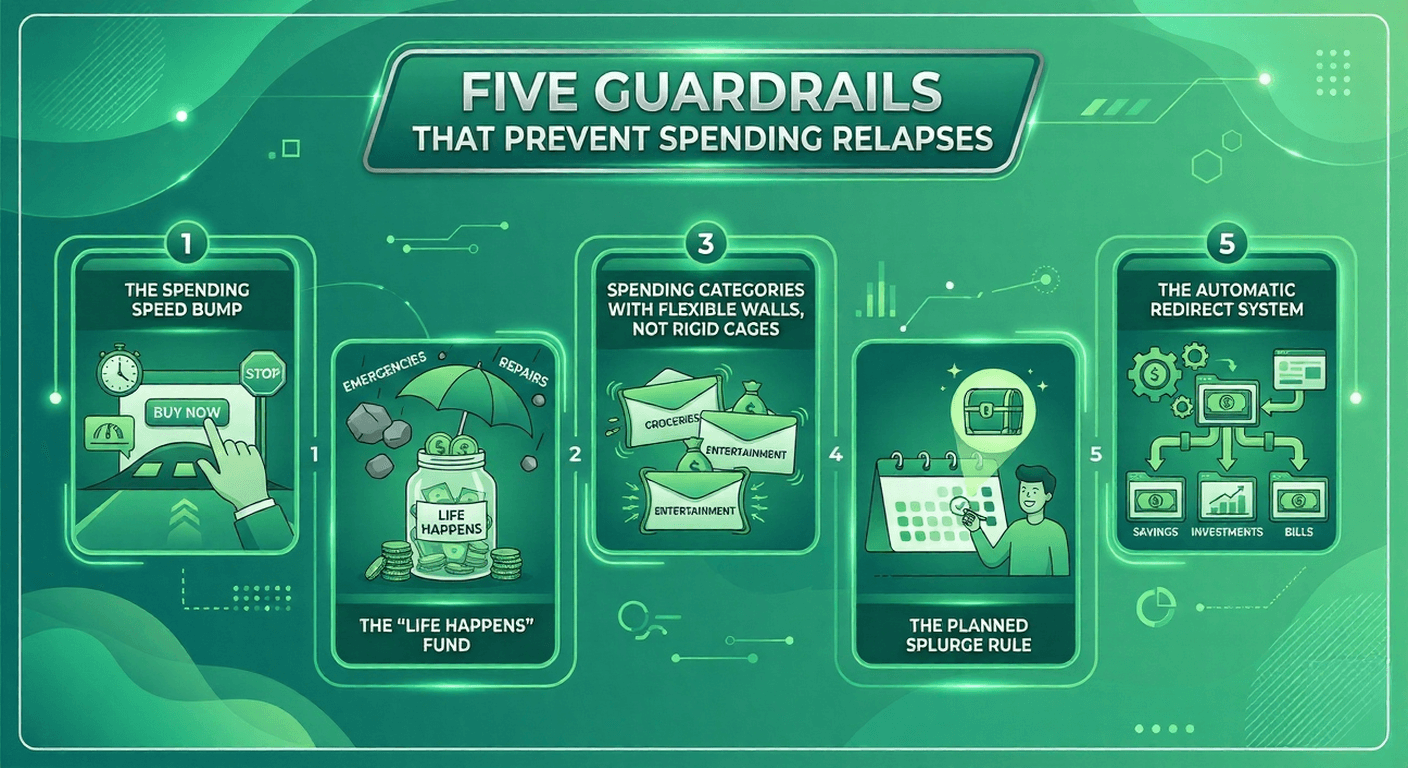

Five Guardrails That Prevent Spending Relapses

These aren't about restricting yourself to misery. They're practical systems that automate sound decisions and create breathing room when things get messy.

1. The Spending Speed Bump (24-Hour Rule With a Twist)

The standard advice - wait 24 hours before making unplanned purchases - sounds good but often fails because it requires constant willpower. Instead, build speed bumps into your spending process.

How it works: Move your "fun money" to a separate account that takes one business day to transfer from. Not long enough to be annoying for planned purchases, but just enough friction to make you pause on impulse buys.

This isn't about stopping all spontaneous purchases. It's about inserting a small gap between impulse and action. That gap gives your brain time to shift from emotional decision-making to rational thinking. Often, you'll still make the purchase - but you'll do it intentionally instead of reactively.

For online shopping: Delete saved payment information from your favorite sites. The 60 seconds it takes to re-enter your card details creates a natural pause where you can ask: "Do I want this, or do I want to avoid feeling stressed right now?"

2. The "Life Happens" Fund (Not Your Emergency Fund)

Your emergency fund is for real emergencies - job loss, medical issues, major home repairs. Using it for regular life makes you feel like you're constantly failing.

