Team Arro

Table Of Contents

The Truth About Credit Repair Companies

Common Credit Report Errors Worth Disputing

How To Dispute Credit Report Errors: Step-by-Step

Building Your Paper Trail

What Happens After You File

If Your Dispute Is Denied

How Arro Helps You Build Credit The Right Way

What To Do Next

FAQ

Credit repair companies promise quick fixes and guaranteed results, charging monthly fees of $50 to $150, plus setup fees up to $200. Over several months, you could spend $500 to $1,000 or more. But here's the truth: anything a credit repair company can legally do, you can do yourself for free.

If you're struggling with a low credit score, this guide shows you exactly how to dispute credit report errors on your own, build the paper trail that protects you, and avoid unnecessary repair fees. The Consumer Financial Protection Bureau (CFPB) and Federal Trade Commission (FTC) provide free resources and template letters to help you, and we'll walk you through every step.

Errors on credit reports are surprisingly common, and fixing them can build your credit history without spending a dime. Whether it's a payment marked late, an account that isn't yours, or outdated negative information, you have the right to dispute it, for free.

The Truth About Credit Repair Companies

Legitimate credit repair services identify potential errors on your credit reports and submit disputes to credit bureaus on your behalf. That's essentially it, a process you can complete yourself.

What They Can't Do

According to the CFPB, credit repair companies cannot:

Remove accurate negative information: If information is accurate and current, no one can legally remove it. It stays for 7 years (most items) or 10 years (bankruptcies).

Guarantee specific credit score increases: No company can promise exact point gains

Create a "new" credit identity: Using an EIN instead of your SSN is illegal and constitutes fraud

Instantly fix your credit: Legitimate improvement takes months to years

Red Flags of Scams

The Credit Repair Organizations Act (CROA) protects consumers. Watch for:

Demanding upfront payment: It's illegal for credit repair companies to charge before completing services

Telling you not to contact credit bureaus: You have the legal right to communicate directly

Pressuring you to dispute accurate information: This wastes time and could be fraudulent

Making unrealistic guarantees: "Remove bankruptcies in 30 days!" is a lie

Lacking transparency: Legitimate services provide detailed contracts upfront

Your Legal Rights

The Fair Credit Reporting Act (FCRA) gives you the right to:

Access free credit reports annually at AnnualCreditReport.com

Dispute inaccurate information

Have disputes investigated within 30 days

Add explanatory statements to your file

The government provides free dispute letter templates and step-by-step guidance. Save your money and use these free resources.

Common Credit Report Errors Worth Disputing

Not all credit report information can be disputed successfully. The CFPB identifies these disputable errors:

Personal Information: Incorrect name, address, or SSN; accounts belonging to someone else; identity theft accounts

Account Status: Accounts listed as open when closed; duplicate accounts; incorrect balances or limits

Payment History: Payments marked late when paid on time; negative information older than 7 years (10 for Chapter 7 bankruptcy)

Unrecognized Accounts: Credit cards or loans you never opened (potential identity theft)

What You Cannot Dispute Away

You cannot legally remove accurate negative information:

Late payments you actually made

Legitimate collection accounts

Foreclosures, repossessions, or bankruptcies that occurred

High utilization that reflects actual balances

Accurate negatives remain for 7-10 years, but their impact decreases as you build positive credit history.

