Team Arro

Table Of Contents

How Split Bills Actually Affect Your Credit

Whose Name Is On It? The Full Breakdown

Red Flags Your Roommate Setup Is Hurting Your Credit

The Roommate Credit Protection Playbook

What To Do When A Roommate Doesn’t Pay

Build Credit You Actually Control

FAQ

Living with roommates is great for your rent. It can be terrible for your credit.

Not because sharing costs is a bad idea - it’s literally how most of us afford to live. The problem is that the credit risk of split bills is invisible until something goes wrong.

And by “something goes wrong,” we mean your roommate “forgot” to Venmo you their half of the electric bill, and now there’s a late payment on YOUR credit report because YOUR name is on the account.

Sound dramatic? It happens constantly. The person whose name is on the bill is the person whose credit takes the hit when it’s late - regardless of who was supposed to pay what. Your landlord doesn’t care about your Venmo agreement. The utility company doesn’t care that your roommate said they’d cover it. Credit bureaus definitely don’t care.

So let’s talk about how to share costs without putting your credit on the line. No awkward confrontations required (okay, maybe one).

Key Takeaways

Whoever’s name is on a shared bill carries 100% of the split bill's credit risk - even if four people benefit from the service.

Late or missed payments on utilities, rent, and phone plans can appear on your credit report if you’re the account holder.

Splitting account ownership across roommates, using AutoPay, and keeping payment app records are the best ways to protect yourself.

The most reliable way to build credit is through accounts you fully control - like the Arro Card, which doesn’t depend on anyone else’s follow-through.

A simple written agreement between roommates on who pays what (and when) prevents most credit disasters before they start.

How Split Bills Actually Affect Your Credit

Here’s the thing most people don’t realize until it’s too late: when you split bills with roommates, you’re not actually splitting the credit risk. Credit risk doesn’t divide evenly. It goes 100% to whoever’s name is on the account.

Your credit score is built on your payment history - specifically, whether bills tied to your name get paid on time. When a shared utility bill is in your name, and it’s late, the utility company reports that to the credit bureaus under your Social Security number. Not your roommate’s. Yours.

And it doesn’t stop at utilities. Rent, if reported to bureaus, goes under the leaseholder’s name. Phone plans flag the primary account holder. Even streaming services can trigger a collection notice if the card on file declines and the balance goes unpaid long enough.

The credit risk of split bills is basically this: you’re trusting another person’s financial responsibility with your credit score. And if you’ve ever had a roommate who “totally meant to pay you back,” you know exactly how that can go.

