Table of Contents

Why Learning Credit Terms Matters

Bridging Language Barriers: A Global Need

The 25 Most Important Credit Terms Explained

Your Path To Financial Confidence

FAQs

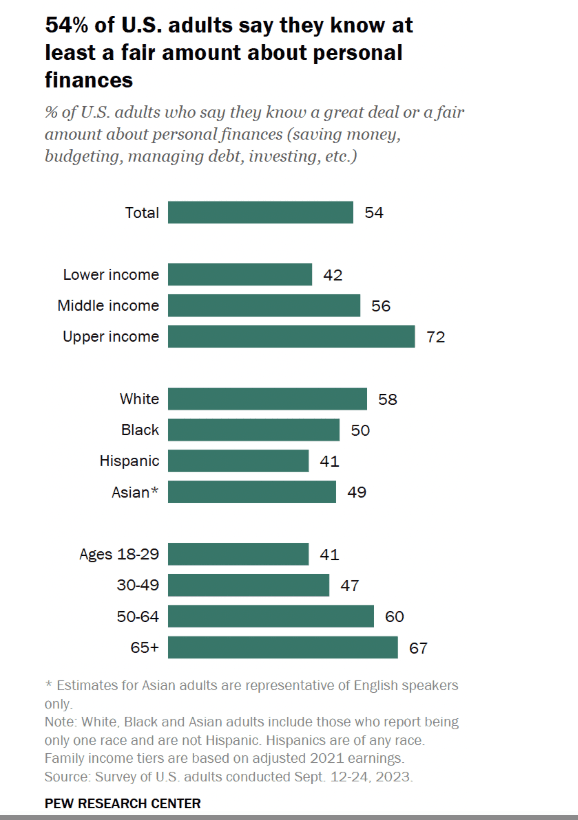

Financial language is everywhere, from loan offers to bank statements, and if the terms are confusing, you’re not alone. A survey found that only 54% of U.S. adults say they know a great deal or a fair amount about personal finances, meaning nearly half aren’t confident about essential money topics such as budgeting and credit.

Source: Pew Research Center

That’s a big reason why so many people struggle with money: not because they’re bad with money, but because the language feels unfamiliar. In this article, we'll explain 25 credit terms in plain English, with Spanish and Hindi definitions, and real-world examples, so you can understand how they impact your financial decisions.

Key Takeaways:

Understanding credit terms helps you make better financial decisions.

Clear definitions in English, Spanish, and Hindi make credit concepts accessible to everyone.

Mastering credit vocabulary can help you avoid mistakes and improve financial decisions.

Regularly reviewing your credit score and report helps you make smarter financial decisions.

Arro’s tools simplify credit-building and reward your everyday spending.

Why Learning Credit Terms Matters

Financial literacy is essential for managing personal finances, but surprisingly low levels of understanding persist even among adults making complex financial decisions.

According to the OECD, financial literacy involves grasping fundamental concepts like money management, borrowing, and planning, all of which are critical in navigating daily life, from budgeting to making informed purchasing decisions.

Many adults lack basic financial knowledge: Terms like APR (Annual Percentage Rate) and interest can be confusing, making people hesitant to engage with financial products or make mistakes later because they didn’t understand the terminology.

Misunderstanding these terms can have consequences: Not understanding financial terms can lead to missed opportunities, penalties, and financial setbacks, including high-interest debt or late payments, which can have lasting impacts on credit and finances.

Learning these terms isn’t just about building a vocabulary; it’s about empowering yourself to make confident, informed decisions. Gaining control over financial terminology means taking control over your financial future, helping you navigate loans, credit cards, and investments without the fear of hidden fees or misunderstandings.

Bridging Language Barriers: A Global Need

Financial literacy isn’t just a challenge in the U.S.; it’s a global issue. Around the world, levels of financial understanding vary significantly, and many adults, even in developed economies, feel ill-equipped to make important financial decisions.

Research has found that financial literacy remains low and often inadequate for the kinds of financial choices people face today, particularly for vulnerable groups like immigrants or low-income households.

Low financial literacy globally: Even in mature markets, many individuals struggle to navigate complex financial systems, leaving them at a disadvantage when making key decisions.