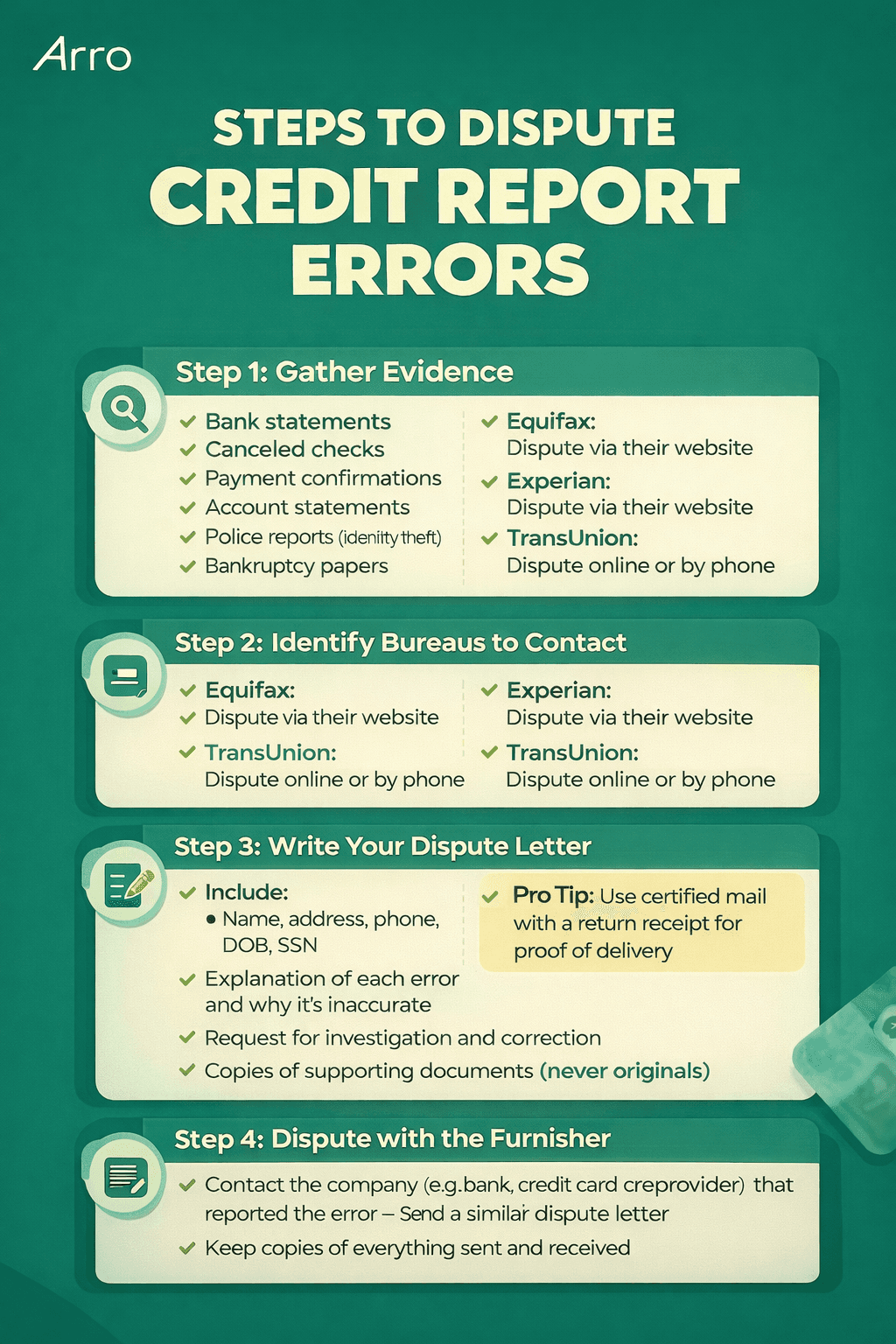

How To Dispute Credit Report Errors: Step-By-Step

Step 1: Gather Evidence

The CFPB recommends collecting copies of: bank statements, canceled checks, payment confirmations, account statements, police reports (identity theft), or bankruptcy papers.

Step 2: Identify Which Bureaus to Contact

Dispute with each credit bureau showing the error:

Equifax: www.equifax.com/personal/credit-report-services/credit-dispute/

Experian: www.experian.com/disputes/main.html

TransUnion: Online or phone on credit report

Step 3: Write Your Dispute Letter

Use the CFPB's sample dispute letter. Include:

Your complete name, address, phone, DOB, and SSN

Clear explanation of each error

Why is it inaccurate

Request to investigate and correct

Copies of supporting documents (never originals)

Pro tip: Mail disputes using certified mail with a return receipt for proof of delivery.

Step 4: Also Dispute with the Furnisher

The furnisher (bank, credit card company, etc.) provided the information. Send them a similar letter for faster resolution.

Step 5: Track Your Timeline

By law, credit bureaus have 30 days to investigate (45 days if you send additional info). Keep copies of everything you send and receive.

Building Your Paper Trail

Strong documentation prevents dismissal as "frivolous" and speeds resolution.

Essential Documents by Dispute Type

Payment Disputes: Bank statements, canceled checks, and payment confirmations

Account Status: Closure letters, final statements

Identity Theft: FTC Identity Theft Report, police report

Bankruptcy: Discharge papers, bankruptcy schedules

Organization Tips

Create a dispute file (physical or digital)

Never send originals, only copies

Label everything clearly

Keep certified mail receipts

Update a tracking checklist

What Happens After You File

The 30-Day Process

Credit bureaus have 30 days to:

Forward your dispute to the furnisher

Investigate your claim

Send you written results

Three Possible Outcomes

Corrected: Error verified and fixed; you get a free updated report.

Unverified: Information can't be verified, so it's deleted.

Denied: Investigation confirms information is accurate.

If corrected, request your updated report to verify that changes were made properly.

If Your Dispute Is Denied

If denied, you can:

Add a consumer statement explaining the dispute (100 words)

Gather more evidence and re-dispute with additional documentation

File a CFPB complaint at www.consumerfinance.gov/complaint

Contact your state Attorney General

Consult an FCRA attorney for possible legal action

Sometimes, for minor errors or items falling off soon, focus energy on building positive credit instead.

How Arro Helps You Build Credit The Right Way

While disputing errors fixes past mistakes, building positive credit history creates lasting improvement, without expensive repair fees.

No Credit Check, No Deposit

Arro uses alternative data like income instead of credit scores:

No hard inquiry: Applying doesn't hurt your score

No deposit needed: Start building immediately

Approval based on income: Not just traditional credit scores

Real Credit Building

Arro reports to all three bureaus: TransUnion, Experian, Equifax:

Every on-time payment counts: Payment history = 35% of your score

Proven results: Members are building stronger credit with every on-time payment

Financial Education + Rewards

Instead of paying credit repair companies, Arro empowers you:

Free financial literacy lessons

AI financial coach (Artie) for personalized guidance

1% cash back on gas and groceries

Credit limit increases. Starting limit up to $300, growing up to $2,500 as you build credit.