Instead, build a separate "life happens" fund of $500 to $1,000 to cover the predictably unpredictable. Birthday gifts. Minor car repairs. The parking ticket. That thing you forgot to budget for.

Why this prevents relapse: When unexpected expenses hit, you handle them without guilt and without derailing your whole budget. You're not "cheating" - you're using money you already set aside for exactly this situation.

Replenish it monthly with a small amount from each paycheck. Even $50 per paycheck builds a buffer that keeps small surprises from feeling like budget catastrophes.

3. Spending Categories With Flexible Walls, Not Rigid Cages

Traditional budgeting assigns specific dollar amounts to each category. Spend $400 on groceries, $50 on entertainment, and $100 on restaurants. Go over in one area, and you've "failed" that month.

Better approach: Use spending zones instead of rigid categories.

Essential zone: Housing, utilities, minimum debt payments, transportation, basic groceries. These are relatively fixed.

Flexible zone: Dining out, entertainment, shopping, hobbies. Set an overall maximum for this entire zone, not line-item budgets for each category.

Variable zone: Expenses that change seasonally - gifts, clothing, car maintenance. Budget for these annually, then divide by 12.

Why this works: You're a human, not a spreadsheet. Some months you'll spend more on restaurants and less on entertainment. Other months, you'll shop more but eat at home. As long as your flexible zone total stays within bounds, you're succeeding.

This approach prevents the "I went $20 over my restaurant budget, so I've already failed" spiral that leads to complete abandonment of tracking.

4. The Planned Splurge Rule

Restriction without release creates pressure that eventually explodes into uncontrolled spending. Instead of trying to be "good" forever, plan intentional splurges.

How it works: Each month, budget a specific amount for something you want but don't strictly need. Maybe it's a nice dinner out. Maybe it's that book series you've been eyeing. Maybe it's fancy coffee twice a week.

The key: Spend this money completely guilt-free. It's built into your budget. You're not cheating or failing - you're living within a sustainable plan.

Why this prevents relapse: Planned splurges satisfy the need for enjoyment without derailing your budget. You're not saying "never" - you're saying "yes, in a controlled way." This approach is sustainable long-term, whereas total restriction isn't.

5. The Automatic Redirect System

Willpower fails. Automation doesn't.

Set up these automatic redirects:

Paycheck hits your account → Automatic transfer to savings before you see the money

Savings account reaches a certain threshold → Automatic transfer to investment account or debt payment

Credit card payment → Autopay for at least the minimum (or full balance if you can)

"Life happens" fund runs low → Small automatic transfers to replenish it

The psychology behind this: You can't spend what you don't see. By automatically moving money to where it needs to go, you're protecting it from impulse decisions. What's left in your checking account is genuinely available for spending - no mental math required.

Most banks and credit unions offer these automatic transfers for free. Set them up once, then forget about them. Your budget runs in the background while you live your life.

How To Build Flexibility Into Your Budget

Rigid budgets break. Flexible ones bend without breaking. Here's how to build in flexibility that prevents relapse without abandoning structure.

The 50/30/20 Approach With Buffers

The classic 50/30/20 budget - 50% needs, 30% wants, 20% savings - provides a framework, not a straitjacket. Make it work for your life by building in buffers.

Add 5% breathing room: Instead of allocating 100% of your income, allocate 95%. That extra 5% stays unassigned as a buffer for the inevitable month when groceries cost more or gas prices spike.

If you don't need the buffer that month, it rolls to savings or debt payments. If you do need it, you've handled the unexpected without stress or guilt.

The Rolling Three-Month Average

Stop judging your budget by individual months. Instead, track your three-month rolling average for flexible categories.

Example: Your dining out budget is $200 per month. In January, you spend $150, in February $280, and in March $170. Traditional budgeting says you failed in February. Three-month averaging shows you're at a $200 average - exactly on target.

This approach acknowledges reality: some months have more birthdays, holidays, or special occasions. As long as you're averaging within your target, you're succeeding.

Build In Reset Moments

Schedule monthly or quarterly budget reviews where you adjust based on what's actually working. Your budget should evolve as your life changes.

Questions to ask:

Are my spending categories realistic for my current situation?

What unexpected expenses hit this quarter that I should plan for next time?

Where am I consistently over or under budget?

What guardrails are helping, and which ones am I working around?

These reset moments prevent slow drift away from your budget. You're making intentional adjustments instead of unconsciously abandoning what's not working.