Vulnerable groups are most affected: Immigrants, low-income households, and other vulnerable populations often face the most significant barriers to understanding and accessing financial resources.

This lack of understanding can lead to poor decision-making and missed opportunities. To help bridge this gap, translating credit terms into languages such as Spanish and Hindi makes this guide far more accessible and impactful.

By providing definitions in these languages, we ensure that newcomers, multilingual readers, and those who are more comfortable with their native language can truly understand their finances and feel more confident making financial decisions that affect their lives.

The 25 Most Important Credit Terms Explained

Understanding the following terms will make managing your finances easier and more straightforward. Here’s a breakdown of key terms, translated into English, Spanish, and Hindi, to help bridge the gap and ensure you feel confident in using these terms.

Term | English Definition | Spanish | Hindi |

AutoPay | A feature that automatically pays your credit card or loan bill from your bank account on a set date to help avoid missed payments. | Pago automático | स्वचालित भुगतान |

APR (Annual Percentage Rate) | The annual cost of borrowing, including interest and fees, is shown as a percentage. This determines the cost of your loan. | Tasa de interés anual | वार्षिक ब्याज दर |

Interest on Loan | The cost of borrowing money, typically expressed as a percentage of the loan amount, is what you pay in addition to the principal. | Interés sobre el préstamo | ऋण पर ब्याज |

Credit Score | A three-digit number that represents your creditworthiness. The higher the score, the more likely you are to be approved for loans at better prices. | Puntaje crediticio | ऋणात्मक स्कोर |

Credit Report | A detailed summary of your credit history, including all loans, credit cards, payments, and balances. | Informe de crédito | ऋण रिपोर्ट |

Credit Utilization | The percentage of available credit you're using. Keeping it below 30% is recommended for a good score. | Utilización de crédito | क्रेडिट उपयोग |

Interest Rate | The cost you pay to borrow money, expressed as a percentage of the loan amount. For some loans, this is the same as APR. | Tasa de interés | ब्याज दर |

Collateral | An asset pledged to secure a loan, such as a car or home. If you default, the lender can seize it to recover the debt. | Colateral | उत्तरदायी जमानत |

Secured vs Unsecured Loans | Secured loans are backed by collateral, while unsecured loans don’t require collateral but tend to have higher interest rates. | Préstamos garantizados vs no garantizados | सुरक्षित बनाम असुरक्षित ऋण |

Secured Credit Card | A credit card that requires a deposit as collateral, which acts as your credit limit. | Tarjeta de crédito asegurada | सुरक्षित क्रेडिट कार्ड |

Debt-to-Income Ratio | A percentage that compares your debt payments to your income. A lower ratio is better for loan approval. | Relación deuda-ingresos | कर्ज-से-आय अनुपात |

Default | Failing to meet the terms of a loan typically results in severe consequences such as foreclosure or legal action. | Incumplimiento | डिफ़ॉल्ट |

Bankruptcy | A legal process that helps individuals or businesses eliminate or repay their debts under the protection of a court. | Quiebra | दिवालियापन |

Charge-Off | A debt that a lender deems uncollectible after a long period of non-payment, usually after six months. | Cancelación de deuda | चार्ज-ऑफ |

Refinancing | The process of replacing an existing loan with a new one, often with better terms, such as a lower interest rate. | Refinanciación | पुनर्वित्त |

Credit Limit | The maximum amount you can borrow on a credit card or line of credit. | Límite de crédito | ऋण सीमा |

Minimum Payment | The lowest amount you can pay on your credit card bill to avoid late fees. | Pago mínimo | न्यूनतम भुगतान |

Late Payment Fee | A fee charged when you miss a payment deadline for a credit card or loan. | Cargo por pago tardío | विलंब भुगतान शुल्क |

Grace Period | The period after the bill’s due date during which you can pay without incurring interest charges. | Período de gracia | क्षमा अवधि |

Credit Card Statement | A summary of your credit card activity, including the balance, payments, interest, and any fees during the billing cycle. | Estado de cuenta de tarjeta de crédito | क्रेडिट कार्ड स्टेटमेंट |