"Instant approval with NO hard credit check and NO deposit was a game changer," says Maggie G.

The path to better credit requires knowledge, consistency, and the right tools. Arro provides all three.

Also, read:

Ask & Receive: Understanding the Impact of Requesting a Credit Limit Increase

Arro’s Commitment to Financial Literacy - Arro | Grow Credit Your Way

What To Do Next

Learning how to dispute credit report errors yourself isn't just about saving money; it's about taking control of your financial future. You now have the knowledge to identify errors, the templates to write effective disputes, the strategy to build strong documentation, and the timeline for investigations.

But fixing past errors is only half the battle. Building a positive credit history going forward is key. Every on-time payment, every month of low utilization, and every financial lesson you complete moves you closer to your goals.

Your Action Plan

This week: Order free reports from AnnualCreditReport.com, review for errors, and gather documentation

This month: Write disputes using the CFPB template, mail via certified mail, and track progress

Ongoing: Make on-time payments, keep utilization low, monitor credit quarterly, build positive history

According to the FTC, you can accomplish everything for free. The power to improve your credit is yours, without paying expensive repair fees.

Apply now - no hard credit check, no deposit required.

Apply now and take control of your financial future.

FAQ

Can I dispute credit report errors myself without paying anyone?

Absolutely. According to the Federal Trade Commission (FTC), anything a credit repair company can legally do, you can do for free. Credit repair companies often charge for services that you can easily handle yourself. You can dispute errors directly with the credit bureaus and use resources like the Consumer Financial Protection Bureau (CFPB), which offers free templates to help you through the dispute process. It's all about taking advantage of the tools and guidelines available to you at no cost.

How long does the dispute process take?

By law, credit bureaus have 30 days to investigate a dispute. However, if you provide additional information during the dispute, they are allowed up to 45 days to complete the investigation. Once the investigation is complete, they must respond in writing with the results and, if the dispute results in a correction, provide a free updated credit report. It’s important to keep track of the timeline and follow up if necessary.

Do I need to dispute with all three credit bureaus?

Yes, you need to dispute with each bureau separately if the error appears on multiple reports. The three major credit bureaus, Equifax, Experian, and TransUnion, each maintain their own independent records. Therefore, a mistake on one bureau's report does not automatically get corrected on the others. You’ll have to contact each bureau to address the error on their respective report.

Can credit repair companies remove accurate negative information?

No, it is illegal for anyone, including credit repair companies, to remove accurate negative information from your credit report. Legitimate negative marks, like late payments, can remain on your report for up to 7 years. However, certain types of bankruptcy, like Chapter 7, can stay for up to 10 years. While these marks will affect your score initially, their impact decreases over time as you continue to build a positive credit history.

What documentation do I need?

When disputing credit report errors, it’s important to provide strong supporting documentation. The CFPB recommends including copies of relevant documents such as bank statements, canceled checks, payment confirmations, account statements, and police reports (in cases of identity theft). If you've filed for bankruptcy, include the relevant paperwork. The more concrete evidence you provide, the stronger your case will be.

Are upfront fees for credit repair illegal?

Yes, credit repair companies are not allowed to charge upfront fees under the Credit Repair Organizations Act (CROA). They can only charge after they have completed the services. If a company demands payment before performing any work, it is violating federal law. Be cautious of companies that ask for money up front, as this is a red flag for potential fraud.

What if my dispute is denied?

If your dispute is denied, you have several options. First, you can add a consumer statement to your credit report to explain your side of the situation. You can also gather more evidence and resubmit the dispute. If the issue persists, consider filing a complaint with the CFPB at www.consumerfinance.gov/complaint. Additionally, you can contact your state Attorney General (AG) or consult with a Fair Credit Reporting Act (FCRA) attorney for further assistance.

How often should I check my credit reports?

It’s recommended that you check your credit reports annually from all three major bureaus. You can do this for free at AnnualCreditReport.com. To keep track of your credit throughout the year, you can space out your requests, one from each bureau every 4 months. If you're actively working to build or rebuild credit, it’s a good idea to check your reports more frequently to stay on top of any changes or potential errors.

Will disputing hurt my credit score?

No, disputing an error on your credit report will not hurt your credit score. The credit bureaus are not allowed to negatively impact your score while they are investigating a legitimate dispute. However, if you dispute accurate information (a frivolous dispute), it could harm your credibility with the bureaus and may even result in your claims being flagged as baseless. It's important to only dispute inaccuracies.

Can I dispute online, or must I mail letters?

Both online and mail disputes are valid, but the FTC recommends submitting your dispute by certified mail with a return receipt. This method creates a proof of delivery, which can be crucial if you need to escalate the issue or if there are any disputes about whether the bureau received your correspondence. Using a paper trail offers extra protection and peace of mind in case things don’t go as planned.