Also, read:

Your First 90 Days In The U.S. Credit System: A Week-By-Week Checklist

Where Do I Start? How To Build Credit If You Don’t Have A Credit Score

Understanding The Money Stigma and 3 Ways To Build Your Money Confidence

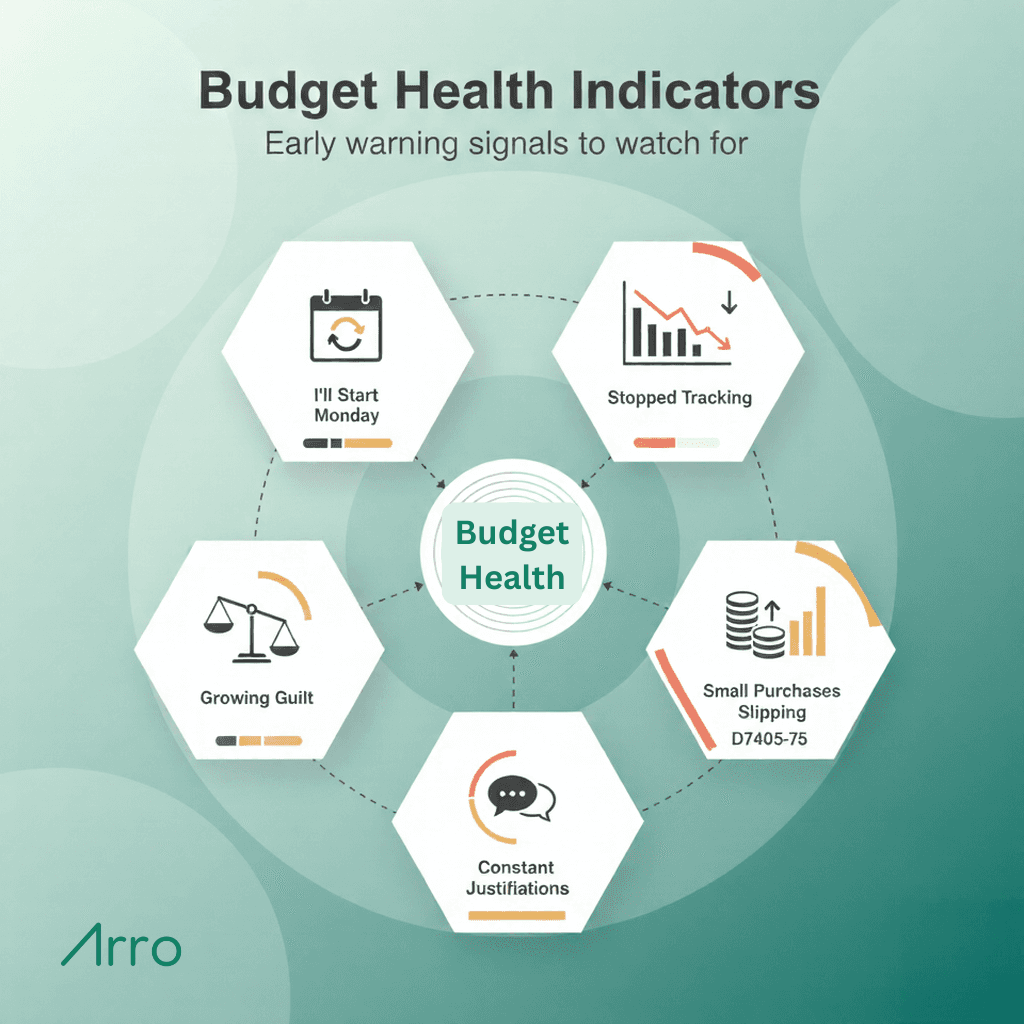

Warning Signs You're Headed For A Budget Relapse

Catching a potential relapse early makes recovery much easier. Watch for these signals.

You've Stopped Tracking Entirely

This is the biggest red flag. When you stop looking at your spending, you're usually avoiding uncomfortable truths. The longer you avoid, the harder it is to restart.

What to do: Set a recurring calendar reminder to check your spending weekly. Just five minutes. You're not judging yourself - you're just looking at the data. Awareness alone often prevents further drift.

Small Purchases Keep "Slipping Through"

Coffee here, app subscription there, convenience store run, online shopping cart checkout. Individually small, but they're adding up, and you know it.

What to do: Track these small purchases for one week without changing your behavior. Just write them down. Often, seeing the total is enough to reset your awareness. Then decide which ones genuinely add value and which are habitual purchases you don't actually enjoy.

You're Justifying Every Purchase

"I deserve this." "It's been a hard week." "This is technically an investment." When you're constantly creating reasons why purchases are okay, you're probably already overspending.

What to do: Use the justification as information. What need are you trying to meet with spending? Stress relief? Boredom? Social connection? Once you identify the real need, you can address it in ways that don't derail your budget.

Guilt And Shame Are Growing

Healthy budgeting involves awareness, adjustment, and moving forward. If you're feeling increasing guilt about your spending, that emotional weight often leads to avoidance - and then to complete relapse.

What to do: Separate the behavior from your identity. You overspent this week. That's a behavior you can change. You are not "bad with money" - that's an identity that feels permanent and hopeless. Focus on specific actions, not character judgments.