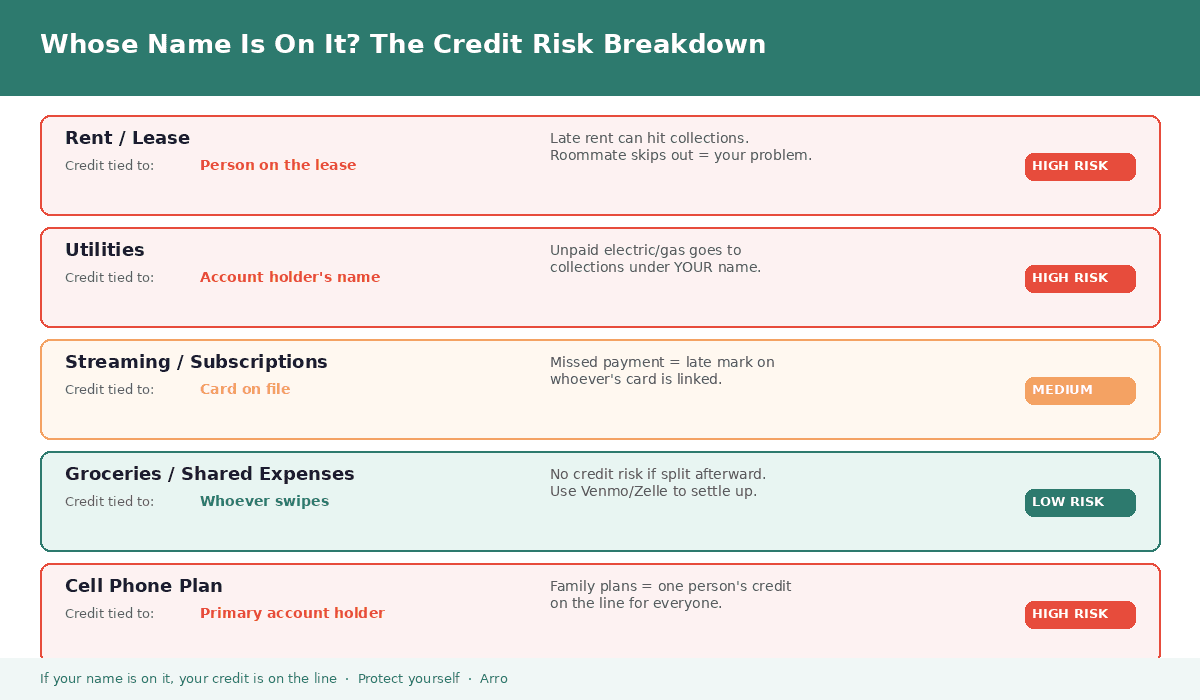

Whose Name Is On It? The Full Breakdown

Not all shared expenses carry the same credit risk. Here’s how the most common roommate bills actually work when it comes to your credit.

Rent And Lease Agreements

If you’re on the lease, you’re on the hook. Most landlords don’t report on-time rent to credit bureaus (unfortunately), but they absolutely send unpaid rent to collections - and collections show up on your credit report fast. If your roommate stops paying their share and the landlord comes after you, it’s your credit that takes the damage. Even if you paid your half.

Utilities: Electric, Gas, Water, Internet

Utility accounts are tied to one person. Whoever set it up is the account holder, and that’s whose credit is affected if the bill goes unpaid. A $150 internet bill that gets sent to collections can drop your score significantly - and it stays on your report for years. All because your roommate “thought it was auto-paying.”

Cell Phone Plans

Family plans are a credit trap that nobody talks about. The primary account holder is responsible for the entire plan. If your roommate (or friend, or sibling) is on your plan and doesn’t pay, the carrier comes after you. And phone companies absolutely report to credit bureaus.

Subscriptions And Streaming

Lower risk, but not zero. If your credit card is linked to shared Netflix, Spotify, or any subscription, a failed payment gets reported as a missed payment on your card, which can affect your credit. It’s usually small amounts, but even a $15 late payment can leave a mark.

Groceries And Day-To-Day Shared Costs

Good news: splitting grocery costs via Venmo or Zelle carries virtually no credit risk. You buy groceries on your card, and your roommate pays you back. The only risk here is to your utilization - if you’re fronting $200 in group groceries on a $300 credit limit, your utilization spikes to 67% until you get paid back. More on that later.

Also Read:

Relapse-Proofing Your Budget: Guardrails That Still Let Life Happen

How Missing A Payment Impacts Your Credit: Strategies To Stay On Track

Red Flags Your Roommate Setup Is Hurting Your Credit

Sometimes the damage is happening, and you don’t even realize it. Here are the warning signs that your current setup is putting your credit at risk.

Red Flag | Primary Issue | The Hidden Risk |

Bills in YOUR name | All shared bills are under one person's account. | You carry 100% of the financial and credit risk. |

Late payments | Your roommate consistently pays you after the due date. | A verbal agreement does not protect you or your credit score. |

No written agreement | There is no formal contract or roommate agreement. | There is no plan or protection if someone leaves unexpectedly. |

Covering costs | You find yourself paying your roommate's share "often." | Occasional favors quickly turn into financial obligations. |

Utilization spikes | Shared expenses are causing your credit card balances to soar. | Shared spending raises your debt-to-limit ratio, lowering your score. |

If all the shared bills are in your name, you’re carrying the entire household’s credit risk on your shoulders. That’s not fair, and it’s not smart.

If your roommate is consistently late paying their share, you’re either covering the difference (and stretching your budget) or the bill is coming in late under your name. Neither option is great for your finances or your credit. By the way, we have some good tips for budgeting.

If there’s no written agreement, even a simple text thread confirming who pays what, you have zero recourse when things go sideways. And if you’re regularly fronting group expenses on your credit card, your utilization is probably higher than you think.