Credit Inquiry | When a lender or financial institution checks your credit report to assess your financial health. | Consulta de crédito | क्रेडिट पूछताछ |

Credit Building | The process of improving your credit by using credit products responsibly, such as paying off loans on time. | Construcción de crédito | क्रेडिट निर्माण |

Balance Transfer | The act of moving debt from one credit card to another, typically to take advantage of a lower interest rate. | Transferencia de saldo | बैलेंस ट्रांसफर |

Co-Signer | A person who agrees to take responsibility for a loan if the primary borrower defaults. | Co-firmante | सहामूल्यदाता |

Prepayment Penalty | A fee is charged if you pay off your loan before its term ends. | Penalización por pago anticipado | पूर्व भुगतान शुल्क |

Revolving Credit | A credit arrangement that allows you to borrow up to a limit, pay it off, and borrow again. | Crédito renovable | रिवोल्विंग क्रेडिट |

With these 25 essential credit terms clearly defined, you now have the foundation to confidently navigate the world of personal finance and make smarter decisions for your financial future.

Also read:

Balance Transfer or Personal Loan: What is the Right Fit for You?

Your Must-Read Guide to Understanding a Negative Balance on Your Credit Card

How to Build Credit Without a Credit Card: Steps to Get Started

Your Path To Financial Confidence

In this article, we've broken down 25 key credit terms to help you navigate the world of personal finance more easily. Whether you're just starting out or looking to improve your financial knowledge, understanding these terms is the first step toward making smart credit decisions.

At Arro, we believe that building credit shouldn’t be complicated or intimidating. That's why we’ve created a credit card that makes it easy to learn, earn, and grow your credit, all through a single, user-friendly app. With no hard credit checks, no deposit required, and 1% cash back on gas and groceries, Arro lets you improve your credit while earning rewards for your everyday spending.

You’ll also have access to Artie, your personal AI Money Coach, available 24/7 to answer your questions, celebrate your wins, and guide you toward smarter financial choices. Every on-time Payment, every lesson learned, and every small step forward helps you unlock higher credit limits and build stronger credit health.

Thousands of people are already using Arro to improve their credit and have fun along the way.

Ready to start your own journey? Join Arro today and take control of your credit-building journey!

FAQs

1. How can I start building my credit if I have no credit history?

To start building your credit, consider a credit card like Arro, which doesn’t require any prior credit history for approval. Arro lets you build credit through everyday purchases and on-time payments without a security deposit or hard credit check.

These options allow you to make small purchases and make on-time payments to establish a positive credit history. Many secured cards also offer a path to upgrading to an unsecured card once you’ve demonstrated responsible use.

2. What is the difference between secured and unsecured loans?

A secured loan is backed by collateral, such as a house or car, which the lender can seize if you fail to repay the loan. On the other hand, an unsecured loan doesn’t require collateral and is typically based on your creditworthiness. While unsecured loans can be riskier for lenders, they are often offered at higher interest rates to compensate for that risk. Understanding the difference helps you choose the right loan for your financial situation and ensures you’re aware of the terms.

3. How often should I check my credit score?

It's a good practice to check your credit score at least once every three months. Monitoring your credit score regularly helps you track your progress, identify discrepancies or errors, and ensure your financial decisions are on track. Furthermore, many services offer free access to your credit score, making it easier than ever to keep tabs on your credit health at no additional cost.

4. What is the role of an AI Money Coach in managing my credit?

An AI Money Coach, like Arro’s Artie, provides personalized financial guidance that adapts to your unique credit journey. Artie helps answer your questions, tracks your progress, and offers tips on building credit, saving money, and improving your financial habits. With Artie, you’ll get immediate feedback and step-by-step assistance, whether it’s learning how to reduce your credit utilization or understanding your credit report better. This makes managing your finances not only more efficient but also less overwhelming.

5. Are there any hidden fees with Arro’s credit card?

Arro is committed to transparency, with clear pricing and no surprise charges. While the Arro Card has an annual fee, all fees and terms are clearly outlined up front. There’s no security deposit required, and Arro is designed to avoid many of the confusing or unexpected fees often found in traditional credit products.