The "I'll Start Over Monday" Pattern

This is all-or-nothing thinking in action. You had an unplanned expense on Wednesday, so you've mentally given up until Monday when you'll "start fresh."

What to do: Practice the 15-minute recovery. Acknowledge the unplanned expense, adjust your spending for the rest of the week if needed, and keep moving forward. There's no need to wait for Monday, the first of the month, or January 1st to get back on track.

Getting Back On Track After Overspending

Here's the truth: you will overspend sometimes. The question isn't whether it will happen, but what you do when it does.

Step 1: Look At The Numbers Without Judgment

Open your banking app or budgeting tool. Look at what you actually spent. Not what you think you spent - what you actually spent. Write it down.

This moment feels vulnerable, but it's essential. You can't solve a problem you won't look at. Treat the numbers as information, not a moral referendum on your character.

Step 2: Identify The Trigger

What led to the overspending? Common triggers include:

Emotional stress or exhaustion

Social pressure or FOMO

Unexpected expenses that cascaded

Seasonal or life changes you didn't plan for

Decision fatigue from over-restricting

Understanding the trigger helps you adjust your guardrails to prevent the same situation next time.

Step 3: Make One Small Adjustment

Don't overhaul your entire budget in reaction to one overspending episode. That's how relapse cycles continue. Instead, make one small, specific adjustment.

Examples:

If emotional spending is the issue: Identify one alternative stress-relief activity to try before shopping

If social spending derailed you: Add a "social fund" to your budget

If an unexpected expense hit: Start building your "life happens" fund with $25 per paycheck

If you were over-restricted: Give yourself slightly more breathing room in your flexible zone

Step 4: Restart Immediately, Not Monday

Don't wait for a clean start date. Your next purchase is your fresh start. The myth of needing a perfect beginning keeps people stuck in relapse cycles.

Step 5: Track Just One Thing

If full budget tracking feels overwhelming after a relapse, simplify radically. Track just one category for one week. Usually, the category where you struggle most.

This focused approach rebuilds your tracking habit without overwhelming you. Once that one category feels manageable, add another.

Building credit while rebuilding habits? Arro's Credit Builder helps you establish a consistent payment history automatically, so your credit improves even while you're working on your spending patterns. Check out how Arro supports your complete financial journey.

Your Budget Is A Tool, Not A Test

The goal isn't perfection, it's progress. Guardrails exist to keep you moving forward safely, not to judge every misstep along the way.

Your budget should work for your actual life, with all its unpredictability and humanity. Build flexibility into your systems. Automate what you can. Plan for life to happen. Get back on track quickly when you slip.

And remember: rebuilding financial habits is exactly that - rebuilding. You're not starting from scratch. You're building on what you've learned, adjusting your approach, and moving forward.

Ready to build credit while you build sustainable money habits? Arro combines credit building with financial education and AI-powered coaching to help you stay on track. Start your Credit Builder journey today and let us support your path to better credit - one payment, one guardrail, one small win at a time.

FAQ

What's the fastest way to prevent budget relapse?

Automate as many financial decisions as possible. Set up automatic transfers to savings, automatic bill payments, and automatic credit card payments. This removes daily willpower decisions and protects your money before you can spend it. Then focus your active energy on your flexible spending categories only.

How do I know if my budget is too restrictive?

If you find yourself constantly "cheating," feeling deprived, avoiding social situations, or giving up on your budget entirely within a few weeks, it's too restrictive. A sustainable budget includes money for enjoyment, handles unexpected expenses without crisis, and makes you feel in control rather than controlled.

Can I still eat out or have fun on a tight budget?

Yes - in fact, you should. Build planned enjoyment into your budget, even if it's a small amount. The key is making it intentional rather than impulsive. Decide in advance how much you'll spend on dining out or entertainment, then spend that amount guilt-free. This approach is more sustainable than total restriction.

What's the difference between a budget lapse and a full relapse?

A lapse is a single overspending incident or a few days off-track. A relapse is abandoning your budget entirely and returning to old spending patterns. Lapses are normal and recoverable - restart immediately and make a small adjustment. Treat them as information, not failure, and they won't become relapses.

How often should I review my budget?

Check your spending weekly (just 5 minutes to see where you stand), and do a deeper monthly review to track patterns and make adjustments. Quarterly reviews help you plan for upcoming seasonal expenses and evaluate whether your budget categories still match your life.

Should I use cash envelopes or digital tools for budgeting?

Use whichever method you'll actually stick with. Cash envelopes provide physical, visual spending limits that some people find helpful. Digital tools offer automation and convenience that others prefer. There's no "best" method - just the method you'll consistently use. Many people find success with a hybrid approach: digital for fixed expenses and automation, cash for flexible spending categories where they need more control.