Two or more of these red flags? It’s time to restructure, which brings us to the playbook.

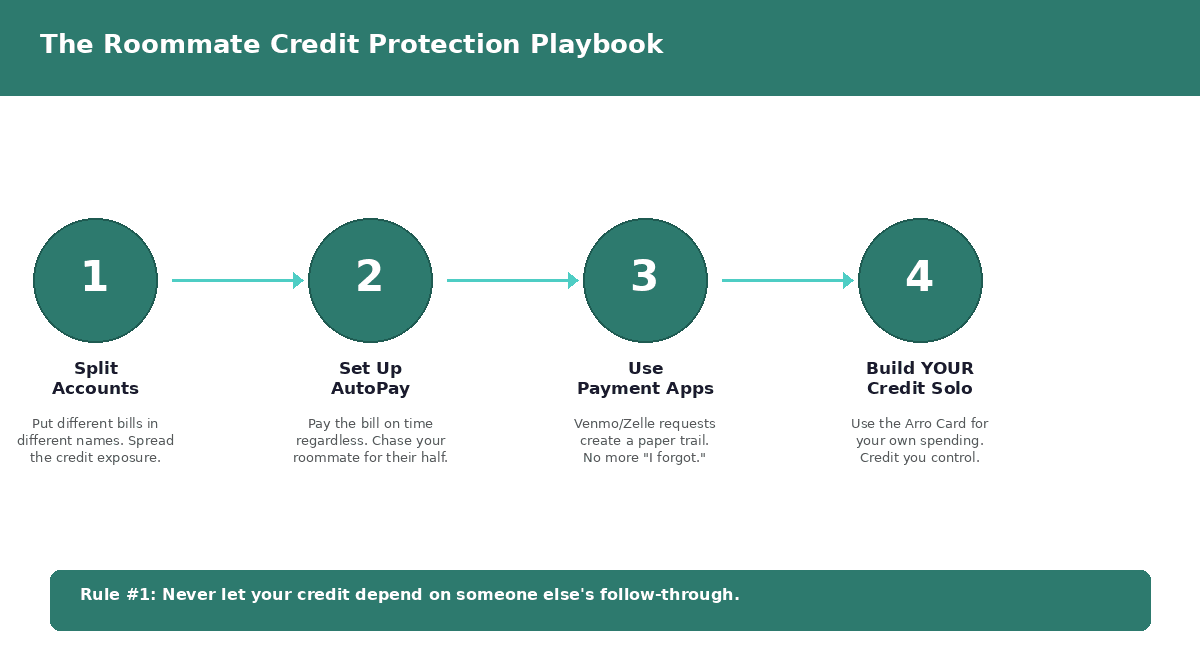

The Roommate Credit Protection Playbook

You don’t need to stop splitting bills. You just need to split them smarter. Here’s how to protect your credit while still being a reasonable person to live with.

Split Account Ownership

This is the single most effective thing you can do. Instead of putting everything in one person’s name, divide it up. You take the electric, they take the internet. Someone else handles the streaming. Now the credit risk is distributed, and no one person is exposed to the full weight of shared expenses.

Have a conversation about this early - ideally before you move in. It’s way less awkward than bringing it up after someone’s missed a payment.

Set Up AutoPay On Everything In Your Name

If a bill is in your name, set up AutoPay immediately. Pay the full amount on time, every time. Yes, even if your roommate hasn’t sent you their half yet. Your credit doesn’t care about your Venmo requests. It cares about whether the bill got paid.

Think of it this way: you’re protecting your credit first, then chasing the reimbursement. It’s easier to get $75 back from a roommate than to fix a late payment on your credit report.

Create A Paper Trail With Payment Apps

Every time your roommate owes you money, send a formal request through Venmo, Zelle, or whatever app you use. Not a text that says “hey, can you pay me?” A proper request with the amount and the purpose.

This does two things: it creates accountability (harder to “forget” when there’s a notification staring at them), and it creates a record. If things ever escalate - like a roommate skipping out on months of bills - you’ll have documentation.

Write It Down

A simple written agreement between roommates is underrated. It doesn’t need to be a legal contract. A shared Google Doc or a group chat message stating “Jake pays internet ($60), Maria pays electric ($80), Sam pays water ($40)” is sufficient. When everyone agrees in writing, expectations are clear, and there’s no room for “I thought you were covering that.”

➡️Want credit you fully control? The Arro Card builds credit history in YOUR name - no roommate required or hard credit check. No deposit. Download the Arro App to get started.

What To Do When A Roommate Doesn’t Pay

It happens. Even with the best systems, sometimes a roommate falls behind. Here’s how to handle it without destroying your credit or your living situation.

First: pay the bill yourself if it’s in your name. Seriously. Whatever the amount, cover it and protect your payment history. A late payment on your credit report does way more long-term damage than the short-term cost of fronting someone’s share.

Then, have the conversation. Be direct but not aggressive. “Hey, I covered the internet bill this month because it was about to be late. I need your half by Friday.” Specific, clear, with a deadline. Most people respond better to this than a passive-aggressive Venmo request with a frowny face.

If it becomes a pattern, restructure. Remove the bill from your name. Or set up a shared bank account that everyone contributes to on the 1st of each month, specifically for bills. The goal is to create a system where your credit isn’t dependent on a reminder text.

And if a roommate truly refuses to pay and you’re stuck with the bill? Document everything. You may be able to pursue it in small claims court if the amount is significant enough. But your first priority is always ensuring the bill is paid on time in your name.

Build Credit You Actually Control

Here’s the real takeaway from all of this: the most reliable credit is credit that depends on nobody but you.

Shared bills are part of life, and the strategies above will help you manage the risk. But the foundation of your credit history should be built on accounts where you’re the only variable. Where your payment behavior - and only your payment behavior - determines what gets reported.

That’s where something like the Arro Card comes in. It’s a credit card in your name, building your credit history based on your spending and your payments. No roommate involved. No shared responsibility. Every on-time payment builds your profile. Every month of low utilization strengthens your score.

You can track everything in the Arro App - your credit score, your spending, your utilization - so you always know where you stand. Artie, your AI Money Coach, can answer questions about how shared expenses affect your credit or help you figure out if your utilization is creeping up from fronting group costs.

No hard credit check to apply. No deposit. No annual fee. 1% cash back on gas & groceries. And the credit you build is yours - not tied to anyone else’s ability to remember a due date.

➡️ Start building credit in your name. Download the Arro App for free - your score, your insights, your AI coach, all in one place.

FAQ

Can splitting bills with roommates hurt my credit?

Yes. If a shared bill is in your name and it’s paid late or goes unpaid, that negative mark appears on your credit report, even if your roommate was supposed to cover their share. The credit risk of split bills falls entirely on the account holder.

How do I protect my credit when sharing expenses with roommates?

Distribute bill ownership across roommates so no one person carries all the risk. Set up AutoPay on any bill in your name, use payment apps to create accountability, and keep a written record of who’s responsible for what.

Does my roommate’s late payment affect my credit score?

Only if the late bill is in your name will credit bureaus report it based on account ownership. If your roommate is the account holder, their late payment affects their credit, not yours. Always confirm whose name is tied to each shared account.

Should I put all shared bills in my name to keep things simple?

No. Putting all bills in your name means you bear 100% of the credit risk for the entire household's split bills. Instead, divide account ownership so each roommate is responsible for at least one bill. This spreads the risk fairly.

What happens if a utility bill goes to collections because of my roommate?

If the utility is in your name, the collections account appears on your credit report regardless of who caused it. Collections can significantly lower your score and stay on your report for up to seven years. Always pay bills in your name on time, then separately pursue reimbursement from roommates.

How can I build credit without relying on my roommates?

Use a credit card that’s solely in your name - like the Arro Card. Your payment history and utilization are based entirely on your own behavior. No shared risk, no dependence on anyone else. The Arro Card requires no hard credit check, no deposit, and has no annual fee.

Does fronting group expenses on my credit card affect my score?

It can. If you frequently charge shared expenses to your card before being reimbursed, your credit utilization may spike. High utilization can temporarily lower your score. Try to keep your balance at or below 30% of your limit, and use the Arro App to monitor utilization in real time.

Resources

Experian. How Is Your Credit Score Calculated?

Facing Disruption. The Invisible Ledger: AI's Growing Debt Crisis